Multiple Choice

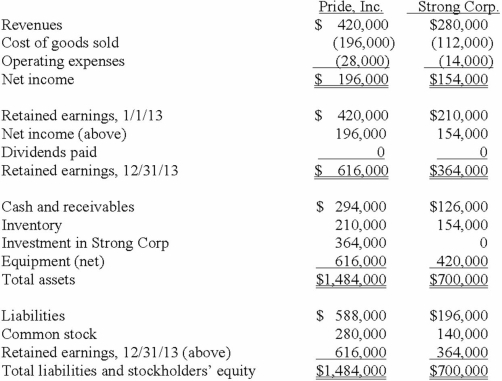

On January 1, 2013, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2013, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2013, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31, 2013.

What is the total of consolidated cost of goods sold?

A) $196,000.

B) $212,800.

C) $184,800.

D) $203,000.

E) $168,000.

Correct Answer:

Verified

Correct Answer:

Verified

Q71: Strickland Company sells inventory to its parent,

Q72: An intra-entity sale took place whereby the

Q73: Throughout 2013, Cleveland Co. sold inventory to

Q74: Clemente Co. owned all of the voting

Q75: Wilson owned equipment with an estimated life

Q77: Pepe, Incorporated acquired 60% of Devin Company

Q78: Pot Co. holds 90% of the common

Q79: What is meant by unrealized inventory gains,

Q81: Gargiulo Company, a 90% owned subsidiary of

Q100: What is the purpose of the adjustments