Exam 7: Special Issues in Accounting for an Investment in a Subsidiary

Exam 1: Business Combinations: New Rules for a Long-Standing Business Practice32 Questions

Exam 2: Consolidated Statements: Date of Acquisition29 Questions

Exam 3: Consolidated Statements: Subsequent to Acquisition30 Questions

Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes29 Questions

Exam 5: Intercompany Transactions: Bonds and Leases54 Questions

Exam 6: Cash Flow, Eps, and Taxation44 Questions

Exam 7: Special Issues in Accounting for an Investment in a Subsidiary35 Questions

Exam 8: Subsidiary Equity Transactions; Indirect and Mutual Holdings36 Questions

Exam 9: The International Accounting Environment28 Questions

Exam 10: Foreign Currency Transactions61 Questions

Exam 11: Translation of Foreign Financial Statements62 Questions

Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise50 Questions

Exam 13: Partnerships: Characteristics, Formation, and Accounting for Activities32 Questions

Exam 14: Partnerships: Ownership Changes and Liquidations48 Questions

Exam 15: Governmental Accounting: the General Fund and the Account Groups53 Questions

Exam 16: Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds43 Questions

Exam 17: Financial Reporting Issues29 Questions

Exam 18: Accounting for Private Not-For-Profit Organizations45 Questions

Exam 19: Accounting for Not-For-Profit Colleges and Universities and Health Care Organizations64 Questions

Exam 20: Estates and Trusts: Their Nature and the Accountants Role46 Questions

Exam 21: Debt Restructuring, Corporate Reorganizations, and Liquidations44 Questions

Select questions type

Control of a subsidiary was achieved with the initial investment in subsidiary stock. When a subsequent block of subsidiary's stock is purchased

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

C

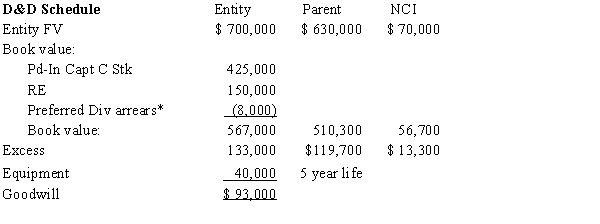

Pilatte Company acquired a 90% interest in the common stock of Sweet Company for $630,000 on January 1, 20X3, when Sweet Company had the following stockholders' equity:

The preferred stock dividends are 2 years in arrears. Any excess is attributable to equipment with a 6-year life, which is undervalued by $40,000, and to goodwill.

Required:

Prepare a determination and distribution of excess schedule for the investment in Sweet Company.

The preferred stock dividends are 2 years in arrears. Any excess is attributable to equipment with a 6-year life, which is undervalued by $40,000, and to goodwill.

Required:

Prepare a determination and distribution of excess schedule for the investment in Sweet Company.

Free

(Essay)

4.8/5 (30)

Correct Answer:Verified

*$80,000 *5% * 2 years = $8,000

*$80,000 *5% * 2 years = $8,000

Parent has purchased additional shares of subsidiary stock. If the original investment blocks are carried at cost, the conversion to simple equity is based upon

Free

(Multiple Choice)

4.8/5 (31)

Correct Answer:Verified

C

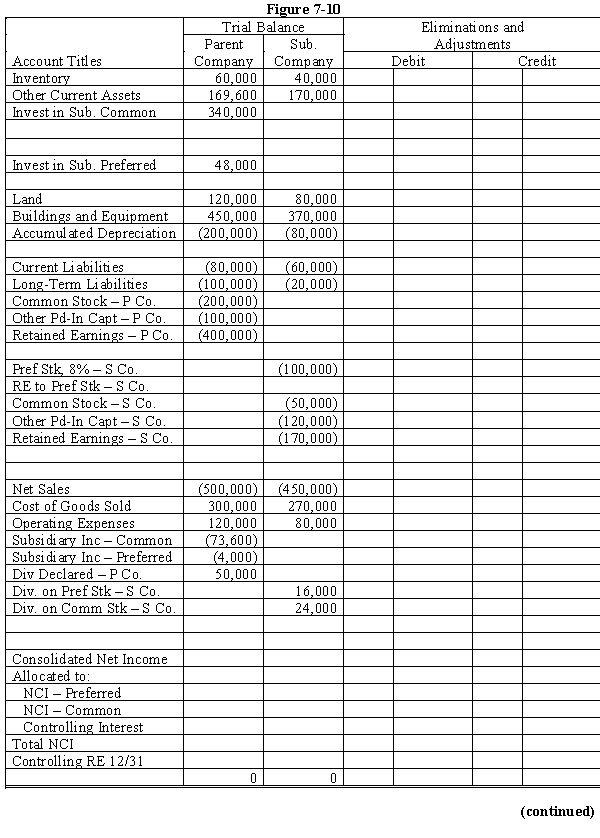

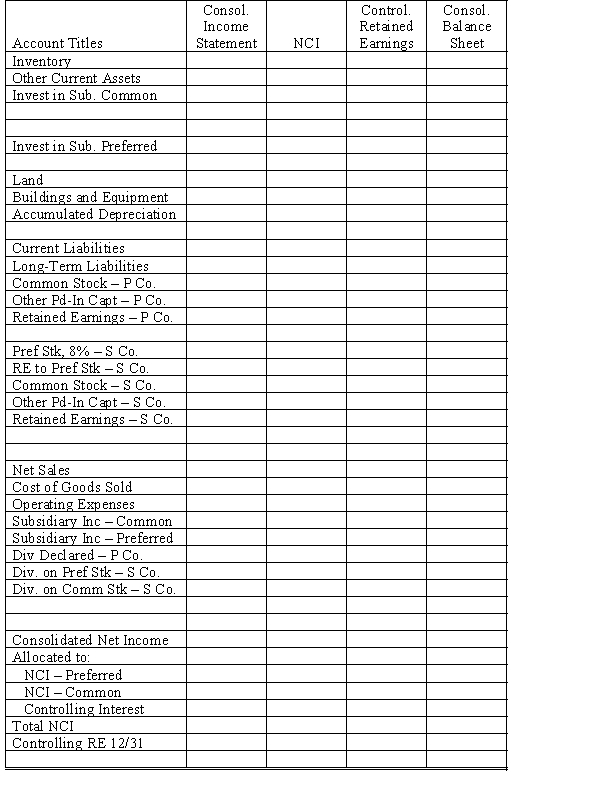

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $300,000. Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years.

On this date, Subsidiary had total shareholders' equity as follows:

8\% Preferred Stock, \ 100 par \ 100,000 Common Stock, \ 10 par 50,000 Other Paid-in Capital 120,000 Retained Earnings \ 180,000 Total \ 450,000 The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears. There were no preferred dividends in arrears on January 1, 20X1.

During 20X1, Subsidiary had a net loss of $10,000 and paid no dividends. In 20X2, Subsidiary had net income of $100,000 and paid dividends, on preferred and common, totaling $40,000.

On January 1, 20X2, Parent purchased $50,000 par value of Subsidiary's preferred stock for $52,000. At year end, the preferred is still held as an investment.

In 20X1 and 20X2, Parent has accounted for its investments in Subsidiary's preferred and common using the simple equity method.

During 20X2, Subsidiary sold merchandise to Parent for $40,000, of which $15,000 is still held by Parent on December 31, 20X2. Subsidiary's usual gross profit is 40%.

Required:

Complete the Figure 7-10 worksheet for consolidated financial statements for the year ended December 31, 20X2.

(Essay)

4.8/5 (32)

Page & Seed scenario:

Page Company purchased an 80% interest in the common stock of the Seed Company for $600,000 on January 1, 20X4, when Seed Company had the following stockholders' equity:

Any excess of cost over book value on the common stock purchase was attributed to goodwill. Page does not hold any of Seed's preferred stock. Seed had net income of $40,000 during 20X4 and paid no dividends.

-Refer to Page and Seed. The preferred stock is 1 year in arrears on January 1, 20X4. The goodwill that will appear on the consolidated balance sheet prepared on January 1, 20X4, is ____.

Any excess of cost over book value on the common stock purchase was attributed to goodwill. Page does not hold any of Seed's preferred stock. Seed had net income of $40,000 during 20X4 and paid no dividends.

-Refer to Page and Seed. The preferred stock is 1 year in arrears on January 1, 20X4. The goodwill that will appear on the consolidated balance sheet prepared on January 1, 20X4, is ____.

(Multiple Choice)

4.7/5 (42)

Page & Seed scenario:

Page Company purchased an 80% interest in the common stock of the Seed Company for $600,000 on January 1, 20X4, when Seed Company had the following stockholders' equity:

Any excess of cost over book value on the common stock purchase was attributed to goodwill. Page does not hold any of Seed's preferred stock. Seed had net income of $40,000 during 20X4 and paid no dividends.

-Refer to Page and Seed. The preferred stock is 2 years in arrears on January 1, 20X4. The controlling interest's share of Seed's 20X4 net income is ____.

(Multiple Choice)

4.9/5 (29)

Pine & Scent scenario:

Pine Company purchased a 60% interest in the Scent Company on January 1, 20X1 for $360,000. On that date, the stockholders' equity of Scent Company was $450,000. Any excess cost on 1/1/X1 was attributable to goodwill. Pine purchased another 20% interest on January 1, 20X4 for $200,000. On January 1, 20X4, Scent Company's stockholders' equity was $700,000, the entire increase due to retained earnings.

-Refer to the Pine and Scent scenario. As part of the consolidation process, the excess of cost over book on the new block of shares is treated as

(Multiple Choice)

4.9/5 (34)

Company P owns an 90% interest in Company S. Company S has outstanding $100,000 of 10% bonds that were sold at face value and have 6 years to maturity as of the balance sheet date. Company P owns $70,000 of the bonds and has a remaining unamortized book value of $66,000. Company S bonds will be presented on the consolidated balance sheet as

(Multiple Choice)

4.9/5 (40)

Which of the following statements is incorrect regarding a parent's purchase of additional subsidiary shares?

(Multiple Choice)

4.9/5 (39)

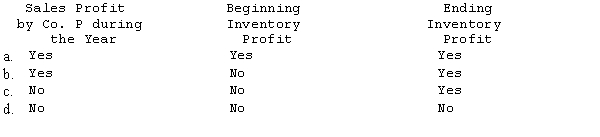

Company P has consistently sold merchandise for resale to its subsidiary at a gross profit of 20%. There were intercompany goods in both the subsidiary's beginning and ending inventory. As a result of these sales, which of the following amounts must be adjusted for when preparing only a consolidated balance sheet?

(Short Answer)

4.8/5 (43)

When a parent sells its subsidiary interest, a gain (loss) is recognized if the parent

(Short Answer)

4.7/5 (34)

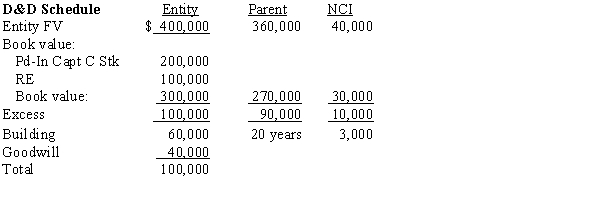

On January 1, 20X1, Company P purchased a 90% interest in Company S for $360,000. Company P prepared the following determination and distribution of excess schedule at that time:

Company S had income of $30,000 for 20X1 and $40,000 for 20X2. No dividends were paid. Company P sold its entire investment in Company S on January 1, 20X3, for $340,000.

Required:

Prepare Company P's entries to record the sale assuming that Company P used the

a.

simple equity method to reflect its investment in Company S.

b.

cost method to reflect its investment in Company S.

Company S had income of $30,000 for 20X1 and $40,000 for 20X2. No dividends were paid. Company P sold its entire investment in Company S on January 1, 20X3, for $340,000.

Required:

Prepare Company P's entries to record the sale assuming that Company P used the

a.

simple equity method to reflect its investment in Company S.

b.

cost method to reflect its investment in Company S.

(Essay)

4.8/5 (37)

Saddle Corporation is an 80%-owned subsidiary of Paso Company. On January 1, 20X1, Saddle sold Paso a machine for $50,000. Saddle's cost was $60,000 and the book value was $40,000. The machine had a 5-year remaining life at the time of the sale. A consolidated balance sheet only is being prepared on December 31, 20X3. The retained earnings of the controlling interest requires which of the following adjustments?

(Multiple Choice)

4.8/5 (34)

A new subsidiary is being formed. The parent company purchased 70% of the shares for $20 per share. The remaining shares were sold to a variety of outside interests for an average of $18 per share. The consolidated statements will show

(Multiple Choice)

4.8/5 (37)

In the year a parent sells its subsidiary investment, the results of subsidiary operations prior to the sale date are

(Multiple Choice)

4.8/5 (33)

Pine & Scent scenario:

Pine Company purchased a 60% interest in the Scent Company on January 1, 20X1 for $360,000. On that date, the stockholders' equity of Scent Company was $450,000. Any excess cost on 1/1/X1 was attributable to goodwill. Pine purchased another 20% interest on January 1, 20X4 for $200,000. On January 1, 20X4, Scent Company's stockholders' equity was $700,000, the entire increase due to retained earnings.

-Refer to the Pine and Scent scenario. The goodwill balance on the December 31, 20X4, balance sheet is ____.

(Multiple Choice)

4.8/5 (38)

Page & Seed scenario:

Page Company purchased an 80% interest in the common stock of the Seed Company for $600,000 on January 1, 20X4, when Seed Company had the following stockholders' equity:

Any excess of cost over book value on the common stock purchase was attributed to goodwill. Page does not hold any of Seed's preferred stock. Seed had net income of $40,000 during 20X4 and paid no dividends.

-Refer to Page and Seed. The preferred stock is 2 years in arrears on January 1, 20X4. The noncontrolling interest share of 20X4 net income was ____.

(Multiple Choice)

4.8/5 (22)

Partridge & Sparrow scenario:

Partridge purchased a 60% interest in Sparrow on January 1, 20X1, for $240,000. At the time of the purchase, Sparrow had the following stockholders' equity:

Any excess is attributable to equipment with a 10-year life. On January 1, 20X6, the retained earnings of Sparrow was $175,000.

-Refer to Partridge and Sparrow. The entire investment was sold for $300,000 on January 1, 20X6. The gain was ____.

Any excess is attributable to equipment with a 10-year life. On January 1, 20X6, the retained earnings of Sparrow was $175,000.

-Refer to Partridge and Sparrow. The entire investment was sold for $300,000 on January 1, 20X6. The gain was ____.

(Multiple Choice)

4.8/5 (28)

It is common for a parent firm to record its investment in a subsidiary under either the cost or simple equity method to expedite the elimination process. This does create some complications, however, when all or a portion of the investment is sold. Assume that in each of the following cases, the parent sells its investment midway through its fiscal year.

(1)

The parent owned an 80% interest and sold all of its holdings.

(2)

The parent owned an 80% interest and sold a 20% interest to reduce its ownership percentage to 60%.

(3)

The parent owned an 80% interest and sold a 60% interest to reduce its ownership percentage to 20%.

Required:

a.

For each of the above cases, comment on the procedures necessary to record the sale, where the investment is carried under simple equity, and the impact on consolidated income of the sale.

b.

For each of the above cases, state the added procedures that would be necessary if the investment was recorded under the cost method.

(Essay)

4.7/5 (41)

When a subsequent block of an existing subsidiary's stock is purchased,

(Multiple Choice)

5.0/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)