Exam 20: Accounting Changes and Error Corrections

Exam 1: Financial Reporting86 Questions

Exam 2: A Review of the Accounting Cycle94 Questions

Exam 3: The Balance Sheet and Notes to the Financial Statements72 Questions

Exam 4: The Income Statement82 Questions

Exam 5: Statement of Cash Flows and Articulation79 Questions

Exam 6: Earnings Management46 Questions

Exam 7: The Revenuereceivablescash Cycle81 Questions

Exam 8: Revenue Recognition74 Questions

Exam 9: Inventory and Cost of Goods Sold121 Questions

Exam 10: Investments in Noncurrent Operating Assets-Acquisition88 Questions

Exam 11: Investments in Noncurrent Operating Assets-Utilization and Retirement84 Questions

Exam 12: Debt Financing103 Questions

Exam 13: Equity Financing88 Questions

Exam 14: Investments in Debt and Equity Securities81 Questions

Exam 15: Leases80 Questions

Exam 16: Income Taxes77 Questions

Exam 17: Employee Compensation-Payroll, Pensions, Other Comp Issues78 Questions

Exam 18: Earnings Per Share78 Questions

Exam 19: Derivatives, Contingencies, Business Segments, and Interim Reports79 Questions

Exam 20: Accounting Changes and Error Corrections74 Questions

Exam 21: Statement of Cash Flows Revisited61 Questions

Exam 22: Accounting in a Global Market60 Questions

Exam 23: Analysis of Financial Statements57 Questions

Select questions type

An accounting change that requires the retrospective approach is a change in

(Multiple Choice)

4.8/5  (41)

(41)

Barker, Inc. receives subscription payments for annual (one year) subscriptions to its magazine. Payments are recorded as revenue when received. Amounts received but unearned at the end of each of the last three years are shown below.

Barker failed to record the unearned revenues in each of the three years. The entry needed to correct the above errors is

Barker failed to record the unearned revenues in each of the three years. The entry needed to correct the above errors is

(Multiple Choice)

4.8/5 (47)

Badger Corporation purchased a machine for $150,000 on January 1, 2010. Badger will depreciate the machine using the straight-line method using a five-year period with no residual value. As a result of an error in its purchasing records, Badger did not recognize any depreciation for the machine in its 2010 financial statements. Badger discovered the problem during the preparation of its 2011 financial statements. What amount should Badger record for depreciation expense on this machine for 2011?

(Multiple Choice)

4.8/5 (34)

For a company with a periodic inventory system, which of the following would cause income to be overstated in the period of occurrence?

(Multiple Choice)

4.7/5 (44)

On January 1, 2011, Wiley Corporation changed its inventory cost flow assumption from FIFO to LIFO. The change was made for financial statement and tax reporting. Wiley's inventory values at the end of each year since inception under both methods are summarized below.

Ignoring income taxes, what is the amount of adjustment required in the 2011 accounts, and where would it be reported in the financial statement?

Ignoring income taxes, what is the amount of adjustment required in the 2011 accounts, and where would it be reported in the financial statement?

(Essay)

4.8/5 (45)

On December 31, 2011, Buckeye Corporation appropriately changed its inventory valuation method to FIFO cost from LIFO cost for both financial statement and income tax purposes. The change will result in a $140,000 increase in the beginning inventory at January 1, 2011. Assume a 30 percent income tax rate. The cumulative effect of this accounting change Buckeye for the year ended December 31, 2011, is

(Multiple Choice)

4.8/5 (29)

On January 1, 2008, Grayson Company purchased for $240,000 a machine with a useful life of ten years and no salvage value. The machine was depreciated by the double-declining-balance method, and the carrying amount of the machine was $153,600 on December 31, 2009. Grayson changed to the straight-line method on January 1, 2010. Grayson can justify the change. What should be the depreciation expense on this machine for the year ended December 31, 2011?

(Multiple Choice)

4.8/5 (36)

Since its organization on January 1, 2009, Langley Inc. failed to properly recognize accruals and prepayments. Selected accounts revealed the following information:

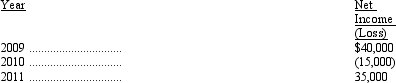

Net income reported by the company was:

Net income reported by the company was:

Compute the corrected net income for the years 2009, 2010, and 2011. (Ignore income taxes.)

Compute the corrected net income for the years 2009, 2010, and 2011. (Ignore income taxes.)

(Essay)

4.9/5 (38)

At the time Fisher Corporation became a subsidiary of Ashbury Corporation, Fisher switched depreciation of its plant assets from the straight-line method to the sum-of-the-years'-digits method used by Ashbury. With respect to Fisher, this change was a

(Multiple Choice)

4.7/5 (33)

On January 2, 2009, McKell Company acquired machinery at a cost of $640,000. This machinery was being depreciated by the double-declining-balance method over an estimated useful life of eight years, with no residual value. At the beginning of 2011, McKell decided to change to the straight-line method of depreciation. Ignoring income tax considerations, the cumulative effect of this accounting change is

(Multiple Choice)

4.9/5 (36)

Cameron Co. began operations on January 1, 2008, at which time it acquired depreciable assets of $100,000. The assets have an estimated useful life of ten years and no salvage value.

In 2011, Cameron Co. changed from the sum-of-the-years'-digits depreciation method to the straight-line depreciation method.

Required:

Determine the depreciation expense for 2011 and prepare the appropriate journal entry.

(Essay)

4.9/5 (40)

Johnson's Distributing purchased equipment on January 1, 2008. The equipment cost $124,000 with a salvage value of $12,000 and an estimated life of 8 years. Initially, Johnson depreciated the equipment using the sum-of-the-years'-digits method. On January 1, 2011, the company elected to change to the straight-line method of depreciation.

Required:

Determine the depreciation expense for 2011 and prepare the appropriate journal entry.

(Essay)

4.8/5 (34)

A change from an accelerated depreciation method to the straight-line depreciation method should be accounted for as a

(Multiple Choice)

4.9/5 (37)

Which of the following is correct regarding the provisions of IFRS No. 8 on accounting changes and error corrections?

(Multiple Choice)

4.9/5 (44)

Which of the following would not be accounted for as a change in accounting principle?

(Multiple Choice)

4.8/5 (33)

An example of an item that should be reported as a prior period adjustment is the

(Multiple Choice)

4.8/5 (39)

Which of the following is not an example of an accounting error, as distinguished from a change in accounting principle or change in accounting estimate?

(Multiple Choice)

4.9/5 (38)

The correction of an error in the financial statements of a prior period should be reflected, net of applicable income taxes, in the current

(Multiple Choice)

4.8/5 (50)

Which of the following is characteristic of a change in accounting principle?

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)