Exam 8: Fraud, Internal Control, and Cash

Exam 1: Accounting in Action220 Questions

Exam 2: The Recording Process192 Questions

Exam 3: Adjusting the Accounts216 Questions

Exam 4: Completing the Accounting Cycle203 Questions

Exam 5: Accounting for Merchandising Operations221 Questions

Exam 6: Inventories204 Questions

Exam 7: Accounting Information Systems139 Questions

Exam 8: Fraud, Internal Control, and Cash212 Questions

Exam 9: Accounting for Receivables220 Questions

Exam 10: Plant Assets, Natural Resources, and Intangible Assets293 Questions

Exam 11: Current Liabilities and Payroll Accounting207 Questions

Exam 12: Accounting for Partnerships210 Questions

Exam 13: Corporations: Organization and Capital Stock Transactions195 Questions

Exam 14: Corporations: Dividends, Retained Earnings, and Income Reporting176 Questions

Exam 15: Long-Term Liabilities215 Questions

Exam 16: Investments178 Questions

Exam 17: Statement of Cash Flows203 Questions

Exam 18: Financial Analysis: the Big Picture225 Questions

Exam 19: Managerial Accounting197 Questions

Exam 20: Job Order Costing199 Questions

Exam 21: Process Costing198 Questions

Exam 22: Cost-Volume-Profit217 Questions

Exam 23: Incremental Analysis208 Questions

Exam 24: Budgetary Planning207 Questions

Exam 25: Budgetary Control and Responsibility Accounting207 Questions

Exam 26: Standard Costs and Balanced Scorecard221 Questions

Select questions type

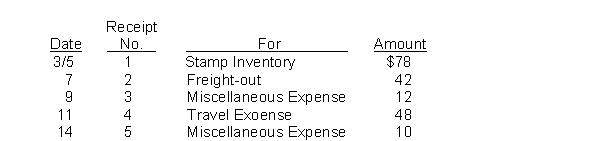

Hemingway Company uses an imprest petty cash system. The fund was established on March 1 with a balance of $200. During March the following petty cash receipts were found in the petty cash box.  The fund was replenished on March 15 when the fund contained $6 in cash. On March 20, the amount in the fund was increased to $300.

Instructions

Journalize the entries in March that pertain to the operation of the petty cash fund.

The fund was replenished on March 15 when the fund contained $6 in cash. On March 20, the amount in the fund was increased to $300.

Instructions

Journalize the entries in March that pertain to the operation of the petty cash fund.

(Essay)

4.8/5  (38)

(38)

Using the code letters below, indicate how each of the items listed would be handled in preparing a bank reconciliation. Enter the appropriate code letter in the space to the left of each item.

Code

A Add to cash balance per books

B Deduct from cash balance per books

C Add to cash balance per bank

D Deduct from cash balance per bank

E Does not affect the bank reconciliation

Items:

1. Outstanding checks.

2. Bank service charge.

3. Check for $320 correctly written and paid by the bank but incorrectly entered in the cash payments journal for $230.

4. Deposit in transit.

5. Bank returns deposited check marked NSF.

6. Bank collects notes receivable and interest for depositor.

7. Bank debit memorandum for check printing fees.

8. Petty cash custodian has $86 in paid petty cash vouchers that have not been reimbursed.

9. Bank charged a check against the company which should have been charged to another company.

10. A check for $236 was correctly paid by the bank but was incorrectly entered in the cash payments journal for $263.

(Essay)

4.8/5 (32)

If a company deposits all its receipts in the bank and pays all its bills by check, then the monthly bank statement balance will always agree with the company's record of its checking account balance.

(True/False)

4.7/5 (39)

The cash records of Sanders Company show the following:

1. In September, deposits per the bank statement totaled $37,600; deposits per books $39,000; and deposits in transit at September 30 were $4,300.

2. In September, cash disbursements per books were $36,500; checks clearing the bank were $37,800; and outstanding checks at September 30 were $2,500.

There were no bank debit or credit memoranda and no errors were made by either the bank or Sanders Company.

Answer the following questions:

(a) What were the deposits in transit at August 31?

(b) What were the outstanding checks at August 31?

(Essay)

4.8/5 (30)

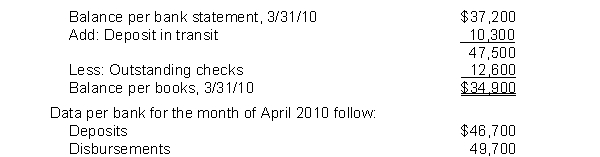

Tyler, Inc. had the following bank reconciliation at March 31. 2010:  All reconciling items at March 31, 2010 cleared the bank in April. Outstanding checks at April 30, 2010 totaled $6,000. There were no deposits in transit at April 30, 2010. What is the cash balance per books at April 30, 2010?

All reconciling items at March 31, 2010 cleared the bank in April. Outstanding checks at April 30, 2010 totaled $6,000. There were no deposits in transit at April 30, 2010. What is the cash balance per books at April 30, 2010?

(Multiple Choice)

4.9/5 (43)

In preparing a bank reconciliation, outstanding checks are ______________ from the cash balance per ______________.

(Short Answer)

4.8/5 (43)

Wynn Company developed the following reconciling information in preparing its September bank reconciliation:  Determine the cash balance per books (before adjustments) for Wynn Company.

Determine the cash balance per books (before adjustments) for Wynn Company.

(Multiple Choice)

4.9/5 (37)

Internal control is most effective when several people are responsible for a given task.

(True/False)

4.8/5 (44)

A segregation of duties among employees eliminates the possibility of collusion.

(True/False)

4.8/5 (46)

The duties of approving an item for payment and paying the item should be done by different departments or individuals.

(True/False)

4.9/5 (35)

The principle of establishing responsibility does not include

(Multiple Choice)

4.7/5 (33)

Controls that enhance the accuracy and reliability of the accounting records are

(Multiple Choice)

4.8/5 (35)

Journal entries are required by the depositor for all of the following except

(Multiple Choice)

4.8/5 (50)

The Foreign Corrupt Practices Act requires that all U.S. corporations under the juris-diction of the Securities and Exchange Commission

(Multiple Choice)

4.8/5 (34)

The use of remittance advices for mail receipts is an example of

(Multiple Choice)

4.9/5 (36)

Control over cash disbursements is generally more effective when

(Multiple Choice)

4.9/5 (30)

Laymon Boat Company's bank statement for the month of September showed a balance per bank of $7,000. The company's Cash account in the general ledger had a balance of $5,459 at September 30. Other information is as follows:

(1) Cash receipts for September 30 recorded on the company's books were $5,700 but this amount does not appear on the bank statement.

(2) The bank statement shows a debit memorandum for $40 for check printing charges.

(3) Check No. 119 payable to Mann Company was recorded in the cash payments journal and cleared the bank for $248. A review of the accounts payable subsidiary ledger shows a $36 credit balance in the account of Mann Company and that the payment to them should have been for $284.

(4) The total amount of checks still outstanding at September 30 amounted to $6,000.

(5) Check No. 138 was correctly written and paid by the bank for $409. The cash payment journal reflects an entry for Check No. 138 as a debit to Accounts Payable and a credit to Cash in Bank for $490.

(6) The bank returned an NSF check from a customer for $360.

(7) The bank included a credit memorandum for $1,560 which represents collection of a customer's note by the bank for the company; principal amount of the note was $1,500 and interest was $60. Interest has not been accrued.

Instructions

(a) Prepare a bank reconciliation for Laymon Boat Company at September 30.

(b) Prepare any adjusting entries necessary as a result of the bank reconciliation.

(Essay)

4.9/5 (40)

Internal controls are not designed to safeguard assets from

(Multiple Choice)

5.0/5 (37)

The following information was used to prepare the March 2010, bank reconciliation for Grider Machine Works. Identify the items that require adjustment to the cash balance per books and prepare the appropriate adjusting entries.

1. Included with the bank statement materials was a check from Bob Simpson for $40 stamped "NSF."

2. A personal deposit by Jim Grider to his personal account in the amount of $300 for dividends on his General Electric common stock was credited to the company account.

3. The bank statement included a debit memorandum for $22.00 for two books of blank checks for Grider Machine Works.

4. The bank statement contains a credit memorandum for $24.75 interest on the average checking account balance.

5. The daily deposits of March 30 and March 31, for $3,362 and $3,125 respectively, were not included in the bank statement postings.

6. Two checks totaling $316.86, which were outstanding at the end of February, cleared in March and were returned with the March statement.

7. The bank statement included a credit memorandum dated March 28, 2008, for $45.00 for the monthly interest on a 6-month, $15,000 certificate of deposit that the company owns.

8. Four checks, #8712, #8716, #8718, #8719, totaling $5,369.65, did not clear the bank during March.

9. On March 24, 2008, Grider Machine Works delivered to the bank for collection a $4,500,

3-month note from Don Decker. A credit memorandum dated March 29, 2008, indicated the collection of the note and $90.00 of interest.

10. The bank statement included a debit memorandum for $25.00 for the collection service on the above note and interest.

(Essay)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)