Exam 11: Output and Costs

Exam 1: What Is Economics479 Questions

Exam 2: The Economic Problem439 Questions

Exam 3: Demand and Supply515 Questions

Exam 4: Elasticity533 Questions

Exam 5: Efficiency and Equity449 Questions

Exam 6: Government Actions in Markets410 Questions

Exam 7: Global Markets in Action200 Questions

Exam 8: Utility and Demand364 Questions

Exam 9: Possibilities, Preferences, and Choices464 Questions

Exam 10: Organizing Production385 Questions

Exam 11: Output and Costs494 Questions

Exam 12: Perfect Competition487 Questions

Exam 13: Monopoly606 Questions

Exam 14: Monopolistic Competition320 Questions

Exam 15: Oligopoly280 Questions

Exam 16: Public Choices and Public Goods356 Questions

Exam 17: Externalities and the Environment284 Questions

Exam 18: Markets for Factors of Production382 Questions

Exam 19: Economic Inequality354 Questions

Exam 20: Uncertainty and Information233 Questions

Exam 21: Extension A: Review11 Questions

Exam 22: Extension B: Review25 Questions

Exam 23: Extension C: Review14 Questions

Exam 24: Extension D: Review38 Questions

Exam 25: Extension E: Review11 Questions

Exam 26: Extension F: Review18 Questions

Select questions type

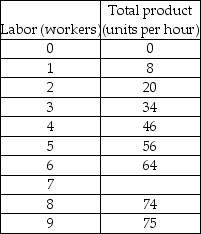

-In the above table, what is marginal product of labor for the 2nd worker?

-In the above table, what is marginal product of labor for the 2nd worker?

(Multiple Choice)

4.9/5  (38)

(38)

The marginal product of labor is defined as the increase in output attributable to the last worker hired divided by the total number of workers employed.

(True/False)

4.8/5 (42)

A firm's average total cost is $80, its fixed cost is $1000, and its output is 100 units. Its average variable cost

(Multiple Choice)

4.9/5 (35)

In August 2008, Toyota halted production of the Tundra, its full-size, gas-guzzling pick-up. Sales of the vehicle are down 15 percent and the production suspension could last for months. When production of the truck resumes, it'll be at a slower pace. If Toyota, like many car makers, experiences increasing returns to scale, what would happen to long run average cost if production resumed, but at a slower pace?

(Multiple Choice)

4.8/5 (38)

If marginal cost exceeds average variable cost but is less than average total cost, then as output increases average total cost ________ and average variable cost ________.

(Multiple Choice)

4.8/5 (36)

What is the difference between average total cost and marginal cost and are they ever equal to each other?

(Essay)

5.0/5 (39)

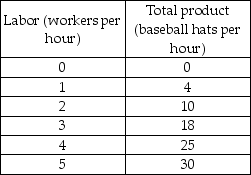

-The table above gives production information for Bob's Baseball Cap Company. Bob's total cost when zero caps are produced is $200 and workers cost $10 per hour. The total fixed cost of producing 10 baseball hats per hour is

-The table above gives production information for Bob's Baseball Cap Company. Bob's total cost when zero caps are produced is $200 and workers cost $10 per hour. The total fixed cost of producing 10 baseball hats per hour is

(Multiple Choice)

4.8/5 (40)

In the short run, average fixed cost is constant as output increases.

(True/False)

4.7/5 (38)

A company could produce 100 units of a good for $320 or produce 101 units of the same good for $324. The $4 difference in costs is

(Multiple Choice)

4.9/5 (27)

Ernie's Earmuffs produces 200 earmuffs per year at a total cost of $2,000 and $400 of this cost is fixed. If he increases output to 220 earmuffs, his total cost increases to $2100, and his fixed cost remains $400. What is Ernie's marginal cost per earmuff?

(Multiple Choice)

4.9/5 (35)

When long-run average cost decreases as output increases there are definitely

(Multiple Choice)

4.9/5 (32)

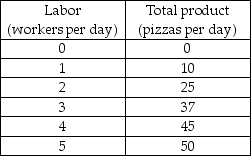

-Based on the production data for Pat's Pizza Parlor in the above table, the average product of labor when 4 workers are hired is ________ pizzas.

-Based on the production data for Pat's Pizza Parlor in the above table, the average product of labor when 4 workers are hired is ________ pizzas.

(Multiple Choice)

4.9/5 (30)

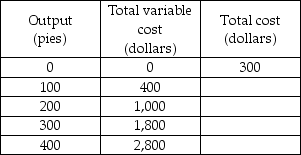

-The above table gives some of the costs of the Delicious Pie Company. What is the total fixed cost of producing 100 pies?

-The above table gives some of the costs of the Delicious Pie Company. What is the total fixed cost of producing 100 pies?

(Multiple Choice)

4.8/5 (36)

When long-run average costs decrease as output increases, there are

(Multiple Choice)

4.8/5 (33)

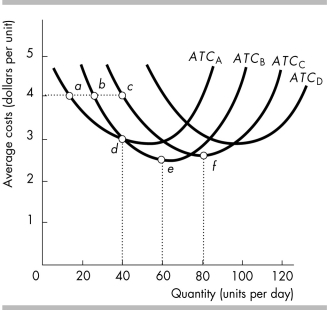

-The average total cost curves for plants A, B, C, and D are shown in the above figure. The plant size that is the most economically efficient

-The average total cost curves for plants A, B, C, and D are shown in the above figure. The plant size that is the most economically efficient

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)