Essay

Consider the model Yi - β1Xi + ui,where the Xi and ui the are mutually independent i.i.d.random variables with finite fourth moment and E(ui)= 0.

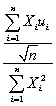

(a)Let  1 denote the OLS estimator of β1.Show that

1 denote the OLS estimator of β1.Show that  (

(  1- β1)=

1- β1)=  .

.

(b)What is the mean and the variance of  ? Assuming that the Central Limit Theorem holds,what is its limiting distribution?

? Assuming that the Central Limit Theorem holds,what is its limiting distribution?

(c)Deduce the limiting distribution of  (

(  1 - β1)? State what theorems are necessary for your deduction.

1 - β1)? State what theorems are necessary for your deduction.

Correct Answer:

Verified

(a)The OLS estimator in this case is  1 ...

1 ...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q8: If, in addition to the least squares

Q15: (Requires Appendix material)If X and Y are

Q26: One of the earlier textbooks in econometrics,

Q28: In order to use the t-statistic for

Q29: Suppose that the conditional variance is var(ui|Xi)=

Q32: The class of linear conditionally unbiased estimators

Q33: You need to adjust <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2833/.jpg" alt="You

Q34: The following is not part of the

Q35: Homoskedasticity means that<br>A)var(ui|Xi)= <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2833/.jpg" alt="Homoskedasticity means

Q36: Your textbook states that an implication of