Exam 24: From the Short Run to the Long Run: the Adjustment of Factor Prices

Exam 1: Economic Issues and Concepts130 Questions

Exam 2: Economic Theories, Data, and Graphs140 Questions

Exam 3: Demand, Supply, and Price161 Questions

Exam 4: Elasticity160 Questions

Exam 5: Price Controls and Market Efficiency125 Questions

Exam 6: Consumer Behaviour140 Questions

Exam 7: Producers in the Short Run144 Questions

Exam 8: Producers in the Long Run141 Questions

Exam 9: Competitive Markets153 Questions

Exam 10: Monopoly, Cartels, and Price Discrimination126 Questions

Exam 11: Imperfect Competition and Strategic Behaviour126 Questions

Exam 12: Economic Efficiency and Public Policy123 Questions

Exam 13: How Factor Markets Work124 Questions

Exam 14: Labour Markets and Income Inequality117 Questions

Exam 16: Market Failures and Government Intervention123 Questions

Exam 17: The Economics of Environmental Protection133 Questions

Exam 18: Taxation and Public Expenditure121 Questions

Exam 19: What Macroeconomics Is All About116 Questions

Exam 20: The Measurement of National Income117 Questions

Exam 21: The Simplest Short-Run Macro Model156 Questions

Exam 22: Adding Government and Trade to the Simple Macro Model132 Questions

Exam 23: Output and Prices in the Short Run142 Questions

Exam 24: From the Short Run to the Long Run: the Adjustment of Factor Prices148 Questions

Exam 25: Long-Run Economic Growth132 Questions

Exam 26: Money and Banking119 Questions

Exam 27: Money, Interest Rates, and Economic Activity135 Questions

Exam 28: Monetary Policy in Canada122 Questions

Exam 29: Inflation and Disinflation123 Questions

Exam 30: Unemployment Fluctuations and the Nairu120 Questions

Exam 31: Government Debt and Deficits129 Questions

Exam 32: The Gains From International Trade127 Questions

Exam 33: Trade Policy126 Questions

Exam 34: Exchange Rates and the Balance of Payments161 Questions

Select questions type

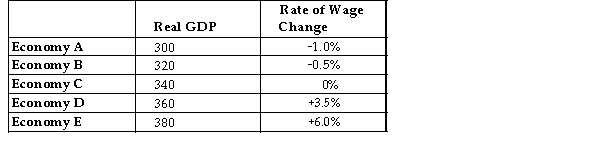

The table below shows data for five economies of similar size. Real GDP is measured in billions of dollars. Assume that potential output for each economy is $340 billion.  TABLE 24-1

-Refer to Table 24-1. In which economy is there the most unused capacity?

TABLE 24-1

-Refer to Table 24-1. In which economy is there the most unused capacity?

(Multiple Choice)

4.8/5  (39)

(39)

Consider the AD/AS macro model. An important asymmetry in the behaviour of aggregate supply is the

(Multiple Choice)

5.0/5 (37)

The curve that is sometimes called the ʺlong-run aggregate supply curveʺ vertical Y*) relates the aggregate price level to real GDP

(Multiple Choice)

4.8/5 (30)

The table below shows data for five economies of similar size. Real GDP is measured in billions of dollars. Assume that potential output for each economy is $340 billion. TABLE 24-1

-Suppose that the economy is initially in a long-run macroeconomic equilibrium. A shock then hits the economy and we observe that the unemployment rate decreases and the price level decreases. We can conclude that

Has increased and there is now an) gap.

(Multiple Choice)

4.8/5 (38)

The ʺparadox of thriftʺ refers to the understandable tendency of people who are worried about their economic situation to their saving, but in aggregate this behaviour causes a recession.

(Multiple Choice)

4.8/5 (39)

Consider the simplest macro model with demand-determined output. Other things being equal, the the value of the simple multiplier, the stable is real GDP in response to shocks to autonomous spending.

(Multiple Choice)

4.9/5 (42)

Consider an AD/AS model in long-run equilibrium. An output gap, caused by a leftward shift of the AD curve, will be eliminated if

(Multiple Choice)

4.7/5 (46)

The table below shows data for five economies of similar size. Real GDP is measured in billions of dollars. Assume that potential output for each economy is $340 billion. TABLE 24-1

-Refer to Table 24-1. How is the adjustment asymmetry demonstrated when comparing Economy A to Economy E?

(Multiple Choice)

4.8/5 (42)

Consider the AD/AS macro model. The wage-adjustment process is asymmetrical because

(Multiple Choice)

4.9/5 (37)

Suppose the government had made a decision to change fiscal policy, but it then took nine months to implement a tax reduction. This is an example of

(Multiple Choice)

4.7/5 (37)

A common assumption among macroeconomists is that when real GDP is less than potential output, factor prices adjust and the

(Multiple Choice)

4.7/5 (35)

Which of the following provides the best explanation for why GDP may increase over long periods of time?

(Multiple Choice)

4.8/5 (40)

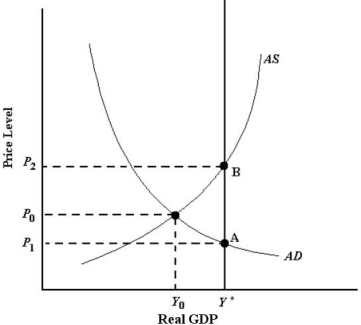

FIGURE 24-1

-Refer to Figure 24-1. Suppose the economy is currently in a short-run equilibrium with output of Y0. An appropriate fiscal policy response, to attain potential output Y*), is

FIGURE 24-1

-Refer to Figure 24-1. Suppose the economy is currently in a short-run equilibrium with output of Y0. An appropriate fiscal policy response, to attain potential output Y*), is

(Multiple Choice)

4.9/5 (32)

The paradox of thrift does not exist in the long run because

(Multiple Choice)

4.9/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)