Exam 20: Forming and Operating Partnerships

Exam 1: An Introduction to Tax110 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities112 Questions

Exam 3: Tax Planning Strategies and Related Limitations107 Questions

Exam 4: Individual Income Tax Overview, Exemptions, and Filing Status126 Questions

Exam 5: Gross Income and Exclusions131 Questions

Exam 6: Individual Deductions107 Questions

Exam 7: Investments75 Questions

Exam 8: Individual Income Tax Computation and Tax Credits154 Questions

Exam 9: Business Income, Deductions, and Accounting Methods99 Questions

Exam 10: Property Acquisition and Cost Recovery94 Questions

Exam 11: Property Dispositions110 Questions

Exam 12: Compensation102 Questions

Exam 13: Retirement Savings and Deferred Compensation115 Questions

Exam 14: Tax Consequences of Home Ownership111 Questions

Exam 15: Entities Overview70 Questions

Exam 16: Corporate Operations140 Questions

Exam 17: Accounting for Income Taxes100 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions98 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 20: Forming and Operating Partnerships102 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 22: S Corporations134 Questions

Exam 23: State and Local Taxes117 Questions

Exam 24: The US Taxation of Multinational Transactions100 Questions

Exam 25: Transfer Taxes and Wealth Planning123 Questions

Select questions type

This year, HPLC, LLC was formed by H Inc., P Inc., L Inc., and C Inc. Each member had an equal share in the LLC's capital. H Inc., P Inc., and L Inc. each had a 30% profitsinterest in the LLC with C Inc. having a 10% profits interest. The members had the following tax year-ends: H Inc. [1/31], P Inc. [5/31], L Inc. [7/31], and C Inc. [10/31]. What tax year-end must the LLC use?

(Multiple Choice)

4.8/5  (46)

(46)

Nonrecourse debt is generally allocated according to the profit-sharing ratios of thepartnership.

(True/False)

4.8/5 (29)

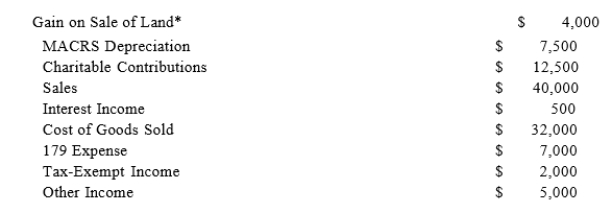

ER General Partnership, a medical supplies business, states in its partnership agreement that Erin and Ryan agree to split profits and losses according to a 40/60 ratio. Additionally, the partnership will provide Erin with a $15,000 guaranteed payment for services she provides to the partnership.ER Partnership reports the following revenues, expenses, gains, losses, and distributions for its current taxable year:  *The Land is a Section 1231 assetGiven these items, answer the following questions:A. Compute Erin's share of ordinary income (loss) and separately-stated items. Include her self-employment income as a separately-stated item.B. Compute Erin's self-employment income, except assume ER Partnership is a limited partnership and Erin is a limited partner.C. Compute Erin's self-employment income, except assume ER Partnership is an LLC and Erin ispersonally liable for half of the debt of the LLC. Apply the IRS's proposed regulations in formulating your answer.

*The Land is a Section 1231 assetGiven these items, answer the following questions:A. Compute Erin's share of ordinary income (loss) and separately-stated items. Include her self-employment income as a separately-stated item.B. Compute Erin's self-employment income, except assume ER Partnership is a limited partnership and Erin is a limited partner.C. Compute Erin's self-employment income, except assume ER Partnership is an LLC and Erin ispersonally liable for half of the debt of the LLC. Apply the IRS's proposed regulations in formulating your answer.

(Essay)

4.9/5 (31)

Partnerships tax rules incorporate both the entity and aggregate approaches.

(True/False)

4.7/5 (31)

A general partner's share of ordinary business income is similar to investment income;thus, a general partner only includes their guaranteed payments as self-employment income.

(True/False)

4.7/5 (33)

Which of the following entities is not considered a flow-through entity?

(Multiple Choice)

4.8/5 (37)

Partnerships may maintain their capital accounts according to which of the following rules?

(Multiple Choice)

4.8/5 (38)

Which of the following statements regarding capital and profit interests received for services contributed to a partnership is false?

(Multiple Choice)

4.8/5 (35)

Which of the following items are subject to the Net Investment Income tax when a partner is a not a material participant in the partnership?

(Multiple Choice)

4.8/5 (38)

Which of the following statements regarding partnerships losses suspended by the tax basis limitation is true?

(Multiple Choice)

4.9/5 (47)

John, a limited partner of Candy Apple, LP, is allocated $30,000 of ordinary businessloss from the partnership. Before the loss allocation, his tax basis is $20,000 and at-risk amount is $10,000. John also has ordinary business income of $20,000 from Sweet Pea, LP as a general partner and ordinary business income of $5,000 from Red Tomato, as a limited partner. How much of the $30,000 loss from Candy Apple can John deduct currently?

(Multiple Choice)

5.0/5 (43)

Which requirement must be satisfied in order to specially allocate partnership income or losses to partners?

(Multiple Choice)

4.9/5 (46)

What type of debt is not included in calculating a partner's at-risk amount?

(Multiple Choice)

4.9/5 (35)

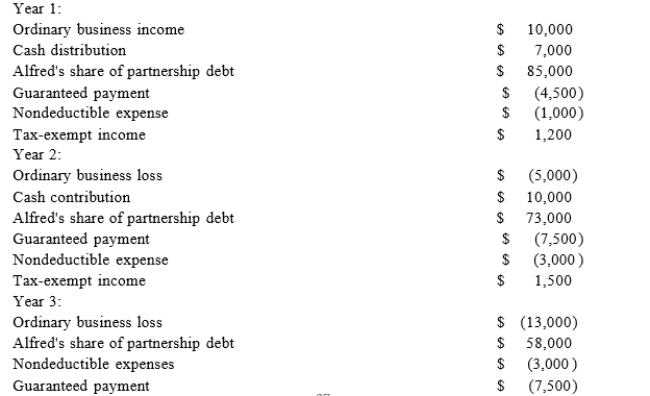

Alfred, a one-third profits and capital partner in Pizzeria Partnership needs help in adjusting his tax basis to reflect the information contained in his most recent Schedule K-1 from the partnership. Unfortunately, the Schedule K-1 he recently received was for year 3 of the partnership, but Alfredonly knows that his tax basis at the beginning of year 2 of the partnership was $23,000. Thankfully, Alfred still has his Schedule K-1 from the partnership for years 1 and 2.Using the following information from Alfred's year 1, year 2, and year 3 Schedule K-1, calculate his tax basis the end of year 2 and year 3.

(Essay)

4.8/5 (39)

The main difference between a partner's tax basis and at-risk amount is that qualified nonrecourse financing is not included in the at-risk basis amount.

(True/False)

4.8/5 (44)

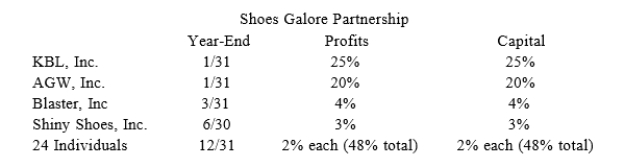

KBL, Inc., AGW, Inc., Blaster, Inc., Shiny Shoes, Inc., and a group of 24 individuals form Shoes Galore General Partnership on October 11, 20X9. Now, Shoes Galore must adopt its required tax year-end. The partners' year-ends, profits interests, and capital interests are reflected in the table below. Given this information, what tax year-end must Shoes Galore use and what rule requires this year-end?

(Essay)

4.8/5 (34)

Income earned by flow-through entities is usually taxed only once at the entity level.

(True/False)

4.9/5 (34)

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax basis at the beginning of the20X8: (1) Jane, a member with a 25% profits and capital interest and a $5,000 outside basis, (2) Joe, a member with a 45% profits and capital interest and a $10,000 outside basis, and (3) Jack, a member with a 30% profits and capital interest and a $2,000 outside basis. The following items were reported on Styling's Schedule K for the year: ordinary income of $100,000, Section 1231 gain of $15,000, charitable contributions of$25,000, and tax-exempt income of $3,000. In addition, Styling received an additional bank loan of $12,000 during 20X8. What is Jane's tax basis after adjustment for her share of these items?

(Multiple Choice)

4.9/5 (29)

In what order should the tests to determine a partnership's year end be applied?

(Multiple Choice)

4.9/5 (38)

Partnerships can use special allocations to shift built-in gains and built-in losses on contributed property from a partner who contributed the property to other partners.

(True/False)

4.8/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)