Exam 20: Forming and Operating Partnerships

The character of each separately-stated item is determined at the partner level.

False

Which of the following statements regarding a partner's basis adjustments is true?

C

What is the difference between the aggregate and entity theory of partnership taxation? Provide two examples of how partnership tax rules reflect the aggregate theory and two examples of how they reflect the entity theory.

The aggregate theory treats a partnership as an aggregation of the partners' undivided interests in the partnership's assets and liabilities. On the other hand, the entity theory views

partnerships as distinct entities separate from their owners. In reality, partnership tax rules are a hybrid of these two approaches. Partnership tax rules use the aggregate theory in the way

they (1) treat partnerships as flow-through entities, (2) specially allocate built-in gains and

built-in losses to the partners contributing these assets, and (3) treat distributions to partners as generally nontaxable. Partnership tax rules use the entity theory in the way they (1) require partnerships rather than partners to make the majority of tax elections, (2) characterize gains and losses at the partnership level, and (3) require the partnership to file a return.

On 12/31/X4, Zoom, LLC reported a $60,000 loss on its books. The items included in the loss computation were $30,000 in sales revenue, $15,000 in qualified dividends,$22,000 in cost of goods sold, $50,000 charitable contribution, $20,000 in employee wages, and $13,000 of rent expense. How much ordinary business income (loss) will Zoom report on its X4 return?

Explain why partners must increase their tax basis for their share of partnership taxable and nontaxable income or gain and reduce their basis by their share of partnership deductible and nondeductible expenses or losses?

A partnership can elect to amortize organization and startup costs; however, syndicationcosts are not deductible.

This year, Reggie's distributive share from Almonte Partnership includes $8,000 of interest income, $4,000 of dividend income, and $60,000 ordinary business income.A. Assume that Reggie materially participates in the partnership. How much of his distributive share fromAlmonte Partnership is potentially subject to the Medicare contribution tax?B. Assume that Reggie does not materially participate in the partnership. How much of his distributive share from Almonte Partnership is potentially subject to the Medicare contribution tax?

A partnership with a C corporation partner must always use the accrual method as its accounting method.

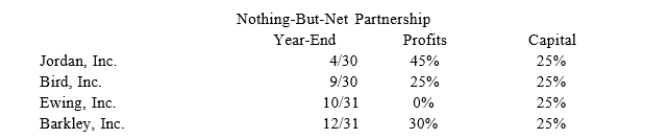

Jordan, Inc., Bird, Inc., Ewing, Inc., and Barkley, Inc. formed Nothing-But-Net Partnership on June1st, 20X9. Now, Nothing-But-Net must adopt its required tax year-end. The partners' year-ends, profitsinterests, and capital interests are reflected in the table below. Given this information, what tax year-end mustNothing-But-Net use and what rule requires this year-end?

An additional allocation of partnership debt or relief of partnership debt is considered to be a deemed cash contribution or cash distribution respectively.

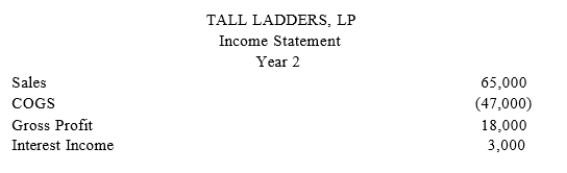

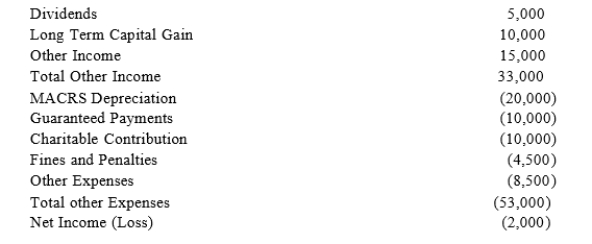

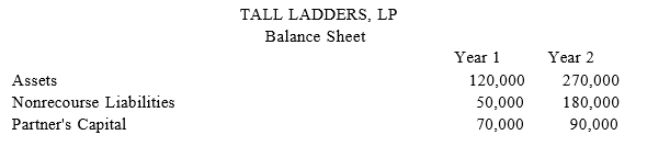

At the end of year 1, Tony had a tax basis of $40,000 in Tall Ladders, Limited Partnership. Tony has a 20 percent profits interest in Tall Ladders. For year 2, Tall Ladders will pay Tony a $10,000guaranteed payment for extra services he provides to the partnership. Given the following IncomeStatement and Balance Sheet from Tall Ladders, what is Tony's adjusted tax basis at the end of year 2?

Under proposed regulations issued by the Treasury Department, in which of the following situations should an LLC member be treated as a general partner for self-employment tax purposes?

How does additional debt or relief of debt affect a partner's basis?

Jerry, a partner with 30% capital and profit interest, received his Schedule K-1 from Plush Pillows, LP. At the beginning of the year, Jerry's tax basis in his partnership interest was $50,000. His current year Schedule K-1 reported an ordinary loss of$15,000, long-term capital gain of $3,000, qualified dividends of $2,000, $500 ofnon-deductible expenses, a $10,000 cash contribution, and a reduction of $4,000 in his share of partnership debt. What is Jerry's adjusted basis in his partnership interest at the end of the year?

On April 18, 20X8, Robert sold his 35 percent partnership interest in Fruit Wonder, LLC to Richard for $120,000. Prior to selling his interest, Robert had a basis in Fruit Wonder of $80,000. Robert's basis included $5,000 of recourse debt and $15,000 of nonrecourse debt that had been allocated to him. Immediately after the purchase, what is Richard's tax basis in Fruit Wonder?

Why are guaranteed payments deducted in calculating the ordinary business income (loss) of partnerships and treated as a separately-stated item for the partners that receive the payment?

For partnership tax years ending after December 31, 2015, when must a partnership file its return?

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales -$150,000, Cost of Goods Sold - $90,000, Depreciation Expense - $45,000, Long-TermCapital Gains - $15,000, Qualified Dividends - $6,000, and Municipal Bond Interest -$3,000. How much ordinary business income (loss) will Bright Line allocate to Kim on her Schedule K-1 for X4?

On January 1, X9, Gerald received his 50% profits and capital interest in High Air, LLCin exchange for $2,000 in cash and real property with a $3,000 tax basis secured by a$2,000 nonrecourse mortgage. High Air reported a $15,000 loss for its X9 calendar year. How much loss can Gerald deduct, and how much loss must he suspend if he onlyapplies the tax basis loss limitation?

In each of the independent scenarios below, how does the partner or partnership determine its holding period in the property received?a. A partner contributes property in exchange for a partnership interest b. The partnership receives contributed propertyc. A partner contributes services in exchange for a partnership interest d. A partner purchases a partnership interest from an existing partner

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)