Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models459 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System492 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply476 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes420 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods262 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply293 Questions

Exam 7: The Economics of Health Care337 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance512 Questions

Exam 9: Comparative Advantage and the Gains From International Trade377 Questions

Exam 10: Consumer Choice and Behavioral Economics304 Questions

Exam 11: Technology, Production, and Costs326 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting272 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets256 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy258 Questions

Exam 17: The Markets for Labor and Other Factors of Production279 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: Gdp: Measuring Total Production and Income260 Questions

Exam 20: Unemployment and Inflation290 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles251 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies261 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run305 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis286 Questions

Exam 25: Money, Banks, and the Federal Reserve System278 Questions

Exam 26: Monetary Policy280 Questions

Exam 27: Fiscal Policy313 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy277 Questions

Exam 30: The International Financial System258 Questions

Select questions type

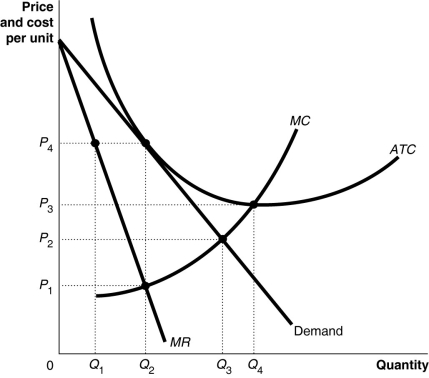

Figure 13-11  -Refer to Figure 13-11. What is the monopolistic competitor's profit maximizing output?

-Refer to Figure 13-11. What is the monopolistic competitor's profit maximizing output?

(Multiple Choice)

4.7/5  (38)

(38)

What is the most important difference between perfectly competitive markets and monopolistically competitive markets?

(Essay)

4.8/5 (38)

For a downward-sloping demand curve, the marginal revenue decreases as the quantity sold increases.

(True/False)

4.8/5 (41)

A monopolistically competitive market is described as one in which there are

(Multiple Choice)

4.9/5 (39)

Explain the similarities and differences between the long-run equilibrium for a perfectly competitive firm and a monopolistically competitive firm. Illustrate your answer with a graph demonstrating the long-run equilibrium for the two types of firms.

(Essay)

4.8/5 (47)

Assume price exceeds average variable cost over the relevant range of demand. If a monopolistically competitive firm is producing at an output where marginal revenue is $23 and marginal cost is $19, then to maximize profits the firm should

(Multiple Choice)

4.9/5 (34)

A firm that is first to the market with a new product frequently discovers that there are design flaws or problems with the product that were not anticipated. How do these problems affect the innovating firm?

(Multiple Choice)

4.8/5 (39)

The key characteristics of a monopolistically competitive market structure include

(Multiple Choice)

4.7/5 (36)

Which of the following is not a characteristic of long-run equilibrium in a monopolistically competitive market?

(Multiple Choice)

5.0/5 (39)

Recent research has shown that the first firm to enter a market often does not have a long-term advantage over later entrants into the market. An example that has been used to illustrate this is

(Multiple Choice)

4.8/5 (39)

When a firm faces a downward-sloping demand curve, marginal revenue

(Multiple Choice)

4.8/5 (40)

A monopolistically competitive firm maximizes profit in the short run by producing where

(Multiple Choice)

4.9/5 (38)

If a monopolistically competitive firm has excess capacity

(Multiple Choice)

4.8/5 (36)

Suppose James and Katherine are successful in establishing a profitable market for their "ghost restaurants" in what is a monopolistically competitive industry. In the long run, James and Katherine will most likely find it ________ to remain profitable as they face ________ competition in the "ghost restaurant" market.

(Multiple Choice)

4.7/5 (42)

What is the profit-maximizing rule for a monopolistically competitive firm?

(Multiple Choice)

4.9/5 (33)

A monopolistically competitive firm faces a downward-sloping demand curve because

(Multiple Choice)

4.9/5 (38)

In the long run, what happens to the demand curve facing a monopolistically competitive firm that is earning short-run profits?

(Multiple Choice)

4.8/5 (35)

The ability to engage in product differentiation is one of the factors a manager or owner of a firm can control in order to create value for consumers.

(True/False)

4.7/5 (39)

One way by which firms differentiate their products is to try to anticipate changes in consumer tastes and adapt their products to fit those changed tastes.

(True/False)

4.8/5 (37)

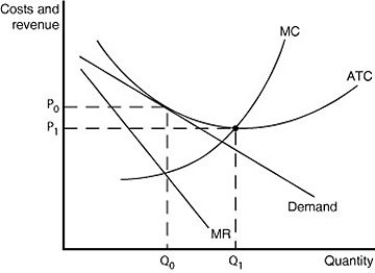

Figure 13-14  Figure 13-14 illustrates a monopolistically competitive firm.

-Refer to Figure 13-14. It is possible to lower the average cost of production by expanding output beyond Q0 to Q1. Why wouldn't a firm expand its output to Q1?

Figure 13-14 illustrates a monopolistically competitive firm.

-Refer to Figure 13-14. It is possible to lower the average cost of production by expanding output beyond Q0 to Q1. Why wouldn't a firm expand its output to Q1?

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)