Exam 16: Expectations Theory and the Economy

Exam 1: What Economics Is About168 Questions

Exam 2: Production Possibilities Frontier Framework152 Questions

Exam 3: Supply and Demand: Theory227 Questions

Exam 4: Prices: Free, Controlled, and Relative107 Questions

Exam 5: Supply, Demand, and Price: Applications83 Questions

Exam 6: Macroeconomic Measurements: Prices and Unemployment129 Questions

Exam 7: Macroeconomic Measurements: GDP and Real GDP138 Questions

Exam 8: Aggregate Demand and Aggregate Supply208 Questions

Exam 9: Classical Macroeconomics and the Self Regulating Economy167 Questions

Exam 10: Keynesian Macroeconomics and Economic Instability: A Critique of the Self-Regulating Economy198 Questions

Exam 11: Fiscal Policy and the Federal Budget164 Questions

Exam 12: Money, Banking,and the Financial System124 Questions

Exam 13: The Federal Reserve System184 Questions

Exam 14: Money and the Economy125 Questions

Exam 15: Monetary Policy176 Questions

Exam 16: Expectations Theory and the Economy146 Questions

Exam 17: Economic Growth: Resources, Technology, Ideas, and Institutions82 Questions

Exam 18: The Financial Crisis of 2007-200970 Questions

Exam 19: Debates in Macroeconomics Over the Role and Effects of Government69 Questions

Exam 20: Elasticity198 Questions

Exam 21: Consumer Choice: Maximizing Utility and Behavioral Economics176 Questions

Exam 22: Production and Costs247 Questions

Exam 23: Perfect Competition191 Questions

Exam 24: Monopoly191 Questions

Exam 25: Monopolistic Competition, Oligopoly, and Game Theory167 Questions

Exam 26: Government and Product Markets: Antitrust and Regulation165 Questions

Exam 27: Factor Markets: With Emphasis on the Labor Market181 Questions

Exam 28: Wages,Unions,and Labor134 Questions

Exam 29: The Distribution of Income and Poverty93 Questions

Exam 30: Interest, Rent, and Profit199 Questions

Exam 31: Market Failure: Externalities, Public Goods, and Asymmetric Information185 Questions

Exam 32: Public Choice and Special-Interest-Group Politics131 Questions

Exam 33: Building Theories to Explain Everyday Life: From Observations to Questions to Theories to Predictions60 Questions

Exam 34: International Trade152 Questions

Exam 35: International Finance119 Questions

Exam 36: Globalization and International Impacts on the Economy136 Questions

Exam 37: The Economic Case For and Against Government: Five Topics Considered82 Questions

Exam 38: Stocks, Bonds, Futures, and Options108 Questions

Exam 39: Agriculture: Problems, Policies, and Unintended Effects149 Questions

Select questions type

Expectations theory tells us that what people think can impact the economy.

(True/False)

4.9/5  (31)

(31)

The economist who won the Nobel Prize in Economics in 1995,and whose name is closely connected with rational expectations theory,is

(Multiple Choice)

4.7/5 (39)

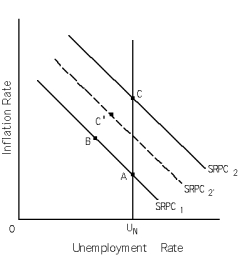

An unanticipated decrease in aggregate demand will cause an upward shift in the short-run Phillips curve.

(True/False)

4.8/5 (38)

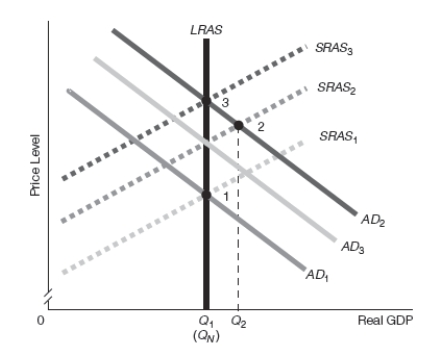

Exhibit 16-9

-Refer to Exhibit 16-9. Assume that the starting point is point 1. Suppose that the government implements expansionary fiscal policy that raises aggregate demand. Which of the following best goes with the diagram shown?

-Refer to Exhibit 16-9. Assume that the starting point is point 1. Suppose that the government implements expansionary fiscal policy that raises aggregate demand. Which of the following best goes with the diagram shown?

(Multiple Choice)

4.8/5 (28)

Explain the difference between how adaptive expectations are formed and how rational expectations are formed.How does this difference affect the speed at which economic variables are expected to change?

(Essay)

4.8/5 (38)

Exhibit 16-2

-Refer to Exhibit 16-2.Suppose the economy starts at point B.Fed monetary policy shifts the AD curve to AD1.If policy is correctly anticipated and people hold rational expectations,according to new classical theory the economy in the short run will

-Refer to Exhibit 16-2.Suppose the economy starts at point B.Fed monetary policy shifts the AD curve to AD1.If policy is correctly anticipated and people hold rational expectations,according to new classical theory the economy in the short run will

(Multiple Choice)

4.8/5 (42)

Describe the sequence of events that real business cycle theorists would use to explain how an adverse supply shock would impact the economy.Use your answer to explain why it is easy to confuse cause and effect between changes originating on the supply side and those that begin on the demand side.

(Essay)

5.0/5 (34)

New classical economists believe that if policy is correctly anticipated and if rational expectations hold,when the Fed increases the money supply the result will be a(n)______________ in the price level and ____________________________.

(Multiple Choice)

4.8/5 (42)

Suppose that the government implements expansionary fiscal policy that raises aggregate demand,but individuals incorrectly anticipate the policy measure (bias upward). According to new classical theory,in the short run the price level would ____________ and Real GDP would ______________. In the long run,new classical theory would predict that the price level would ______________ compared to its original long-run equilibrium level and that Real GDP would _____________.

(Multiple Choice)

4.8/5 (40)

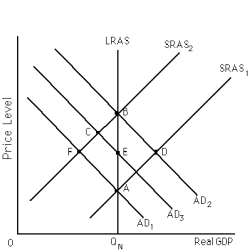

Exhibit 16-3

-Refer to Exhibit 16-3.The economy is at point A.According to the Friedman natural rate theory,in the long run after a rise in the money supply,the economy will be at point

-Refer to Exhibit 16-3.The economy is at point A.According to the Friedman natural rate theory,in the long run after a rise in the money supply,the economy will be at point

(Multiple Choice)

4.9/5 (49)

New Keynesian theory differs from new classical theory in that New Keynesian theory assumes that wages and prices are not completely flexible in the short-run,while fully flexible wages and prices are an assumption of new classical theory.

(True/False)

4.7/5 (36)

Milton Friedman argued that the economy is not in long-run equilibrium if the expected inflation rate __________ the actual inflation rate.

(Multiple Choice)

4.8/5 (41)

Rational expectations are based on the past alone,while adaptive expectations are based on the past,the present,and the future.

(True/False)

4.8/5 (33)

Which of the following assumptions is held by both the classical view and the new classical view?

(Multiple Choice)

4.9/5 (40)

New classical economists believe that monetary and fiscal policies are never effective.

(True/False)

4.9/5 (40)

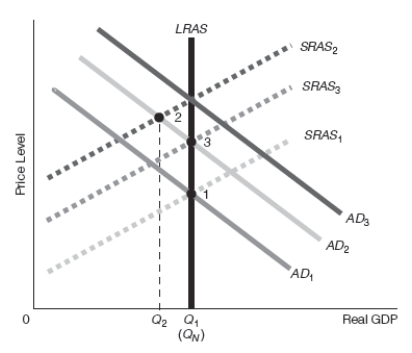

Exhibit 16-8

-Refer to Exhibit 16-8. Assume that the starting point is point 1. Suppose that the Fed implements expansionary monetary policy that raises aggregate demand. Which of the following best goes with the diagram shown?

-Refer to Exhibit 16-8. Assume that the starting point is point 1. Suppose that the Fed implements expansionary monetary policy that raises aggregate demand. Which of the following best goes with the diagram shown?

(Multiple Choice)

4.9/5 (45)

Although the possibility exists for an economy to experience stagflation,it has never actually happened in the United States.

(True/False)

5.0/5 (35)

According to new classical economists,if a decrease in aggregate demand is correctly anticipated,the short-run aggregate supply curve will shift __________ at the same time the AD curve shifts _________ so that there will be no change in Real GDP .

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)