Exam 16: Expectations Theory and the Economy

Exam 1: What Economics Is About168 Questions

Exam 2: Production Possibilities Frontier Framework152 Questions

Exam 3: Supply and Demand: Theory227 Questions

Exam 4: Prices: Free, Controlled, and Relative107 Questions

Exam 5: Supply, Demand, and Price: Applications83 Questions

Exam 6: Macroeconomic Measurements: Prices and Unemployment129 Questions

Exam 7: Macroeconomic Measurements: GDP and Real GDP138 Questions

Exam 8: Aggregate Demand and Aggregate Supply208 Questions

Exam 9: Classical Macroeconomics and the Self Regulating Economy167 Questions

Exam 10: Keynesian Macroeconomics and Economic Instability: A Critique of the Self-Regulating Economy198 Questions

Exam 11: Fiscal Policy and the Federal Budget164 Questions

Exam 12: Money, Banking,and the Financial System124 Questions

Exam 13: The Federal Reserve System184 Questions

Exam 14: Money and the Economy125 Questions

Exam 15: Monetary Policy176 Questions

Exam 16: Expectations Theory and the Economy146 Questions

Exam 17: Economic Growth: Resources, Technology, Ideas, and Institutions82 Questions

Exam 18: The Financial Crisis of 2007-200970 Questions

Exam 19: Debates in Macroeconomics Over the Role and Effects of Government69 Questions

Exam 20: Elasticity198 Questions

Exam 21: Consumer Choice: Maximizing Utility and Behavioral Economics176 Questions

Exam 22: Production and Costs247 Questions

Exam 23: Perfect Competition191 Questions

Exam 24: Monopoly191 Questions

Exam 25: Monopolistic Competition, Oligopoly, and Game Theory167 Questions

Exam 26: Government and Product Markets: Antitrust and Regulation165 Questions

Exam 27: Factor Markets: With Emphasis on the Labor Market181 Questions

Exam 28: Wages,Unions,and Labor134 Questions

Exam 29: The Distribution of Income and Poverty93 Questions

Exam 30: Interest, Rent, and Profit199 Questions

Exam 31: Market Failure: Externalities, Public Goods, and Asymmetric Information185 Questions

Exam 32: Public Choice and Special-Interest-Group Politics131 Questions

Exam 33: Building Theories to Explain Everyday Life: From Observations to Questions to Theories to Predictions60 Questions

Exam 34: International Trade152 Questions

Exam 35: International Finance119 Questions

Exam 36: Globalization and International Impacts on the Economy136 Questions

Exam 37: The Economic Case For and Against Government: Five Topics Considered82 Questions

Exam 38: Stocks, Bonds, Futures, and Options108 Questions

Exam 39: Agriculture: Problems, Policies, and Unintended Effects149 Questions

Select questions type

In which of the following economic theories is it possible for an increase in the money supply to lead to a decrease in Real GDP in the short run?

(Multiple Choice)

4.8/5  (27)

(27)

According to Milton Friedman,there are two Phillips curves,a short-run one and a long-run one.

(True/False)

4.8/5 (36)

The Samuelson-Solow version of the Phillips curve showed the relationship between unemployment rates and

(Multiple Choice)

4.8/5 (44)

One implication of the policy ineffectiveness proposition (PIP)is that expansionary __________ policy is not effective at raising __________.

(Multiple Choice)

4.8/5 (26)

An increase in the actual inflation rate is represented by a

(Multiple Choice)

4.9/5 (42)

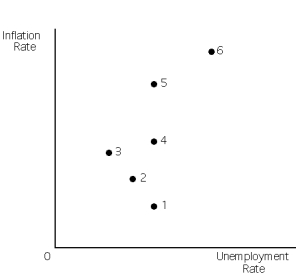

Exhibit 16-5

-Refer to Exhibit 16-5. If the economy is at point 6,and the natural unemployment rate exists at points 1,4, and 5,it follows that

-Refer to Exhibit 16-5. If the economy is at point 6,and the natural unemployment rate exists at points 1,4, and 5,it follows that

(Multiple Choice)

4.7/5 (37)

Real business cycle theory emphasizes that an adverse supply shock will shift the LRAS curve leftward and cause a decline in Real GDP.

(True/False)

4.9/5 (31)

Suppose that the government implements expansionary fiscal policy that raises aggregate demand,but the policy is unanticipated. According to new classical theory,in the short run the price level would ____________ and Real GDP would ______________. In the long run,new classical theory would predict that the price level would ______________ compared to its original long-run equilibrium level and that Real GDP would ____________.

(Multiple Choice)

4.8/5 (34)

The difference between new classical theory and new Keynesian theory is that

(Multiple Choice)

4.9/5 (41)

In their 1960 article,Paul Samuelson and Robert Solow found

(Multiple Choice)

4.8/5 (38)

The real business cycle theory focuses on the impact that changes in long-run aggregate supply will have on the business cycle.

(True/False)

4.9/5 (34)

Under new Keynesian theory,a correctly anticipated decrease in aggregate demand will lead to __________ in Real GDP and __________ in the price level.

(Multiple Choice)

4.9/5 (33)

The Friedman natural rate theory holds that there is an inverse relationship between inflation and unemployment in the long run,but not in the short run.

(True/False)

4.8/5 (37)

The Phillips curve that Samuelson and Solow fitted to their data was

(Multiple Choice)

4.9/5 (36)

According to a new Keynesian theorist,a correctly anticipated increase in aggregate demand will

(Multiple Choice)

4.9/5 (32)

According to the original Phillips curve,the cost of reducing the unemployment rate in the short run is a

(Multiple Choice)

4.8/5 (34)

One of the arguments supporting new classical theory is the policy ineffectiveness proposition (PIP).

(True/False)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)