Exam 8: Property Dispositions

Exam 1: Introduction to Taxation109 Questions

Exam 2: The Tax Practice Environment111 Questions

Exam 3: Determining Gross Income132 Questions

Exam 4: Employee Compensation101 Questions

Exam 5: Deductions for Individuals and Tax Determination120 Questions

Exam 6: Business Expenses116 Questions

Exam 7: Property Acquisitions and Cost Recovery Deductions114 Questions

Exam 8: Property Dispositions116 Questions

Exam 9: Tax-Deferred Exchanges112 Questions

Exam 10: Taxation of Corporations111 Questions

Exam 11: Sole Proprietorships and Flow-Through Entities133 Questions

Exam 12: Estates, Gifts, and Trusts116 Questions

Select questions type

In what order are capital gains subject to the 15%/20%, 25%, and 28% capital gains tax rates included in taxable income in the determination of the tax liability?

Free

(Essay)

4.9/5  (34)

(34)

Correct Answer: Verified

Verified

Taxpayers' capital gains that are subject to different rates must be included in the following order in taxable income: 25% asset capital gains are included first, 28% asset capital gains are included second, and 15%/20% asset capital gains are included last.

Carol used her auto 60 percent for business and 40 percent for personal use. She purchased it for $10,800 and has taken $3,992 of depreciation on it. What is her recognized gain on a sale for $7,800 and what is it character?

Free

(Multiple Choice)

4.9/5 (44)

Correct Answer:Verified

C

Gain representing depreciation recapture on equipment is taxed at ordinary income rates.

Free

(True/False)

4.9/5 (43)

Correct Answer:Verified

True

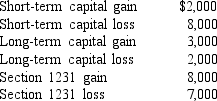

Taxpayer B has the following gains and losses from property transactions. What is the effect on the taxpayer's taxable income if Taxpayer B is (a) a corporation; (b) an individual?

Long-term capital gain $6,000

Long-term capital loss 20,000

Section 1231 gain 8,000

Section 1231 loss 5,000

Short-term capital gain 23,000

Short-term capital loss 6,000

(Essay)

4.9/5 (38)

Identify the type(s) of gain or loss that would be recognized on the following asset sales as capital, Section 1231, ordinary, Section 1245 recapture, Section 291 recapture, or Section 1250 unrecaptured gain.

-Lopez Corporation sold equipment that is had purchased for $300,000 ($100,000 cash and a note for $200,000) four years ago.. As of the date of sale, Lopez had claimed $187,500 in accumulated depreciation on this equipment and had made $50,000 in principal payments on the note. Lopez received $80,000 cash and a note for $100,000 in addition to the purchaser assuming Lopez's $150,000 note on the equipment. What is Lopez Corporation's realized gain on the sale?

(Multiple Choice)

4.7/5 (37)

During the current year, Zach had taxable income of $100,000 before considering the following property transactions:  Two years ago Zach had a $4,000 gain from the sale of a Section 1231 asset but last year Zach had no capital or Section 1231 gains or losses. What effect will the above property transactions have on Zach current taxable income and will there be any carryforward or carryback of gains or losses?

Two years ago Zach had a $4,000 gain from the sale of a Section 1231 asset but last year Zach had no capital or Section 1231 gains or losses. What effect will the above property transactions have on Zach current taxable income and will there be any carryforward or carryback of gains or losses?

(Multiple Choice)

4.8/5 (38)

On March 17, a calendar-year taxpayer sells a machine used in its business for $9,500. The machine was purchased sixteen months earlier for $9,000 and depreciation deductions of $1,800 have been taken. What is the amount and type of gain recognized on the sale?

(Multiple Choice)

4.7/5 (39)

George and Sally sold their primary residence in New Jersey on January 1, 2016 after having lived in the home for 20 years. (They used their $500,000 exclusion to avoid recognizing their $289,000 gain on the sale.) They decided to become permanent Florida residents and moved into the condominium they had purchased on January 2, 2014 at a foreclosure auction. Unfortunately, Sally missed all of her friends and family in New Jersey and in the latter part of 2018, they put the condominium up for sale and they sold it on January 2, 2019. They had purchased the condominium for only $65,000 and after putting in improvements at a cost of $21,000, they were able to sell it for $525,000. What is their realized and recognized gain on the sale of the condominium?

(Essay)

4.8/5 (39)

Shawn, a single taxpayer, sold the house he lived in for seven years for $700,000. He purchased the house for $285,000. He made improvements at a cost of $125,000 and paid a $30,000 commission on the sale. What are Shawn's realized and recognized gains on the sale?

(Multiple Choice)

4.9/5 (35)

Identify the type(s) of gain or loss that would be recognized on the following asset sales as capital, Section 1231, ordinary, Section 1245 recapture, Section 291 recapture, or Section 1250 unrecaptured gain.

-The following properties have been owned by a business for more than one year. Which of them would not qualify for Section 1231 treatment on its disposal?

(Multiple Choice)

4.9/5 (35)

A gain must be recognized unless some tax provision allows nonrecognition or deferral.

(True/False)

4.9/5 (35)

Craig and Sally, a married couple, file a joint tax return and report taxable income (excluding their home sale) of $325,000 for 2018. They purchased their home on December 1, 2016 for $250,000 and have made $100,000 of improvements during the time they owned the home. They sold the home on May 31, 2018 after Craig accepted a job in another state netting $775,000 after the expenses of the sale. What are the tax consequences of this sale?

(Essay)

4.9/5 (37)

A taxpayer's initial investment in Section 1202 stock is limited to $1 million.

(True/False)

4.9/5 (50)

An individual's net Section 1231 gain is given the tax-favored treatment of a long-term capital asset.

(True/False)

4.9/5 (30)

A mixed-use asset is an asset that is used for both personal purposes and business activities.

(True/False)

4.8/5 (40)

The most common ordinary income assets are receivables and inventory.

(True/False)

4.9/5 (43)

Ian and Mia married in early 2018 and purchased a new home together. Each owned and lived in separate residences prior to the marriage. Ian purchased his residence 5 years ago for $190,000 and he added a master bedroom and bathroom addition at a cost of $40,000. Mia purchased her home three years ago for $135,000. In late 2018, Ian sold his residence for $510,000 and paid a sales commission of $8,000. After paying off his $80,000 mortgage balance, he received the remaining cash proceeds of $422,000. In late 2018 Mia sold her residence for $190,000 and paid a sales commission of $2,000. She had paid off her mortgage so she received $188,000 cash from the sale. If Ian and Mia file a joint tax return for 2018, how much gain do they recognize on their 2018 joint tax return from the sales of their previous homes?

(Multiple Choice)

4.9/5 (43)

Tina is single and one of the founding shareholders of Exacta Corporation. She acquired her Exacta Section 1244 stock four years ago for $123,000. During the current year, Tina sold all of her Exacta stock to an unrelated party for $40,000. Tina had no other capital gains or losses during the year. What is the maximum amount of loss Tina can deduct in the current year for the Exacta stock?

(Multiple Choice)

4.8/5 (44)

Identify the type(s) of gain or loss that would be recognized on the following asset sales as capital, Section 1231, ordinary, Section 1245 recapture, Section 291 recapture, or Section 1250 unrecaptured gain.

-A business sells a machine used in its business for $18,000. It had purchased the machine 10 months earlier for $26,000. What is the amount and type of the $8,000 loss on the sale of the asset?

(Multiple Choice)

4.9/5 (35)

All losses on Section 1244 stock are deductible in the year realized.

(True/False)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)