Exam 7: Fraud, Internal Control, and Cash

Exam 1: Accounting in Action276 Questions

Exam 2: The Recording Process223 Questions

Exam 3: Adjusting the Accounts303 Questions

Exam 4: Completing the Accounting Cycle262 Questions

Exam 5: Accounting for Merchandising Operations244 Questions

Exam 6: Inventories257 Questions

Exam 7: Fraud, Internal Control, and Cash238 Questions

Exam 8: Accounting for Receivables269 Questions

Exam 9: Plant Assets, Natural Resources, and Intangible Assets339 Questions

Exam 10: Liabilities317 Questions

Exam 11: Corporations: Organization, Share Transactions, Dividends, and Retained Earnings352 Questions

Exam 12: Investments227 Questions

Exam 13: Statement of Cash Flows213 Questions

Exam 14: Financial Statement Analysis231 Questions

Exam 15: Accounting and Financial Reporting for Contingent Liabilities and Leases281 Questions

Select questions type

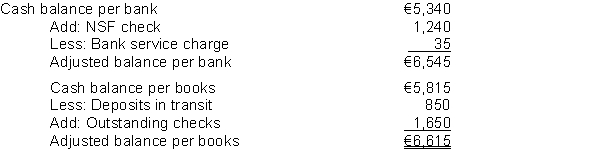

In preparing its August 31, 2014 bank reconciliation, Acme Corp. has the following information available.  At August 31, 2014, Acme's adjusted cash balance is

At August 31, 2014, Acme's adjusted cash balance is

(Multiple Choice)

4.8/5  (37)

(37)

An application of good internal control over cash disbursements is

(Multiple Choice)

4.8/5 (43)

Requiring employees to take vacations is a weakness in the system of internal controls because it does not promote operational efficiency.

(True/False)

4.9/5 (46)

Identify which principle of internal control is being followed in each of the following cases.

1. Warehouse employees do not have access to the accounting records.

2. Prenumbered shipping documents are prepared for each shipment of goods.

3. The locked warehouse is accessible only by warehouse employees with keys.

(Essay)

4.8/5 (35)

If a check correctly written and paid by the bank for ¥4,710 is incorrectly recorded on the company's books for ¥4,170, the appropriate treatment on the bank reconciliation would be to

(Multiple Choice)

4.8/5 (33)

Control over cash disbursements is generally more effective when

(Multiple Choice)

4.7/5 (39)

Cash equivalents are currently reported as short-term investments on the statement of financial position.

(True/False)

4.8/5 (33)

Electronic Funds Transfer (EFT) is a disbursement system that uses telephone or computer to transfer cash from one location to another.

(True/False)

4.9/5 (38)

Dillman Food Store developed the following information in recording its bank statement for the month of March.  -------------------------------------------

(1) Checks written in March but still outstanding $6,000.

(2) Checks written in February but still outstanding $2,800.

(3) Deposits of March 30 and 31 not yet recorded by bank $5,200.

(4) NSF check of customer returned by bank $1,200.

(5) Check No. 210 for $594 was correctly issued and paid by bank but incorrectly entered in the cash payments journal as payment on account for $549.

(6) Bank service charge for March was $50.

(7) A payment on account was incorrectly entered in the cash payments journal and posted to the accounts payable subsidiary ledger for $824 when Check No. 318 was correctly prepared for $284. The check cleared the bank in March.

(8) The bank collected a note receivable for the company for $5,000 plus $150 interest revenue.

Instructions

Prepare a bank reconciliation at March 31.

-------------------------------------------

(1) Checks written in March but still outstanding $6,000.

(2) Checks written in February but still outstanding $2,800.

(3) Deposits of March 30 and 31 not yet recorded by bank $5,200.

(4) NSF check of customer returned by bank $1,200.

(5) Check No. 210 for $594 was correctly issued and paid by bank but incorrectly entered in the cash payments journal as payment on account for $549.

(6) Bank service charge for March was $50.

(7) A payment on account was incorrectly entered in the cash payments journal and posted to the accounts payable subsidiary ledger for $824 when Check No. 318 was correctly prepared for $284. The check cleared the bank in March.

(8) The bank collected a note receivable for the company for $5,000 plus $150 interest revenue.

Instructions

Prepare a bank reconciliation at March 31.

(Essay)

4.8/5 (36)

Identify the internal control procedures applicable to cash receipts for Ferguson Company in each of the following cases.

1. All cashiers are bonded.

2. The treasurer compares the total cash receipts to the bank deposit daily.

3. The bookkeeper records cash receipts which are held by the treasurer.

4. Only the treasurer holds cash receipts.

5. Deposit slips are completed for each deposit.

(Essay)

4.7/5 (35)

Gordon Company is unable to reconcile the bank balance at January 31. Gordon's reconciliation is as follows.  Instructions

(a) Prepare a correct bank reconciliation.

(b) Journalize the entries required by the reconciliation.

Instructions

(a) Prepare a correct bank reconciliation.

(b) Journalize the entries required by the reconciliation.

(Essay)

4.8/5 (33)

Proper control for over-the-counter cash receipts includes

(Multiple Choice)

5.0/5 (33)

If a petty cash fund is established in the amount of ₤250, and contains ₤145 in cash and ₤100 in receipts for disbursements when it is replenished, the journal entry to record replenishment should include credits to which of the following accounts?

(Multiple Choice)

4.8/5 (37)

Personnel who handle cash receipts should have the option of taking a vacation or not.

(True/False)

4.8/5 (41)

A disbursement system that uses wire, telephone, computers, etc., to transfer cash from one location to another is referred to as ______________.

(Not Answered)

This question doesn't have any answer yet

Bertram Company assembled the following information in completing its May bank reconciliation: balance per bank ₤23,460 outstanding checks ₤5,325; deposits in transit ₤3,750; NSF check ₤2,040; bank service charge ₤75; cash balance per books ₤24,000. As a result of this reconciliation, Bertram will

(Multiple Choice)

4.8/5 (47)

Listed below are seven errors or problems which might occur in the processing of cash transactions. Also shown is a list of internal control principles. Evaluate each possible error and cite a principle that is listed that would reduce the probability of the error occurring. If none of the principles given will correct the problem, write "None." If you think more than one principle is appropriate, list all principles that apply.

Possible Errors or Problems

1. An employee steals the cash collected from a customer for an account receivable and conceals this theft by issuing a credit memorandum indicating that the customer returned the merchandise.

2. A small fire destroys 3 days of cash receipts.

3. The official designated to sign checks is able to steal blank checks and issue them without fear of detection.

4. A salesclerk in serving customers often rings up a sale for less than the actual amount and then keeps the additional cash collected from the customer.

5. Three cashiers use one cash register drawer and the cash in the drawer is often short of the balance kept on hand.

6. Each cashier counts his own register drawer each day and verbally reports the results to the supervisor.

7. Cashiers with over 5 years' experience are not bonded.

Internal Control Principles

a. Establishment of responsibility

b. Segregation of duties

c. Physical controls

d. Documentation procedures

e. Independent internal verification

(Essay)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)