Exam 14: Oligopoly

Exam 1: First Principles199 Questions

Exam 2: Economic Models: Trade-Offs and Trade299 Questions

Exam 4: Consumer and Producer Surplus229 Questions

Exam 3: Supply and Demand265 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets216 Questions

Exam 6: Elasticity226 Questions

Exam 7: Taxes286 Questions

Exam 8: International Trade260 Questions

Exam 9: Decision Making by Individuals and Firms186 Questions

Exam 10: The Rational Consumer182 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs317 Questions

Exam 12: Perfect Competition and the Supply Curve341 Questions

Exam 13: Monopoly317 Questions

Exam 14: Oligopoly271 Questions

Exam 15: Monopolistic Competition and Product Differentiation245 Questions

Exam 16: Externalities193 Questions

Exam 17: Public Goods and Common Resources208 Questions

Exam 18: The Economics of the Welfare State126 Questions

Exam 19: Factor Markets and the Distribution of Income316 Questions

Exam 20: Uncertainty, Risk, and Private Information192 Questions

Exam 21: Graphs in Economics60 Questions

Exam 22: Consumer Preferences and Consumer Choice135 Questions

Select questions type

_____ occurs when the only two firms in an industry agree to fix the price at a given level.

Free

(Multiple Choice)

4.9/5  (33)

(33)

Correct Answer: Verified

Verified

A

When a firm responds to a rival's cheating by cheating and to a rival's cooperation by cooperating,that firm is practicing a _____ strategy.

Free

(Multiple Choice)

4.9/5 (33)

Correct Answer:Verified

D

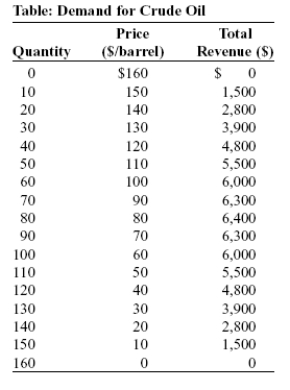

Use the following to answer question:  -(Table: Demand for Crude Oil)Use Table: Demand for Crude Oil.Assume that the crude oil industry is a duopoly and the marginal cost and fixed cost of producing crude oil equal zero.Suppose that the two firms are maximizing industry profit and splitting the profit evenly.If both firms decide to cheat and produce 10 more barrels each,industry output will be _____ barrels.

-(Table: Demand for Crude Oil)Use Table: Demand for Crude Oil.Assume that the crude oil industry is a duopoly and the marginal cost and fixed cost of producing crude oil equal zero.Suppose that the two firms are maximizing industry profit and splitting the profit evenly.If both firms decide to cheat and produce 10 more barrels each,industry output will be _____ barrels.

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

A

Suppose there are 10 identical firms in an industry and each produces 10% of the total market sales.The HHI for this industry would indicate that the industry is:

(Multiple Choice)

4.7/5 (38)

Antitrust legislation was first passed in the United States in 1776.

(True/False)

4.9/5 (37)

The FIRST trust in the United States was established by _____ in the _____ industry.

(Multiple Choice)

4.8/5 (31)

Use the following to answer question:

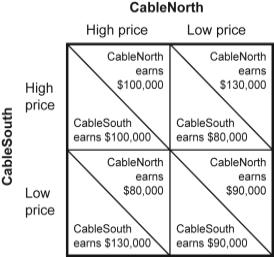

Figure: Pricing Strategy in Cable TV Market II  -(Figure: Pricing Strategy in Cable TV Market II)Use Figure: Pricing Strategy in Cable TV Market II.If CableNorth followed a high-price strategy one period but found that CableSouth followed a noncooperative low-price strategy,and CableNorth decided to lower prices for the next month,we would say that CableNorth is following a:

-(Figure: Pricing Strategy in Cable TV Market II)Use Figure: Pricing Strategy in Cable TV Market II.If CableNorth followed a high-price strategy one period but found that CableSouth followed a noncooperative low-price strategy,and CableNorth decided to lower prices for the next month,we would say that CableNorth is following a:

(Multiple Choice)

4.7/5 (27)

A trust is a government agency that enforces laws limiting the power of oligopolies.

(True/False)

4.9/5 (27)

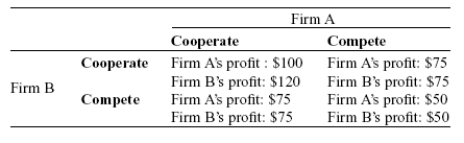

(Scenario: Payoff Matrix for Two Firms)Use Scenario: Payoff Matrix for Two Firms.Firm B has: Scenario: Payoff Matrix for Two Firms

The following table provides the payoff matrix for two firms,firm A and firm B.They are the only two firms in the industry and can either compete or cooperate with each other,with the following profit results reflecting their actions.

(Multiple Choice)

4.9/5 (38)

Use the following to answer question:

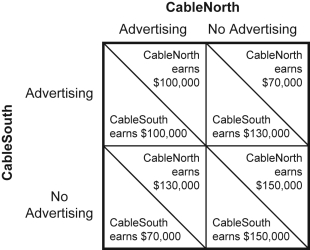

Figure: Pricing Strategy in Cable TV Market I  -(Figure: Pricing Strategy in Cable TV Market I)Use Figure: Pricing Strategy in Cable TV Market I.If neither CableNorth nor CableSouth advertises,then without any collusion:

-(Figure: Pricing Strategy in Cable TV Market I)Use Figure: Pricing Strategy in Cable TV Market I.If neither CableNorth nor CableSouth advertises,then without any collusion:

(Multiple Choice)

4.9/5 (31)

In the 1960s and 1970s,General Motors often set prices for the new model year and Ford and Chrysler would follow.This was a form of tacit collusion known as price leadership.

(True/False)

4.9/5 (35)

Which example is MOST likely to be observed when firms engage mainly in nonprice competition?

(Multiple Choice)

4.9/5 (29)

A strategy in which players cooperate initially but then mimic what the other players do is referred to as a:

(Multiple Choice)

4.9/5 (32)

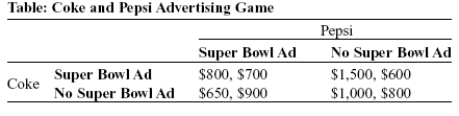

Use the following to answer question:  -(Table: Coke and Pepsi Advertising Game)Use Table: Coke and Pepsi Advertising Game.The soft-drink industry is dominated by Coca-Cola and Pepsi,and each firm spends a lot of money on advertising.Suppose each firm is considering a costly television commercial during halftime of the Super Bowl.The table shows the payoff matrix of profits that each firm would receive from their advertising decision,given the advertising decision of their rival.Profits in each cell of the payoff matrix are given as (Coke,Pepsi).If both firms expect to play this game repeatedly (every year for the foreseeable future)and they use a tit-for-tat strategy,in equilibrium,Coke _____ and Pepsi _____.

-(Table: Coke and Pepsi Advertising Game)Use Table: Coke and Pepsi Advertising Game.The soft-drink industry is dominated by Coca-Cola and Pepsi,and each firm spends a lot of money on advertising.Suppose each firm is considering a costly television commercial during halftime of the Super Bowl.The table shows the payoff matrix of profits that each firm would receive from their advertising decision,given the advertising decision of their rival.Profits in each cell of the payoff matrix are given as (Coke,Pepsi).If both firms expect to play this game repeatedly (every year for the foreseeable future)and they use a tit-for-tat strategy,in equilibrium,Coke _____ and Pepsi _____.

(Multiple Choice)

4.9/5 (45)

A strategy that is the same,regardless of the action of the other player in a game,is a _____ strategy.

(Multiple Choice)

4.8/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)