Exam 9: The Nature and Creation of Money

Exam 1: Economics: the Study of Choice138 Questions

Exam 2: Confronting Scarcity: Choices in Production193 Questions

Exam 3: Demand and Supply243 Questions

Exam 4: Applications of Demand and Supply108 Questions

Exam 5: Macroeconomics: the Big Picture243 Questions

Exam 6: Measuring Total Output and Income228 Questions

Exam 7: Aggregate Demand and Aggregate Supply223 Questions

Exam 8: Economic Growth221 Questions

Exam 9: The Nature and Creation of Money267 Questions

Exam 10: Monopoly229 Questions

Exam 11: The World of Imperfect Competition227 Questions

Exam 12: Wages and Employment in Perfect Competition173 Questions

Exam 13: Interest Rates and the Markets for Capital and Natural Resources161 Questions

Exam 14: Imperfectly Competitive Markets for Factors of Production178 Questions

Exam 15: Public Finance and Public Choice179 Questions

Exam 16: Inflation and Unemployment132 Questions

Exam 17: International Trade179 Questions

Exam 18: The Economics of the Environment144 Questions

Exam 19: Inequality, Poverty, and Discrimination134 Questions

Exam 20: Macroeconomics: the Big Picture104 Questions

Exam 21: Measuring Total Income and Output134 Questions

Exam 22: Aggregate Demand and Aggregate Supply120 Questions

Exam 23: Economic Growth124 Questions

Exam 24: The Nature and Creation of Money183 Questions

Exam 25: Financial Markets and the Economy158 Questions

Exam 26: Monetary Policy and the Fed175 Questions

Exam 27: Government and Fiscal Policy177 Questions

Exam 28: Consumption and the Aggregate Expenditures Model199 Questions

Exam 29: Investment and Economic Activity115 Questions

Exam 30: Net Exports and International Finance202 Questions

Exam 31: Macro Inflation and Unemployment135 Questions

Exam 32: Macro a Brief History of Macroeconomic Thought and Policy120 Questions

Exam 33: Economic Development107 Questions

Exam 34: Socialist Economies in Transition129 Questions

Select questions type

When a perfectly competitive firm is in long-run equilibrium, the firm is:

(Multiple Choice)

4.8/5  (33)

(33)

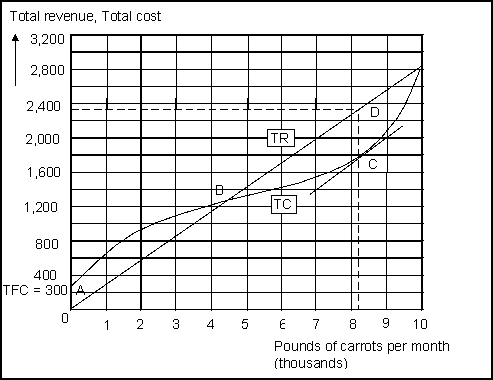

Use the following to answer questions  -(Exhibit: Total Revenue, Total Costs, and Economic Profit)The firm maximizes economic profit when the _______ of the total revenue and total cost curves are _______ and when _______ and ________ are equal.

-(Exhibit: Total Revenue, Total Costs, and Economic Profit)The firm maximizes economic profit when the _______ of the total revenue and total cost curves are _______ and when _______ and ________ are equal.

(Multiple Choice)

4.8/5 (45)

The firm will continue to produce in the short run if P <ATC and P > AVC.

(True/False)

4.9/5 (31)

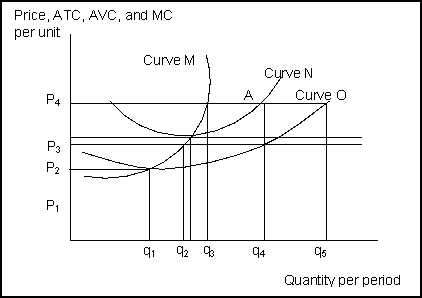

Use the following to answer questions  -(Exhibit: Profit Maximizing)The exhibit shows cost curves for a firm operating in a perfectly competitive market.If the market price is less than P2, the firm will _______ in the short run.

-(Exhibit: Profit Maximizing)The exhibit shows cost curves for a firm operating in a perfectly competitive market.If the market price is less than P2, the firm will _______ in the short run.

(Multiple Choice)

4.8/5 (34)

Provided that there are no external benefits or costs, in the long run, perfect competition will result in an efficient allocation of resources because P = MC.

(True/False)

4.9/5 (38)

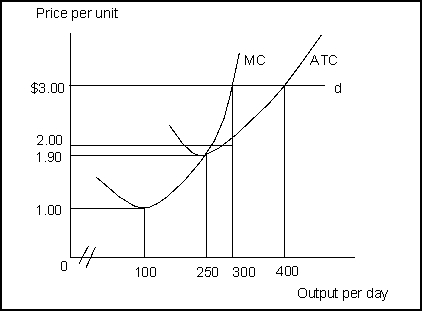

Use the following to answer questions 122-128:  -(Exhibit: Perfectly Competitive Firm)The exhibit shows a perfectly competitive firm that faces demand curve d, has the cost curves shown, and maximizes profit.The firm will produce _______ units of output per day.

-(Exhibit: Perfectly Competitive Firm)The exhibit shows a perfectly competitive firm that faces demand curve d, has the cost curves shown, and maximizes profit.The firm will produce _______ units of output per day.

(Multiple Choice)

4.7/5 (34)

Economic profit in long-run equilibrium in perfect competition will be:

(Multiple Choice)

4.9/5 (43)

Individuals in a market who must take the market price as given are:

(Multiple Choice)

4.8/5 (44)

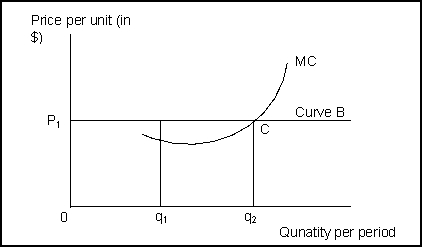

Use the following to answer questions 80-84:  -(Exhibit: Marginal Decision Rule)If P1 is the market price, and if this firm has decided to produce any output, it should produce:

-(Exhibit: Marginal Decision Rule)If P1 is the market price, and if this firm has decided to produce any output, it should produce:

(Multiple Choice)

4.8/5 (38)

A reduction in _______ leads to a _______ , shifting each firm's _______ curve _______ .

(Multiple Choice)

4.9/5 (34)

A firm's total output times the price at which it sells that output is:

(Multiple Choice)

4.9/5 (44)

Use the following to answer questions

-(Exhibit: Total Revenue, Total Costs, and Economic Profit)At zero level of output, total costs are ________ and total revenue is _______ .

(Multiple Choice)

4.9/5 (36)

Charges that are paid for factors of production are called:

(Multiple Choice)

4.9/5 (38)

If a firm in perfect competition sells 10 units of output at a market price of $5 per unit, its marginal revenue is:

(Multiple Choice)

4.7/5 (37)

If price is greater than average total cost at the profit-maximizing quantity of output in the short run, a perfectly competitive firm will:

(Multiple Choice)

4.8/5 (44)

The profit-maximizing level of output for a perfectly competitive firm in the short run occurs where:

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)