Exam 12: Perfect Competition and the Supply Curve

Exam 1: First Principles199 Questions

Exam 2: Economic Models: Trade-Offs and Trade299 Questions

Exam 4: Consumer and Producer Surplus229 Questions

Exam 3: Supply and Demand265 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets216 Questions

Exam 6: Elasticity226 Questions

Exam 7: Taxes286 Questions

Exam 8: International Trade260 Questions

Exam 9: Decision Making by Individuals and Firms186 Questions

Exam 10: The Rational Consumer182 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs317 Questions

Exam 12: Perfect Competition and the Supply Curve341 Questions

Exam 13: Monopoly317 Questions

Exam 14: Oligopoly271 Questions

Exam 15: Monopolistic Competition and Product Differentiation245 Questions

Exam 16: Externalities193 Questions

Exam 17: Public Goods and Common Resources208 Questions

Exam 18: The Economics of the Welfare State126 Questions

Exam 19: Factor Markets and the Distribution of Income316 Questions

Exam 20: Uncertainty, Risk, and Private Information192 Questions

Exam 21: Graphs in Economics60 Questions

Exam 22: Consumer Preferences and Consumer Choice135 Questions

Select questions type

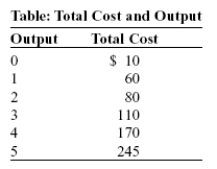

Use the following to answer question:  -(Table: Total Cost and Output)Use Table: Total Cost and Output,which describes Sergei's total costs for his perfectly competitive all-natural ice cream firm.If the market price of a tub of ice cream is $20,how many tubs of ice cream will Sergei produce in the short run?

-(Table: Total Cost and Output)Use Table: Total Cost and Output,which describes Sergei's total costs for his perfectly competitive all-natural ice cream firm.If the market price of a tub of ice cream is $20,how many tubs of ice cream will Sergei produce in the short run?

Free

(Multiple Choice)

5.0/5  (32)

(32)

Correct Answer: Verified

Verified

A

The short-run supply curve for a perfectly competitive firm is its:

Free

(Multiple Choice)

4.8/5 (28)

Correct Answer:Verified

C

When economic profits in an industry are zero:

Free

(Multiple Choice)

4.8/5 (26)

Correct Answer:Verified

B

If a perfectly competitive firm is producing a quantity where P > MC,then the firm can increase profit by:

(Multiple Choice)

4.8/5 (32)

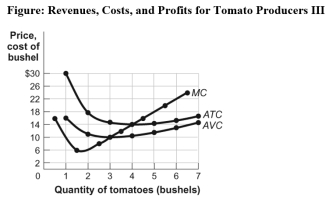

Use the following to answer question:  -(Figure: Revenues,Costs,and Profits for Tomato Producers III)Use Figure: Revenues,Costs,and Profits for Tomato Producers III.The market for tomatoes is perfectly competitive.If the market price of a bushel of tomatoes is $8,in the short run the farmer's profit-maximizing output is _____ bushels.

-(Figure: Revenues,Costs,and Profits for Tomato Producers III)Use Figure: Revenues,Costs,and Profits for Tomato Producers III.The market for tomatoes is perfectly competitive.If the market price of a bushel of tomatoes is $8,in the short run the farmer's profit-maximizing output is _____ bushels.

(Multiple Choice)

4.7/5 (38)

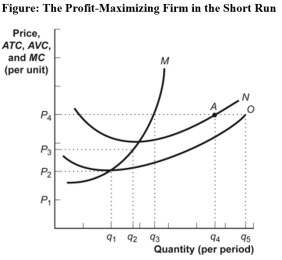

Use the following to answer question:  -(Figure: The Profit-Maximizing Firm in the Short Run)Use Figure: The Profit-Maximizing Firm in the Short Run.N is the _____ curve.

-(Figure: The Profit-Maximizing Firm in the Short Run)Use Figure: The Profit-Maximizing Firm in the Short Run.N is the _____ curve.

(Multiple Choice)

5.0/5 (32)

Use the following to answer question:

-(Table: Total Cost and Output)Use Table: Total Cost and Output,which describes Sergei's total costs for his perfectly competitive all-natural ice cream firm.If the market price of a tub of ice cream is $50,how much is Sergei's profit at the profit-maximizing output?

(Multiple Choice)

4.7/5 (41)

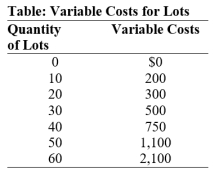

Use the following to answer question:  -(Table: Variable Costs for Lots)Use Table: Variable Costs for Lots.During the winter,Alexa runs a snow-clearing service in a perfectly competitive industry,which is made up of 50 identical firms.Assume that costs are constant in each interval;so,for example,the marginal cost of clearing each of the lots from 1 through 10 is $20.Also assume that she can only plow the quantities of the lots given in the table (and not numbers in between).Her only fixed cost is $1,000 for a snowplow.Her variable costs include fuel,her time,and hot coffee.Which point falls on the industry short-run supply curve?

-(Table: Variable Costs for Lots)Use Table: Variable Costs for Lots.During the winter,Alexa runs a snow-clearing service in a perfectly competitive industry,which is made up of 50 identical firms.Assume that costs are constant in each interval;so,for example,the marginal cost of clearing each of the lots from 1 through 10 is $20.Also assume that she can only plow the quantities of the lots given in the table (and not numbers in between).Her only fixed cost is $1,000 for a snowplow.Her variable costs include fuel,her time,and hot coffee.Which point falls on the industry short-run supply curve?

(Multiple Choice)

4.9/5 (32)

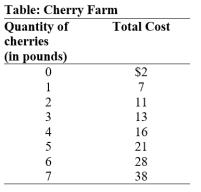

Use the following to answer question:  -(Table: Cherry Farm)Use Table: Cherry Farm.Suppose there are 100 farms in this industry with identical cost curves,as shown in the table.If the price is $10 per pound:

-(Table: Cherry Farm)Use Table: Cherry Farm.Suppose there are 100 farms in this industry with identical cost curves,as shown in the table.If the price is $10 per pound:

(Multiple Choice)

4.8/5 (30)

Use the following to answer question:

-(Table: Total Cost and Output)Use Table: Total Cost and Output,which describes Sergei's total costs for his perfectly competitive all-natural ice cream firm.Which point falls on Sergei's short-run supply curve (assuming he can only produce whole quantities of output)?

(Multiple Choice)

4.9/5 (29)

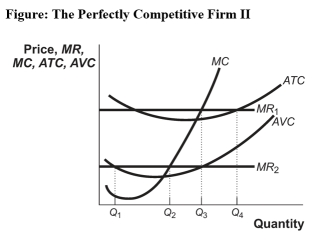

Use the following to answer question:  -(Figure: The Perfectly Competitive Firm II)Use Figure: The Perfectly Competitive Firm II.If this firm's MR curve is MR1,the firm will maximize profit by producing _____ units of output,and its economic profit will be _____.

-(Figure: The Perfectly Competitive Firm II)Use Figure: The Perfectly Competitive Firm II.If this firm's MR curve is MR1,the firm will maximize profit by producing _____ units of output,and its economic profit will be _____.

(Multiple Choice)

4.8/5 (33)

Use the following to answer question:

-(Table: Cherry Farm)Use Table: Cherry Farm.If Hank and Helen have one of 100 farms in the perfectly competitive cherry industry and if the price is $4,in the short run the industry will supply _____ pounds.

(Multiple Choice)

4.9/5 (29)

The market for beef is in long-run equilibrium at $3.25 per pound.The announcement that mad cow disease has been discovered in the United States reduces the demand for beef sharply,and the price falls to $2.00 per pound.If the long-run supply curve is horizontal,when the long-run equilibrium is reestablished,the price will be:

(Multiple Choice)

4.9/5 (38)

For the Colorado beef industry to be classified as perfectly competitive,ranchers in Colorado must have _____ on prices and beef must be a _____ product.

(Multiple Choice)

4.8/5 (32)

Use the following to answer question:

-(Table: Total Cost and Output)Use Table: Total Cost and Output,which describes Sergei's total costs for his perfectly competitive all-natural ice cream firm.What is the minimum price that Sergei needs to receive for a tub of ice cream to stay in business in the short run?

(Multiple Choice)

4.8/5 (29)

Suppose Sarah's pottery studio is charging the market price,which is slightly higher than her average total cost.This means that Sarah:

(Multiple Choice)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)