Exam 2: Consolidated Statements: Date of Acquisition

Discuss the conditions under which the FASB would assume a presumption of control. Additionally, under what circumstances might the FASB require consolidation even though the parent does not control the subsidiary?

The FASB presumes that control exists if one company owns over 50% of the voting interest in another company or has an unconditional right to appoint a majority of the members of another company's controlling body. Additionally, in the absence of evidence to the contrary, one or more of the following conditions would lead to a presumption of control:

1.Ownership of a large noncontrolling interest where no other party has a significant interest.

2.Ownership of securities or unconditional rights in the company that can be converted into securities that would cause a controlling interest to exist.

3.The acquiring company has the unconditional right to dissolve the entity whose interest was acquired and assume control of the assets.

4.A relationship with another entity that assures control through provisions in a charter, bylaws, or trust agreement.

5.A legal obligation created with the controlled entity that requires substantially all cash flows and other economic benefits to flow to the controlling entity.

6.A sole general partner in a limited partnership where no other party may dissolve the partnership or remove the general partner.

The goal of the consolidation process is for:

A

Pagach Company purchased 100% of the voting common stock of Rage Company for $1,800,000. The following book and fair values are available:  The bonds payable will appear on the consolidated balance sheet

The bonds payable will appear on the consolidated balance sheet

B

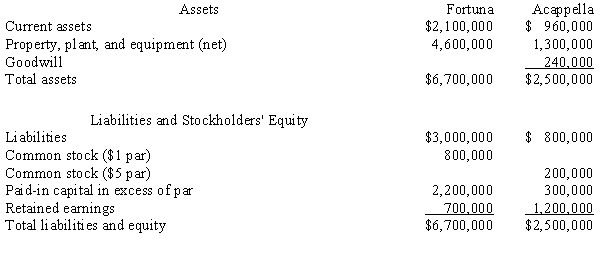

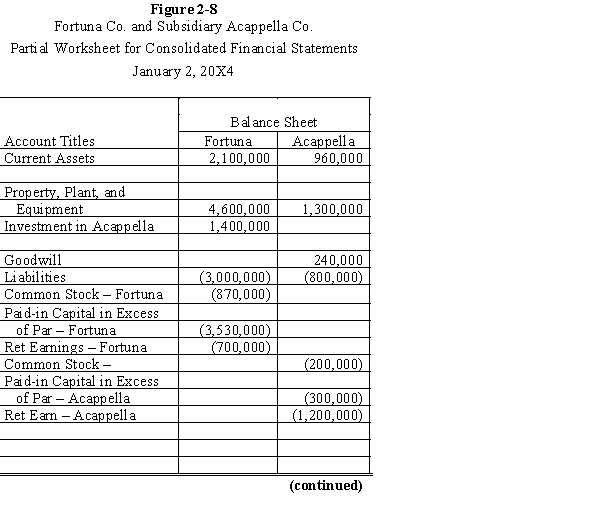

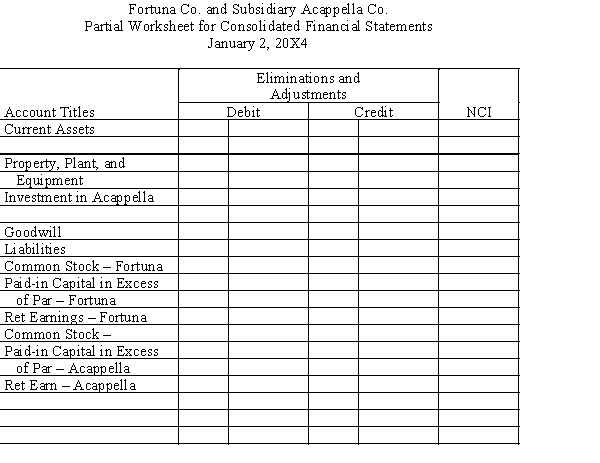

Fortuna Company issued 70,000 shares of $1 par stock, with a fair value of $20 per share, for 80% of the outstanding shares of Acappella Company. The firms had the following separate balance sheets prior to the acquisition:

Book values equal fair values for the assets and liabilities of Acappella Company, except for the property, plant, and equipment, which has a fair value of $1,600,000.

Required:

a.

Prepare a value analysis schedule

b.

Prepare a determination and distribution of excess schedule.

c.

Provide all eliminations on the partial balance sheet worksheet provided in Figure 2-8 and complete the noncontrolling interest column.

Book values equal fair values for the assets and liabilities of Acappella Company, except for the property, plant, and equipment, which has a fair value of $1,600,000.

Required:

a.

Prepare a value analysis schedule

b.

Prepare a determination and distribution of excess schedule.

c.

Provide all eliminations on the partial balance sheet worksheet provided in Figure 2-8 and complete the noncontrolling interest column.

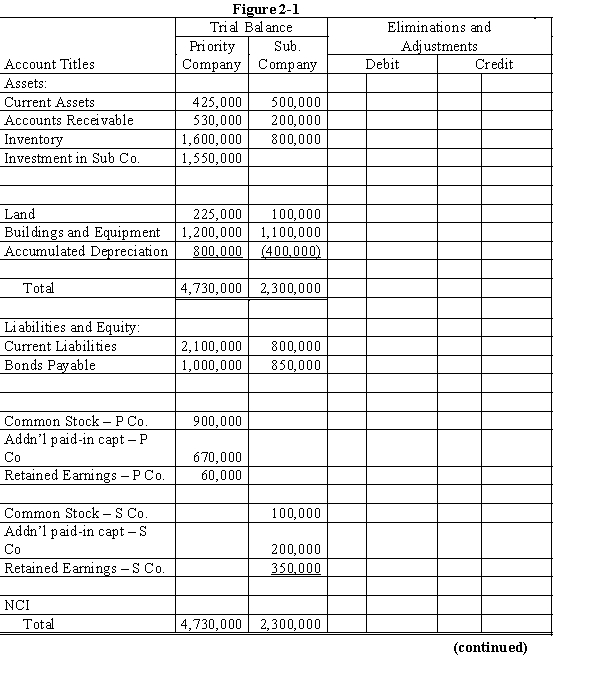

On December 31, 20X1, Priority Company purchased 80% of the common stock of Subsidiary Company for $1,550,000. On this date, Subsidiary had total owners' equity of $650,000 (common stock $100,000; other paid-in capital, $200,000; and retained earnings, $350,000). Any excess of cost over book value is due to the under or overvaluation of certain assets and liabilities. Assets and liabilities with differences in book and fair values are provided in the following table:

Remaining excess, if any, is due to goodwill.

Required:

a.

Using the information above and on the separate worksheet, prepare a schedule to determine and distribute the excess of cost over book value.

b.

Complete the Figure 2-1 worksheet for a consolidated balance sheet as of December 31, 20X1.

Remaining excess, if any, is due to goodwill.

Required:

a.

Using the information above and on the separate worksheet, prepare a schedule to determine and distribute the excess of cost over book value.

b.

Complete the Figure 2-1 worksheet for a consolidated balance sheet as of December 31, 20X1.

In an 80% purchase accounted for as a tax-free exchange, the excess of cost over book value is $200,000. The equipment's book value for tax purposes is $100,000 and its fair value is $150,000. All other identifiable assets and liabilities have fair values equal to their book values. The tax rate is 30%. What is the total deferred tax liability that should be recognized on the consolidated balance sheet on the date of purchase?

Consolidated financial statements are appropriate even without a majority ownership if which of the following exists:

Paro Company purchased 80% of the voting common stock of Sabon Company for $900,000. There are no liabilities. The following book and fair values are available for Sabon:  The machinery will appear on the consolidated balance sheet at ____.

The machinery will appear on the consolidated balance sheet at ____.

A subsidiary was acquired for cash in a business combination on December 31, 20X1. The purchase price exceeded the fair value of identifiable net assets. The acquired company owned equipment with a fair value in excess of the book value as of the date of the combination. A consolidated balance sheet prepared on December 31, 20X1, would

When it purchased Sutton, Inc. on January 1, 20X1, Pavin Corporation issued 500,000 shares of its $5 par voting common stock. On that date the fair value of those shares totaled $4,200,000. Related to the acquisition, Pavin had payments to the attorneys and accountants of $200,000, and stock issuance fees of $100,000. Immediately prior to the purchase, the equity sections of the two firms appeared as follows:  Immediately after the purchase, the consolidated balance sheet should report paid-in capital in excess of par of

Immediately after the purchase, the consolidated balance sheet should report paid-in capital in excess of par of

The investment in a subsidiary should be recorded on the parent's books at the

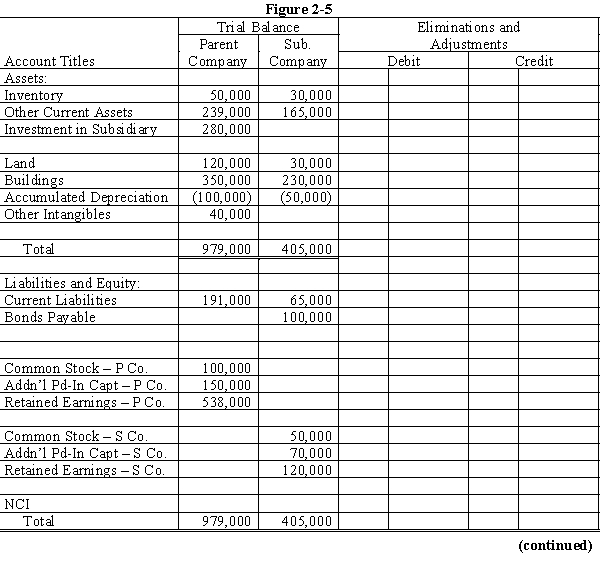

On January 1, 20X1, Parent Company purchased 100% of the common stock of Subsidiary Company for $280,000. On this date, Subsidiary had total owners' equity of $240,000.

On January 1, 20X1, the excess of cost over book value is due to a $15,000 undervaluation of inventory, to a $5,000 overvaluation of Bonds Payable, and to an undervaluation of land, building and equipment. The fair value of land is $50,000. The fair value of building and equipment is $200,000. The book value of the land is $30,000. The book value of the building and equipment is $180,000.

Required:

a.

Using the information above and on the separate worksheet, complete a value analysis schedule

b.

Complete schedule for determination and distribution of the excess of cost over book value.

c.

Complete the Figure 2-5 worksheet for a consolidated balance sheet as of January 1, 20X1.

The SEC requires the use of push-down accounting in some specific situations. Push-down accounting results in:

A parent company purchases an 80% interest in a subsidiary at a price high enough to revalue all assets and allow for goodwill on the interest purchased. If "push down accounting" were used in conjunction with the "economic entity concept," what unique procedures would be used?

Judd Company issued nonvoting preferred stock with a fair value of $1,500,000 in exchange for all the outstanding common stock of the Bath Corporation. On the date of the exchange, Bath had tangible net assets with a book value of $900,000 and a fair value of $1,400,000. In addition, Judd issued preferred stock valued at $100,000 to an individual as a finder's fee for arranging the transaction. As a result of these transactions, Judd should report an increase in net assets of ____.

On June 30, 20X1, Naeder Corporation purchased for cash at $10 per share all 100,000 shares of the outstanding common stock of the Tedd Company. The total fair value of all identifiable net assets of Tedd was $1,400,000. The only noncurrent asset is property with a fair value of $350,000. The consolidated balance sheet of Naeder and its wholly owned subsidiary on June 30, 20X1, should report

The SEC and FASB has recommended that a parent corporation should consolidate the financial statements of the subsidiary into its financial statements when it exercises control over the subsidiary, even without majority ownership. In which of the following situations would control NOT be evident?

When a company purchases another company that has existing goodwill and the transaction is accounted for as a stock acquisition, the goodwill should be treated in the following manner.

Assuming Investor owns 70% of Investee. What is the amount that will be recorded as Net Income for the Controlling Interest?

Assuming Investor owns 70% of Investee. What is the amount that will be recorded as Net Income for the Controlling Interest?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)