Exam 13: Financial Statements and Closing Procedures

Exam 1: Accounting: the Language of Business82 Questions

Exam 2: Analyzing Business Transactions93 Questions

Exam 3: Analyzing Business Transactions Using T Accounts107 Questions

Exam 4: The General Journal and the General Ledger85 Questions

Exam 5: Adjustments and the Worksheet76 Questions

Exam 6: Closing Entries and the Postclosing Trial Balance80 Questions

Exam 7: Accounting for Sales and Accounts Receivable76 Questions

Exam 8: Accounting for Purchases and Accounts Payable89 Questions

Exam 9: Cash Receipts, Cash Payments, and Banking Procedures88 Questions

Exam 10: Payroll Computations, Records, and Payment79 Questions

Exam 11: Payroll Taxes, Deposits, and Reports82 Questions

Exam 12: Accruals, Deferrals, and the Worksheet84 Questions

Exam 13: Financial Statements and Closing Procedures38 Questions

Exam 14: Accounting Principles and Reporting Standards67 Questions

Exam 15: Accounts Receivable and Uncollectible Accounts65 Questions

Exam 16: Notes Payable and Notes Receivable83 Questions

Exam 17: Merchandise Inventory91 Questions

Exam 18: Property, Plant, and Equipment118 Questions

Exam 19: Accounting for Partnerships106 Questions

Exam 20: Corporations: Formation and Capital Stock Transactions76 Questions

Exam 21: Corporate Earnings and Capital Transactions99 Questions

Exam 22: Long-Term Bonds105 Questions

Exam 23: Financial Statement Analyses107 Questions

Exam 24: The Statement of Cash Flows114 Questions

Exam 25: Departmentalized Profit and Cost Centers103 Questions

Exam 26: Accounting for Manufacturing Activities103 Questions

Exam 27: Job Order Cost Accounting102 Questions

Exam 28: Process Cost Accounting94 Questions

Exam 29: Controlling Manufacturing Costs: Standard Costs118 Questions

Exam 30: Cost-Revenue Analysis for Decision Making124 Questions

Select questions type

An income statement that has one total for all revenues and one total for all expenses is known as a

(Multiple Choice)

4.9/5  (41)

(41)

Current assets provide the funds needed to pay bills and meet expenses.

(True/False)

4.8/5 (37)

The balance of the Sales Returns and Allowances account is reported as a selling expense in Operating Expenses section of a multiple-step income statement.

(True/False)

4.8/5 (35)

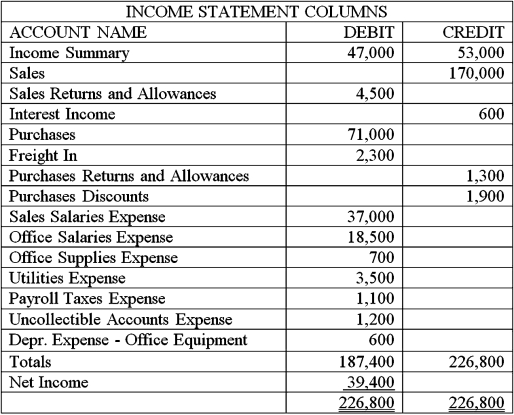

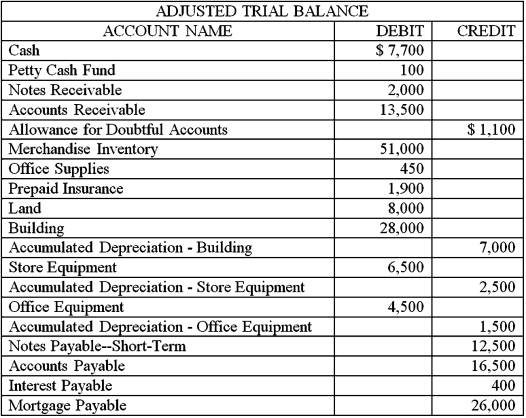

Use the following account balances from the adjusted trial balance columns of Goody Chocolate's worksheet to answer below question.  Using the adjusted trial balance above,select the correct closing entry that Goody Chocolate would make to close their revenue accounts (and other temporary income statement accounts with credit balances)at the end of the accounting period.

Using the adjusted trial balance above,select the correct closing entry that Goody Chocolate would make to close their revenue accounts (and other temporary income statement accounts with credit balances)at the end of the accounting period.

(Multiple Choice)

4.9/5 (37)

If the Income Summary account has a credit balance after revenues,and expenses are closed,the firm had a net income for the fiscal period.

(True/False)

4.9/5 (41)

When a firm experiences a net loss,the owner's capital is decreased.

(True/False)

4.9/5 (38)

A total of $8,000 in supplies was purchased during the year.By the end of the year,the company had used up $5,300 of the supplies.The adjusting entry needed at the end of the year is:

(Multiple Choice)

4.9/5 (30)

The ____________________ of a building is the portion of the original cost that has not yet been depreciated.

(Essay)

4.8/5 (38)

Interest on notes payable would be listed in the Other Income section of a classified income statement.

(True/False)

4.9/5 (35)

Use the following account balances from the adjusted trial balance columns of RB Auto's worksheet to answer below question.  Select the closing entry that RB Auto would make at the end of the accounting period to close their revenue accounts and income statement accounts with credit balances.

Select the closing entry that RB Auto would make at the end of the accounting period to close their revenue accounts and income statement accounts with credit balances.

(Multiple Choice)

4.7/5 (44)

A gross profit percentage of 45 percent means that for every $1 of net sales,gross profit amounts to ___________________.

(Essay)

4.9/5 (40)

Use the following account balances from the adjusted trial balance columns of Goody Chocolate's worksheet to answer below question.  Using the adjusted trial balance above,select the correct closing entry that Goody Chocolate would make to close the expense accounts (and cost of goods sold accounts with debit balances)at the end of the accounting period.

Using the adjusted trial balance above,select the correct closing entry that Goody Chocolate would make to close the expense accounts (and cost of goods sold accounts with debit balances)at the end of the accounting period.

(Multiple Choice)

4.9/5 (31)

The beginning capital balance shown on a statement of owner's equity is $43,000.Net income for the period is $18,000.The owner withdrew $22,000 cash from the business and made no additional investments during the period.The owner's capital balance at the end of the period is

(Multiple Choice)

5.0/5 (32)

After all adjusting entries are posted,the balances of the general ledger accounts should match the amounts shown in the Adjusted Trial Balance section of the worksheet.

(True/False)

4.7/5 (36)

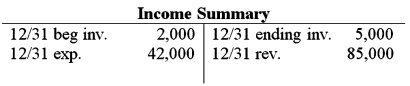

The accountant of Randy's Flooring has closed all of the temporary income statement accounts.The accountant is now ready to close the Income Summary account.Using the Income Summary T-account below,determine the correct closing entry the accountant needs to make in order to close the account.

(Multiple Choice)

4.8/5 (33)

Use the following account balances from the adjusted trial balance columns of RB Auto's worksheet to answer below question.  Select the correct closing entry that RB Auto would make to close their expense account(s)at the end of the accounting period.

Select the correct closing entry that RB Auto would make to close their expense account(s)at the end of the accounting period.

(Multiple Choice)

4.7/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)