Exam 19: Derivatives, Contingencies, Business Segments, and Interim Reports

Exam 1: Financial Reporting86 Questions

Exam 2: A Review of the Accounting Cycle94 Questions

Exam 3: The Balance Sheet and Notes to the Financial Statements72 Questions

Exam 4: The Income Statement82 Questions

Exam 5: Statement of Cash Flows and Articulation79 Questions

Exam 6: Earnings Management46 Questions

Exam 7: The Revenuereceivablescash Cycle81 Questions

Exam 8: Revenue Recognition74 Questions

Exam 9: Inventory and Cost of Goods Sold121 Questions

Exam 10: Investments in Noncurrent Operating Assets-Acquisition88 Questions

Exam 11: Investments in Noncurrent Operating Assets-Utilization and Retirement84 Questions

Exam 12: Debt Financing103 Questions

Exam 13: Equity Financing88 Questions

Exam 14: Investments in Debt and Equity Securities81 Questions

Exam 15: Leases80 Questions

Exam 16: Income Taxes77 Questions

Exam 17: Employee Compensation-Payroll, Pensions, Other Comp Issues78 Questions

Exam 18: Earnings Per Share78 Questions

Exam 19: Derivatives, Contingencies, Business Segments, and Interim Reports79 Questions

Exam 20: Accounting Changes and Error Corrections74 Questions

Exam 21: Statement of Cash Flows Revisited61 Questions

Exam 22: Accounting in a Global Market60 Questions

Exam 23: Analysis of Financial Statements57 Questions

Select questions type

Which of the following is not true regarding standards for interim reporting?

(Multiple Choice)

4.8/5  (38)

(38)

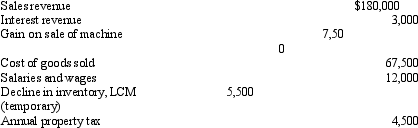

Marshall Company reported the following data with regard to its first quarter of operations:

The expected annual income tax rate is 40 percent. Marshall should report net income on the first quarter interim financial statements of

The expected annual income tax rate is 40 percent. Marshall should report net income on the first quarter interim financial statements of

(Multiple Choice)

4.9/5 (32)

Information obtained prior to the issuance of the current period's financial statements of a company indicates that it is probable that, at the date of the financial statements, a liability will be incurred for obligations related to product warranties on products sold during the current period. During the past three years, product warranty costs have been approximately 1 1/2 percent of annual sales revenue.

An estimated loss contingency should be

(Multiple Choice)

4.9/5 (44)

A contingent loss should be disclosed in a note to the financial statements but should not be recorded as a liability if the

(Multiple Choice)

4.8/5 (46)

In exchange for the rights inherent in an option contract, the owner of the option will typically pay a price

(Multiple Choice)

4.9/5 (39)

Uncertainty that the party on the other side of an agreement will abide by the terms of the agreement is referred to as

(Multiple Choice)

4.8/5 (34)

Which of the following measures is not used to determine whether a subunit of a business is a reportable segment?

(Multiple Choice)

4.8/5 (40)

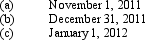

On November 5, 2011, a Timp Rental truck was in an accident with an auto driven by Fred Meyer. Timp Rental received notice on January 12, 2012, of a lawsuit for $700,000 damages for personal injuries suffered by Meyer. Timp Rental's counsel believes it is probable that Meyer will be awarded an estimated amount in the range between $200,000 and $450,000, and that $300,000 is a better estimate of potential liability than any other amount. Timp's accounting year ends on December 31, and the 2011 financial statements were issued on March 2, 2012. What amount of loss should Timp accrue at December 31, 2011?

(Multiple Choice)

4.8/5 (39)

On November 1, 2011, Cahoon Company sold some limited edition art prints to Sitake Company for ¥47,850,000 to be paid on January 1, 2012. The current exchange rate on November 1, 2011, was ¥110=$1, so the total payment at the current exchange rate would be equal to $435,000. Cahoon entered into a forward contract with a large bank to guarantee the number of dollars to be received. According to the terms of the contract, if ¥47,850,000 is worth less than $435,000, the bank will pay Cahoon the difference in cash. Likewise, if ¥47,850,000 is worth more than $435,000, Cahoon must pay the bank the difference in cash. Assuming the exchange rate on December 31, 2011 is ¥115=$1, what amount will Cahoon disclose as the fair value of the forward contract on December 31, 2011 (answers rounded to the nearest dollar)?

(Multiple Choice)

4.8/5 (37)

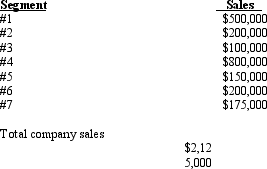

The following segments have been identified for an enterprise, along with each segments sales. No segment qualifies on any other criterion for determining reportable segments except possibly for sales. Sales for each segment, and the total for the enterprise follow:

What is the minimum number of reportable segments for this firm?

What is the minimum number of reportable segments for this firm?

(Multiple Choice)

4.8/5 (39)

Which of the following is most likely to require only a note disclosure as a contingency?

(Multiple Choice)

4.9/5 (37)

When gains or losses on derivatives designated as fair value hedges exceed the gains or losses on the item being hedged, the excess

(Multiple Choice)

4.9/5 (39)

Stiggins Fitness Enterprises uses soybeans to make one of their nutritional supplement products. Stiggins anticipates a need of 500,000 pounds of soybeans in January of 2012. On November 1, 2011, Stiggins purchased a call option for 500,000 pounds of soybeans on January 1, 2012, at a price of $0.40 per pound, which is the market price on November 1. Stiggins paid $1,200 for the call option and designated this option as a hedge against price fluctuations for their January purchase of soybeans. On December 31, 2011, and January 1, 2012, the prevailing market price for soybeans is $0.45 per pound. On January 1, 2012, Stiggins purchased 500,000 pounds of soybeans.

Make the necessary entries on Stiggins's books at

(Essay)

5.0/5 (35)

Which of the following is themost likely candidate for a contingent liability that must be accrued?

(Multiple Choice)

4.8/5 (41)

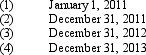

On January 1, 2011, Eden Ventures, Inc., received a three-year, $1 million loan with interest payments due at the end of each year and the principal to be repaid on December 31, 2013. The interest rate for the first year is the prevailing market rate of 9 percent, and the rate each succeeding year will be equal to the prevailing market rate on January 1 of that year. Eden also entered into an interest rate swap agreement related to this loan. Under the terms of the swap agreement, in the years 2012 and 2013, Eden will receive a swap payment based on the principal amount of $1 million. If the January 1 interest rate is greater than 9 percent, Eden will receive a swap payment for the difference; and if the January 1 interest rate is less than 9 percent, Eden will make a swap payment for the difference. The swap payments are made on December 31 of each year. On January 1, 2012, the interest rate is 8 percent, and on January 1, 2013, the interest rate is 12 percent.

Make all the journal entries necessary on Eden's books at the dates shown below. For purposes of estimating future swap payments, assume that the current interest rate is the best forecast of the future interest rate (round all entries to the nearest dollar).

(Essay)

4.9/5 (30)

On January 1, 2011, Cougar Company received a two-year $500,000 loan. The loan calls for payments to made at the end of each year based on the prevailing market rate at January 1 of each year. The interest rate at January 1, 2011, was 10 percent. Aggie company also has a two-year $500,000 loan, but Aggie's loan carries a fixed interest rate of 10 percent.

Cougar Company does not want to bear the risk that interest rates may increase in year two of the loan. Aggie Company believes that rates may decrease and they would prefer to have variable debt. So the two companies enter into an interest rate swap agreement whereby Aggie agrees to make Cougar's interest payment in 2012 and Cougar likewise agrees to make Aggie's interest payment in 2012. The two companies agree to make settlement payments, for the difference only, on December 31, 2012. If the interest rate on January 1, 2012, is 12 percent, what will be Cougar's settlement payment to/from Aggie?

(Multiple Choice)

4.8/5 (34)

When a company with reportable segments issues interim condensed financial statements, current GAAP requires that the interim reports provide all of the following for each reportable segment except

(Multiple Choice)

4.9/5 (40)

A contingency must be accrued in the accounts and reported in the financial statements when

(Multiple Choice)

4.9/5 (36)

An obligation that is contingent on the occurrence of a future event should be reported in the balance sheet as a liability if the

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)