Exam 20: Accounting Changes and Error Corrections

Exam 1: Financial Reporting86 Questions

Exam 2: A Review of the Accounting Cycle94 Questions

Exam 3: The Balance Sheet and Notes to the Financial Statements72 Questions

Exam 4: The Income Statement82 Questions

Exam 5: Statement of Cash Flows and Articulation79 Questions

Exam 6: Earnings Management46 Questions

Exam 7: The Revenuereceivablescash Cycle81 Questions

Exam 8: Revenue Recognition74 Questions

Exam 9: Inventory and Cost of Goods Sold121 Questions

Exam 10: Investments in Noncurrent Operating Assets-Acquisition88 Questions

Exam 11: Investments in Noncurrent Operating Assets-Utilization and Retirement84 Questions

Exam 12: Debt Financing103 Questions

Exam 13: Equity Financing88 Questions

Exam 14: Investments in Debt and Equity Securities81 Questions

Exam 15: Leases80 Questions

Exam 16: Income Taxes77 Questions

Exam 17: Employee Compensation-Payroll, Pensions, Other Comp Issues78 Questions

Exam 18: Earnings Per Share78 Questions

Exam 19: Derivatives, Contingencies, Business Segments, and Interim Reports79 Questions

Exam 20: Accounting Changes and Error Corrections74 Questions

Exam 21: Statement of Cash Flows Revisited61 Questions

Exam 22: Accounting in a Global Market60 Questions

Exam 23: Analysis of Financial Statements57 Questions

Select questions type

Ending inventory for 2009 is overstated by $4,000 due to a faulty count and costing. The tax rate is 30%. Assume the same accounting methods for both financial reporting and taxes. The error is discovered late in 2011. The 2011 annual report shows the financial statements for 2009, 2010, 2011 on a comparative basis.

Which of the following is correct regarding the reporting of this error in the 2011 annual report?

(Multiple Choice)

4.8/5  (37)

(37)

Adams Company decides at the beginning of 2011 to adopt the FIFO method of inventory valuation. The company had been using the LIFO method for financial and tax reporting since it inception on January 1, 2009. The profit-sharing agreement was in place for all years prior to the year of change, 2011. Payments under this agreement are not an inventoriable cost.

Which of the following statements regarding the accounting for the profit-sharing agreement in connection with the change from LIFO to FIFO is correct?

(Multiple Choice)

4.8/5 (46)

Which of the following should be reported as a change in accounting estimate?

(Multiple Choice)

4.9/5 (43)

On January 1, 2011, Nicole Corporation changed its method of accounting for bad debts from the direct write-off method to the allowance method. The company's controller determined that an allowance of $22,000 should be established on that date.

(Essay)

4.8/5 (37)

Effective January 2, 2011, Kincaid Co. adopted the accounting principle of expensing advertising and promotion costs as they are incurred. Previously, advertising and promotion costs applicable to future periods were recorded in prepaid expenses. Kincaid can justify the change, which was made for both financial statement and income tax reporting purposes. Kincaid's prepaid advertising and promotion costs totaled $250,000 at December 31, 2010. Assume that the income tax rate is 40 percent for 2010 and 2011. The adjustment for the effect of the change in accounting principle should result in a net charge against income in the income statement for 2011 of

(Multiple Choice)

4.9/5 (45)

Barker, Inc. receives subscription payments for annual (one year) subscriptions to its magazine. Payments are recorded as revenue when received. Amounts received but unearned at the end of each of the last three years are shown below:

Barker failed to record the unearned revenues in each of the three years. As a result of the omission, 2011 income was

Barker failed to record the unearned revenues in each of the three years. As a result of the omission, 2011 income was

(Multiple Choice)

4.9/5 (42)

Managers often are accused of making accounting changes in order to avoid regulation, to achieve compliance with debt covenants, to increase compensation through earnings-based bonus plans, or to smooth earnings. Managers may indeed believe that by increasing earnings, and thus increasing earnings per share, stock prices will increase.

Explain the relationship between attempts by managers to manipulate earnings through accounting changes and the efficient market hypothesis.

(Essay)

4.9/5 (38)

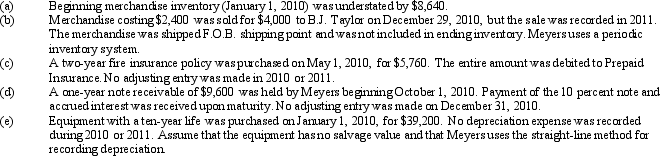

In reviewing the books of Meyers Retailers Inc., the auditor discovered certain errors that had occurred during 2010 and 2011. No errors were corrected during 2010. The errors are summarized below:

Prepare journal entries to correct each of these independent situations. Assume that the nominal accounts for 2011 have not yet been closed into the income summary account.

Prepare journal entries to correct each of these independent situations. Assume that the nominal accounts for 2011 have not yet been closed into the income summary account.

(Essay)

4.8/5 (42)

Which of the following is not correct regarding the provisions of IAS No. 8 on accounting changes and error corrections?

(Multiple Choice)

5.0/5 (45)

Perfect Technologies has estimated bad debts using the percentage-of-sales method since their business began operations in 2008. Information relating to bad debts and sales is as follows:

At the beginning of 2011, Perfect proposes changing their estimation of bad debt expense from 3 percent of sales to 2 percent. Sales for the year totaled $163,000 and actual bad debts amounted to $3,720.

At the beginning of 2011, Perfect proposes changing their estimation of bad debt expense from 3 percent of sales to 2 percent. Sales for the year totaled $163,000 and actual bad debts amounted to $3,720.

(Essay)

4.9/5 (32)

Which of the following would cause income of the current period to be understated?

(Multiple Choice)

4.9/5 (36)

The cumulative effect on prior years' earnings of a change in accounting principle should be reported separately as an adjustment to retained earnings for the earliest period presented for all of the following changes except

(Multiple Choice)

4.7/5 (37)

Koppell Co. made the following errors in counting its year-end physical inventories:

As a result of the above undetected errors, 2011 income was

As a result of the above undetected errors, 2011 income was

(Multiple Choice)

4.7/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)