Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models459 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System492 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply476 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes420 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods262 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply293 Questions

Exam 7: The Economics of Health Care337 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance512 Questions

Exam 9: Comparative Advantage and the Gains From International Trade377 Questions

Exam 10: Consumer Choice and Behavioral Economics304 Questions

Exam 11: Technology, Production, and Costs326 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting272 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets256 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy258 Questions

Exam 17: The Markets for Labor and Other Factors of Production279 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: Gdp: Measuring Total Production and Income260 Questions

Exam 20: Unemployment and Inflation290 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles251 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies261 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run305 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis286 Questions

Exam 25: Money, Banks, and the Federal Reserve System278 Questions

Exam 26: Monetary Policy280 Questions

Exam 27: Fiscal Policy313 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy277 Questions

Exam 30: The International Financial System258 Questions

Select questions type

Firms use two marketing tools to differentiate their products. What are these two tools?

(Multiple Choice)

4.8/5  (35)

(35)

How does the long-run equilibrium of a monopolistically competitive industry differ from that of a perfectly competitive industry?

(Multiple Choice)

4.7/5 (42)

In San Francisco there are many restaurants that specialize in a wide variety of cuisines. Patronage at these restaurants is influenced by factors such as tastes, price, and location. This market is

(Multiple Choice)

4.9/5 (36)

Explain the significance of brand management to a firm that has differentiated its product. Comment specifically on the importance of obtaining a trademark.

(Essay)

4.8/5 (38)

Which of the following is true for a monopolistically competitive firm in long-run equilibrium?

(Multiple Choice)

4.8/5 (43)

Long-run equilibrium under monopolistic competition is similar to that under perfect competition in that

(Multiple Choice)

5.0/5 (52)

A major difference between monopolistic competition and perfect competition is

(Multiple Choice)

4.8/5 (36)

Being the first to sell a particular good can give a firm advantages over other firms that sell similar products. What is the name given to these advantages?

(Multiple Choice)

5.0/5 (38)

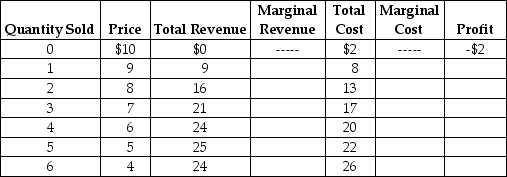

Table 13-4

Table 13-4 lists estimated revenues and costs (per week) for plastic vials (100 vials per box) for the Victoria Biological Supplies Company. Victoria sells plastic vials to universities and private research laboratories.

-Refer to Table 13-4. Victoria's profit-maximizing quantity (Q) and price (P) are

Table 13-4 lists estimated revenues and costs (per week) for plastic vials (100 vials per box) for the Victoria Biological Supplies Company. Victoria sells plastic vials to universities and private research laboratories.

-Refer to Table 13-4. Victoria's profit-maximizing quantity (Q) and price (P) are

(Multiple Choice)

4.7/5 (35)

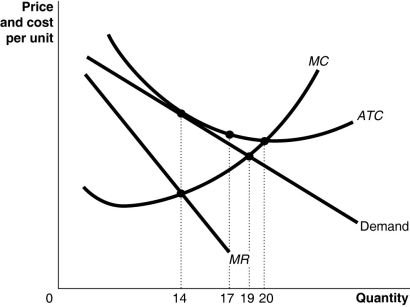

Figure 13-19  -Refer to Figure 13-19 to answer the following questions.

a. What is the productively efficient output?

b. What is the allocatively efficient output?

c. What is the amount of excess capacity?

d. Suppose the firm is currently producing 14 units. What happens if it increases output to 17 units?

-Refer to Figure 13-19 to answer the following questions.

a. What is the productively efficient output?

b. What is the allocatively efficient output?

c. What is the amount of excess capacity?

d. Suppose the firm is currently producing 14 units. What happens if it increases output to 17 units?

(Essay)

4.9/5 (33)

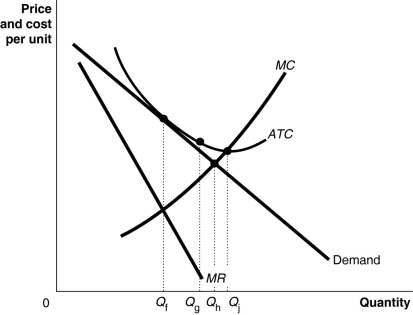

Figure 13-17  -Refer to Figure 13-17. What is the amount of excess capacity?

-Refer to Figure 13-17. What is the amount of excess capacity?

(Multiple Choice)

4.8/5 (31)

If a significant number of consumers switch from ordering food delivery from traditional restaurants to ordering from "ghost restaurants", a "ghost restaurant" will likely find its demand curve shifting to the ________ and its marginal revenue curve shifting to the ________ as more competitors enter the market.

(Multiple Choice)

4.9/5 (32)

Which of the following is not a characteristic of monopolistic competition?

(Multiple Choice)

4.8/5 (32)

Only one of the following statements is correct. The statements compare perfectly competitive (PC) markets and monopolistically competitive (MC) markets. Which statement is correct?

(Multiple Choice)

4.7/5 (42)

When new firms are encouraged to enter a monopolistically competitive market

(Multiple Choice)

4.7/5 (35)

Which of the following will not happen as a consequence of a monopolistically competitive firm suffering economic losses in the short run?

(Multiple Choice)

4.7/5 (38)

Which of the following is not an example of a monopolistically competitive market?

(Multiple Choice)

4.8/5 (42)

If firms in a monopolistically competitive market are earning economic profits, which of the following scenarios best reflects the change a representative firm experiences as the market adjusts to its long-run equilibrium?

(Multiple Choice)

4.9/5 (38)

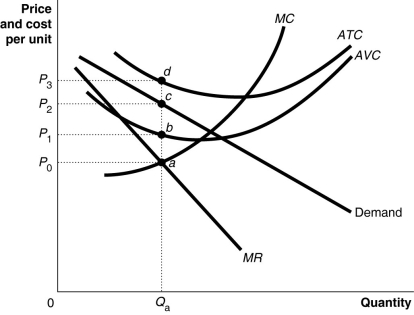

Figure 13-4  Figure 13-4 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-4. What is the area that represents the total revenue made by the firm?

Figure 13-4 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-4. What is the area that represents the total revenue made by the firm?

(Multiple Choice)

4.9/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)