Exam 8: Short-Run Costs and Output Decisions

Exam 1: The Scope and Method of Economics68 Questions

Exam 2: The Economic Problem: Scarcity and Choice50 Questions

Exam 3: Demand, Supply, and Market Equilibrium52 Questions

Exam 4: Demand and Supply Applications41 Questions

Exam 5: Elasticity74 Questions

Exam 6: Household Behavior and Consumer Choice50 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms64 Questions

Exam 8: Short-Run Costs and Output Decisions59 Questions

Exam 9: Long-Run Costs and Output Decisions87 Questions

Exam 10: Input Demand: the Labor and Land Markets77 Questions

Exam 11: Input Demand: the Capital Market and the Investment Decision66 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition44 Questions

Exam 13: Monopoly and Antitrust Policy45 Questions

Exam 14: Oligopoly53 Questions

Exam 15: Monopolistic Competition31 Questions

Exam 16: Externalities, Public Goods, and Social Choice54 Questions

Select questions type

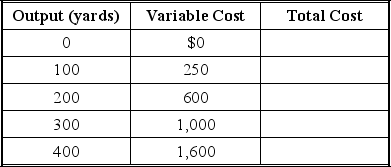

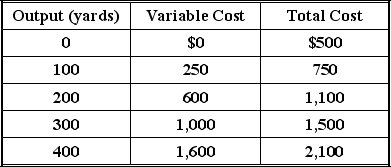

Mark's Fabrics produces fabric for window curtains. The firm's fixed costs are $500 per day. The firm's variable costs vary with the level of output as follows:

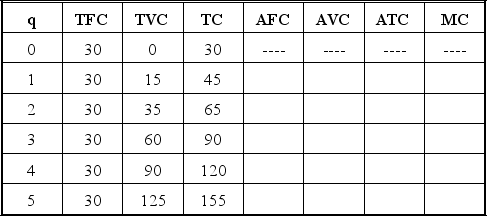

Fill in the column for total cost.

Fill in the column for total cost.

Free

(Essay)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

What two things does the level of total variable costs depend on?

Free

(Essay)

4.8/5 (42)

Correct Answer:Verified

(1.) The techniques of production which are available. (2.) The prices of inputs required by each technology.

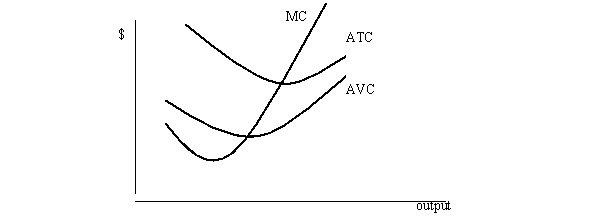

Draw average variable cost, average total cost, and marginal cost on the same set of axes.

Free

(Essay)

4.8/5 (26)

Correct Answer:Verified

Marginal cost intersects average variable cost at minimum average variable cost. Marginal cost intersects average total cost at minimum average total cost. In addition, the average variable cost and average total cost curves become closer as output rises.

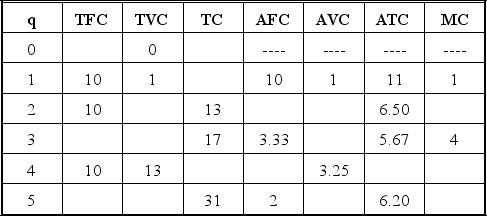

Laura's Cookie Company faces the following cost schedule for making cookies by the dozen:

Fill in the blanks above.

Fill in the blanks above.

(Essay)

4.8/5 (31)

What is the relationship between total variable cost and marginal cost? Explain.

(Essay)

5.0/5 (31)

The equation for the firm's total variable costs is given by TVC = 5q. The firm's total fixed costs are $10. What is the equation for the firm's TC curve? Draw the firm's TVC, TFC, TC, MC, AVC, and ATC cost curves. Does the firm's cost curve have the usual shape? Why or why not?

(Essay)

4.8/5 (29)

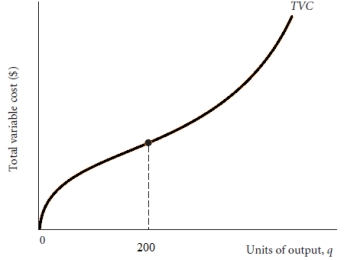

Using the graph below draw a marginal cost curve that would likely be the result. Use the output level of 200 as a reference point and explain why you drew it the way you did.

(Essay)

4.8/5 (34)

What is meant by variable cost? What kinds of things might be included in variable cost?

(Essay)

4.9/5 (39)

White Paper Company faces the following cost schedule for producing reams of paper:

Fill in the columns for average fixed cost, average variable cost, average total cost, and marginal cost.

Fill in the columns for average fixed cost, average variable cost, average total cost, and marginal cost.

(Essay)

4.7/5 (37)

Explain how it might be possible for the total variable cost function to be linear? Explain.

(Essay)

4.8/5 (27)

If a firm shuts down in the short run, will it have zero costs or not? Explain.

(Essay)

4.7/5 (31)

Assume that you have data on a firm's average fixed cost and average variable cost for various levels of output and you are asked to calculate the total variable cost and total cost of the firm. Would this be enough information to perform this calculation? Explain

(Essay)

4.8/5 (30)

What is the relationship between average total cost, average variable cost, and average fixed cost? If average total cost is $5.76 and average fixed cost is $1.35, what is the level of average variable cost?

(Essay)

4.7/5 (38)

Assume a firm is operating under conditions of pure competition and faces a marginal cost function that is everywhere below its average total cost. If the firm is producing where marginal revenue equals marginal cost will it be possible for it to make an economic profit? Explain.

(Essay)

4.8/5 (39)

If General Motors cuts back production on the Hummer because of high gasoline prices what should you expect to happen to the average fixed cost of production? What about the average total cost?

(Essay)

4.9/5 (29)

How is it possible for marginal cost to equal to the slope of either the total variable cost function or the total cost function?

(Essay)

4.8/5 (33)

Assume that we only have data on total cost when output is equal to zero and no other cost information at our disposal. How could we possibly know what the fixed costs are for the firm?

(Essay)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)