Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models459 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System492 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply476 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes420 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods262 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply293 Questions

Exam 7: The Economics of Health Care337 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance512 Questions

Exam 9: Comparative Advantage and the Gains From International Trade377 Questions

Exam 10: Consumer Choice and Behavioral Economics304 Questions

Exam 11: Technology, Production, and Costs326 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting272 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets256 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy258 Questions

Exam 17: The Markets for Labor and Other Factors of Production279 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: Gdp: Measuring Total Production and Income260 Questions

Exam 20: Unemployment and Inflation290 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles251 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies261 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run305 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis286 Questions

Exam 25: Money, Banks, and the Federal Reserve System278 Questions

Exam 26: Monetary Policy280 Questions

Exam 27: Fiscal Policy313 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy277 Questions

Exam 30: The International Financial System258 Questions

Select questions type

If the demand curve for a firm is downward-sloping, its marginal revenue curve

(Multiple Choice)

4.7/5  (30)

(30)

If a monopolistically competitive firm is producing 50 units of output where marginal cost equals marginal revenue, total cost is $1,674 and total revenue is $2,000, its average profit is

(Multiple Choice)

4.8/5 (33)

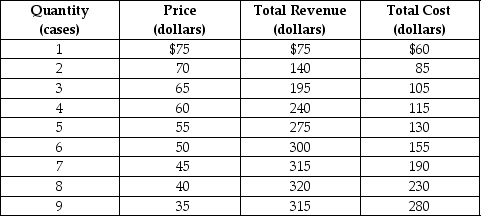

Table 13-2

Eco Energy is a monopolistically competitive producer of a sports beverage called Power On. Table 13-2 shows the firm's demand and cost schedules.

-Refer to Table 13-2. What is the output (Q) that maximizes profit and what is the price (P) charged?

Eco Energy is a monopolistically competitive producer of a sports beverage called Power On. Table 13-2 shows the firm's demand and cost schedules.

-Refer to Table 13-2. What is the output (Q) that maximizes profit and what is the price (P) charged?

(Multiple Choice)

4.7/5 (37)

Which of the following is not a characteristic of monopolistic competition?

(Multiple Choice)

4.7/5 (37)

Why are demand and marginal revenue represented by the same curve for a firm in a perfectly competitive market, but by separate curves for a firm in a monopolistically competitive market?

(Essay)

4.9/5 (45)

A monopolistically competitive firm can increase its profits beyond the long-run equilibrium break-even level by deliberately lowering its price to force some of its competitors out of the market.

(True/False)

4.8/5 (43)

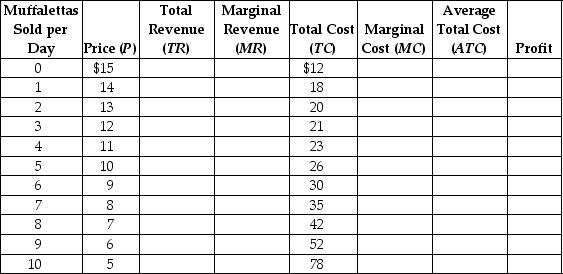

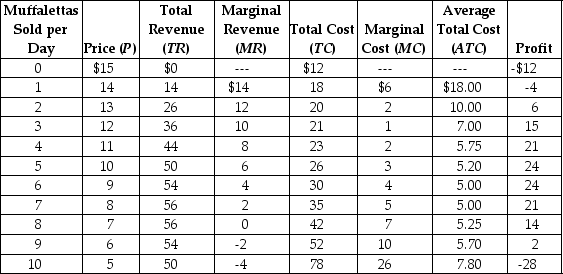

Central Grocery in New Orleans is famous for its muffaletta, a large round sandwich filled with deli meats and topped with a tangy olive salad. Suppose the following table represents cost and revenue data for Central Grocery. Fill in the columns for TR, MR, MC, ATC, and profit. If Central Grocery wants to maximize profits, what price should it charge for a muffaletta, what quantity should it sell, and what will be the amount of its total profit?

(Essay)

4.9/5 (32)

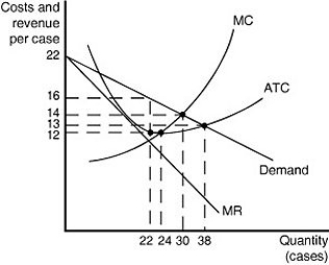

Figure 13-8  Figure 13-8 shows cost and demand curves for a monopolistically competitive producer of iced tea.

-Refer to Figure 13-8. Based on the diagram, one can conclude that

Figure 13-8 shows cost and demand curves for a monopolistically competitive producer of iced tea.

-Refer to Figure 13-8. Based on the diagram, one can conclude that

(Multiple Choice)

4.8/5 (35)

Which of the following describes a difference between the marginal revenue and demand curves of a perfectly competitive firm and a monopolistically competitive firm?

(Multiple Choice)

4.8/5 (35)

When a monopolistically competitive firm cuts its price to increase its sales, it experiences a loss in revenue due to the income effect and a gain in revenue due to the substitution effect.

(True/False)

4.7/5 (39)

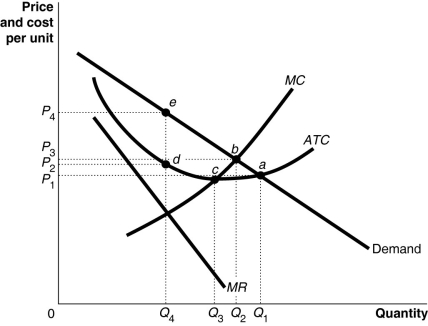

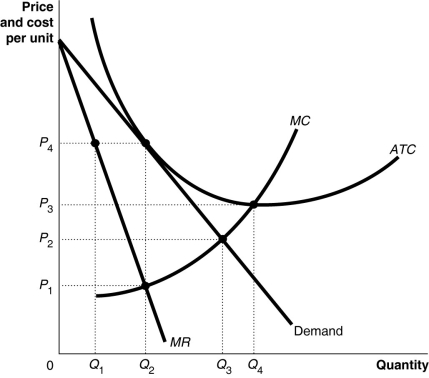

Figure 13-13  -Refer to Figure 13-13. What is the output price?

-Refer to Figure 13-13. What is the output price?

(Multiple Choice)

5.0/5 (38)

Figure 13-11  -Why do most firms in monopolistic competition typically make zero profit in the long run?

-Why do most firms in monopolistic competition typically make zero profit in the long run?

(Multiple Choice)

4.9/5 (38)

Which of the following is a disadvantage of trademarking a firm's product?

(Multiple Choice)

4.9/5 (39)

What effect does the entry of new firms in a monopolistically competitive market have on the economic profits of existing firms in the market? How might existing firms attempt to counteract this effect?

(Essay)

4.9/5 (26)

Compared to a perfectly competitive firm, the demand curve facing a monopolistically competitive firm is

(Multiple Choice)

4.9/5 (36)

Central Grocery in New Orleans is famous for its muffaletta, a large round sandwich filled with deli meats and topped with a tangy olive salad. Suppose the following table represents cost and revenue data for Central Grocery.

Illustrate this data by graphing the demand, MR, MC, and ATC curves. Identify the profit-maximizing price and quantity, and show the area representing the total profit received by Central Grocery.

Illustrate this data by graphing the demand, MR, MC, and ATC curves. Identify the profit-maximizing price and quantity, and show the area representing the total profit received by Central Grocery.

(Essay)

4.9/5 (39)

Suppose Jason owns a small pastry shop. Jason wants to maximize his profit, and thinking back to the microeconomics class he took in college, he decides he needs to produce a quantity of pastries which will minimize his average total cost. Will Jason's strategy necessarily maximize profits for his pastry shop?

(Multiple Choice)

4.8/5 (37)

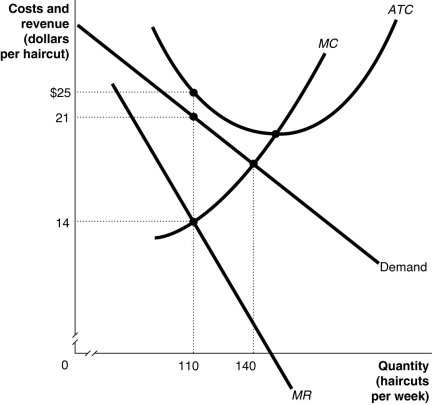

Figure 13-16  -Refer to Figure 13-16. Figure 13-16 depicts a monopolistically competitive barber shop. Use the diagram to answer the following questions.

a. Suppose the average variable cost of production is $15 when output equals 110 haircuts and $15.25 when output equals 140 haircuts. If the firm wants to maximize its profit or minimize its losses, how many haircuts will it produce and what price should it charge? Explain your answer.

b. Calculate the firm's profit or loss.

c. What is likely to happen in this industry over time as it moves to its new long-run equilibrium?

d. Suppose the barber shop depicted in the diagram remains in the industry. Is this barber shop likely to produce this same quantity of haircuts as in part (a) in the long run?

-Refer to Figure 13-16. Figure 13-16 depicts a monopolistically competitive barber shop. Use the diagram to answer the following questions.

a. Suppose the average variable cost of production is $15 when output equals 110 haircuts and $15.25 when output equals 140 haircuts. If the firm wants to maximize its profit or minimize its losses, how many haircuts will it produce and what price should it charge? Explain your answer.

b. Calculate the firm's profit or loss.

c. What is likely to happen in this industry over time as it moves to its new long-run equilibrium?

d. Suppose the barber shop depicted in the diagram remains in the industry. Is this barber shop likely to produce this same quantity of haircuts as in part (a) in the long run?

(Essay)

4.8/5 (45)

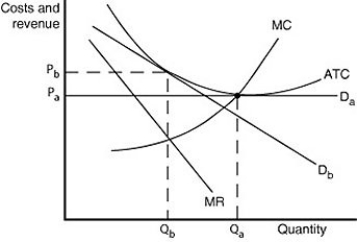

Figure 13-18  -Refer to Figure 13-18. Which of the following statements is true?

-Refer to Figure 13-18. Which of the following statements is true?

(Multiple Choice)

4.8/5 (25)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)