Exam 9: The Nature and Creation of Money

Exam 1: Economics: the Study of Choice138 Questions

Exam 2: Confronting Scarcity: Choices in Production193 Questions

Exam 3: Demand and Supply243 Questions

Exam 4: Applications of Demand and Supply108 Questions

Exam 5: Macroeconomics: the Big Picture243 Questions

Exam 6: Measuring Total Output and Income228 Questions

Exam 7: Aggregate Demand and Aggregate Supply223 Questions

Exam 8: Economic Growth221 Questions

Exam 9: The Nature and Creation of Money267 Questions

Exam 10: Monopoly229 Questions

Exam 11: The World of Imperfect Competition227 Questions

Exam 12: Wages and Employment in Perfect Competition173 Questions

Exam 13: Interest Rates and the Markets for Capital and Natural Resources161 Questions

Exam 14: Imperfectly Competitive Markets for Factors of Production178 Questions

Exam 15: Public Finance and Public Choice179 Questions

Exam 16: Inflation and Unemployment132 Questions

Exam 17: International Trade179 Questions

Exam 18: The Economics of the Environment144 Questions

Exam 19: Inequality, Poverty, and Discrimination134 Questions

Exam 20: Macroeconomics: the Big Picture104 Questions

Exam 21: Measuring Total Income and Output134 Questions

Exam 22: Aggregate Demand and Aggregate Supply120 Questions

Exam 23: Economic Growth124 Questions

Exam 24: The Nature and Creation of Money183 Questions

Exam 25: Financial Markets and the Economy158 Questions

Exam 26: Monetary Policy and the Fed175 Questions

Exam 27: Government and Fiscal Policy177 Questions

Exam 28: Consumption and the Aggregate Expenditures Model199 Questions

Exam 29: Investment and Economic Activity115 Questions

Exam 30: Net Exports and International Finance202 Questions

Exam 31: Macro Inflation and Unemployment135 Questions

Exam 32: Macro a Brief History of Macroeconomic Thought and Policy120 Questions

Exam 33: Economic Development107 Questions

Exam 34: Socialist Economies in Transition129 Questions

Select questions type

In the long run, provided that there are no external benefits or costs, perfect competition will result in an efficient allocation of resources because:

(Multiple Choice)

4.8/5  (42)

(42)

If some firms in a perfectly competitive industry earn less than a zero economic profit, the industry's market supply curve will decrease in the long run.

(True/False)

5.0/5 (46)

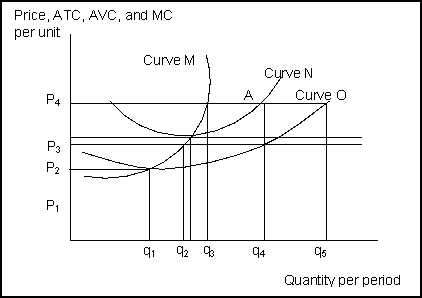

Use the following to answer questions  -(Exhibit: Profit Maximizing)The exhibit shows cost curves for a firm operating in a perfectly competitive market.If the market price is P4:

-(Exhibit: Profit Maximizing)The exhibit shows cost curves for a firm operating in a perfectly competitive market.If the market price is P4:

(Multiple Choice)

4.8/5 (40)

An increase in demand in a perfectly competitive market will cause a(n):

(Multiple Choice)

4.8/5 (42)

A reduction in variable production costs shifts the firm's _______ and _______ curves _______ in the short run.

(Multiple Choice)

4.8/5 (31)

Costs included in the economic concept of cost but that are not an explicit cost are:

(Multiple Choice)

5.0/5 (40)

Suppose life is discovered on Mars and that it turns out to be quite sophisticated.In fact, perfect competition prevails everywhere on the planet.Which of the following characteristics of Martian firms are we likely to observe?

(Multiple Choice)

4.9/5 (29)

If firms are experiencing economic losses in the short run, firms will leave the industry and industry output will _______ and economic losses will _______ in the long run.

(Multiple Choice)

4.8/5 (45)

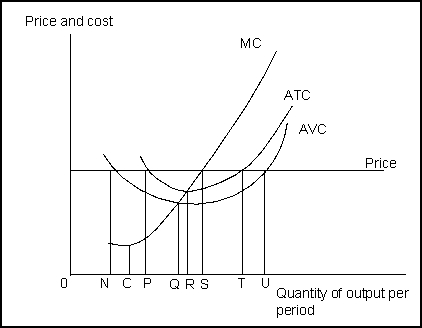

Use the following to answer questions 142-145:  -(Exhibit: Short-Run Costs)If the price declines, production will continue in the short run, even though the firm incurs a loss, between quantities:

-(Exhibit: Short-Run Costs)If the price declines, production will continue in the short run, even though the firm incurs a loss, between quantities:

(Multiple Choice)

4.9/5 (39)

Suppose that some firms in a perfectly competitive industry are earning positive economic profits.In the long run, the:

(Multiple Choice)

4.8/5 (42)

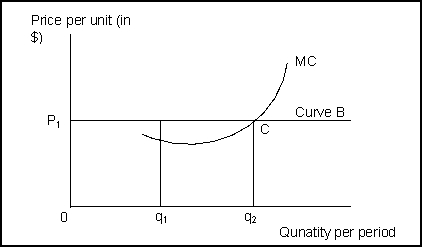

Use the following to answer questions 80-84:  -(Exhibit: Marginal Decision Rule)Economic profit:

-(Exhibit: Marginal Decision Rule)Economic profit:

(Multiple Choice)

4.7/5 (33)

Use the following to answer questions 129-135:

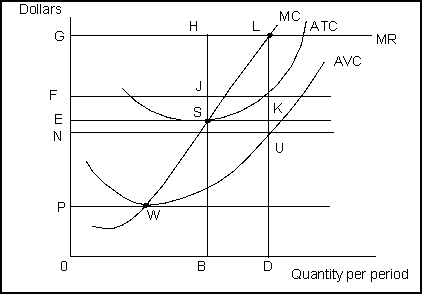

-(Exhibit: A Perfectly Competitive Firm in the Short Run)The firm's total economic profit at its most profitable level of output is:

-(Exhibit: A Perfectly Competitive Firm in the Short Run)The firm's total economic profit at its most profitable level of output is:

(Multiple Choice)

4.9/5 (33)

The profit-maximizing level of output for a perfectly competitive firm occurs at the quantity at which the slopes of the marginal cost and marginal revenue curves are equal.

(True/False)

4.7/5 (34)

The profit-maximizing level of output for a perfectly competitive firm occurs where:

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)