Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics455 Questions

Exam 2: Thinking Like an Economist643 Questions

Exam 3: Interdependence and the Gains From Trade547 Questions

Exam 4: The Market Forces of Supply and Demand693 Questions

Exam 5: Elasticity and Its Application626 Questions

Exam 6: Supply, Demand, and Government Policies668 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets547 Questions

Exam 8: Applications: the Costs of Taxation509 Questions

Exam 9: Application: International Trade521 Questions

Exam 10: Externalities543 Questions

Exam 11: Public Goods and Common Resources452 Questions

Exam 12: The Design of the Tax System664 Questions

Exam 13: The Costs of Production649 Questions

Exam 14: Firms in Competitive Markets604 Questions

Exam 15: Monopoly662 Questions

Exam 16: Monopolistic Competition649 Questions

Exam 17: Oligopoly522 Questions

Exam 18: The Markets for the Factors of Production592 Questions

Exam 19: Earnings and Discrimination511 Questions

Exam 20: Income Inequality and Poverty478 Questions

Exam 21: The Theory of Consumer Choice570 Questions

Exam 22: Frontiers in Microeconomics461 Questions

Exam 23: Measuring a Nation S Income547 Questions

Exam 24: Measuring the Cost of Living565 Questions

Exam 25: Production and Growth527 Questions

Exam 26: Saving, Investment, and the Financial System637 Questions

Exam 27: Tools of Finance534 Questions

Exam 28: Unemployment and Its Natural Rate701 Questions

Exam 29: The Monetary System540 Questions

Exam 30: Money Growth and Inflation504 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts540 Questions

Exam 32: A Macroeconomic Theory of the Open Economy511 Questions

Exam 33: Aggregate Demand and Aggregate Supply572 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand523 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment536 Questions

Exam 36: Six Debates Over Macroeconomic Policy354 Questions

Select questions type

Suppose there is an early freeze in California that reduces the size of the lemon crop. What happens to consumer surplus in the market for lemons?

(Multiple Choice)

4.8/5  (30)

(30)

Table 7-4

The numbers in Table 7-1 reveal the maximum willingness to pay for a ticket to a Chicago Cubs vs. St. Louis Cardinal's baseball game at Wrigley Field.  -Refer to Table 7-4. If tickets sell for $40 each, then what is the total consumer surplus in the market?

-Refer to Table 7-4. If tickets sell for $40 each, then what is the total consumer surplus in the market?

(Multiple Choice)

4.8/5 (38)

Oil is used to produce gasoline. If the price of oil increases, consumer surplus in the gasoline market

(Multiple Choice)

4.9/5 (36)

Table 7-10

The following table represents the costs of five possible sellers.

Seller

Cost

Abby

$1,600

Bobby

$1,300

Dianne

$1,100

Evaline

$900

Carlos

$800

-Refer to Table 7-10. Who is a marginal seller when the price is $1,100?

(Multiple Choice)

4.8/5 (41)

Table 7-14

Seller

Cost

LeBron

$700

Kobe

$600

Kevin

$450

Steve

$400

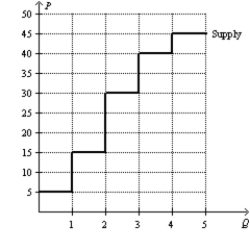

-Refer to Table 7-14. You want to hire a professional photographer to take pictures of your family. The table shows the costs of the four potential sellers in the local photography market. Which of the following graphs represents the market supply curve?

(Multiple Choice)

4.8/5 (47)

If the government removes a binding price ceiling in a market, then the producer surplus in that market will increase.

(True/False)

4.8/5 (38)

Figure 7-31  -Refer to Figure 7-31. If the market equilibrium price rises from $25 to $35, how much is the producer surplus for the producers entering the market after the price increase?

-Refer to Figure 7-31. If the market equilibrium price rises from $25 to $35, how much is the producer surplus for the producers entering the market after the price increase?

(Essay)

4.8/5 (50)

All else equal, what happens to consumer surplus if the price of a good increases?

(Multiple Choice)

4.9/5 (42)

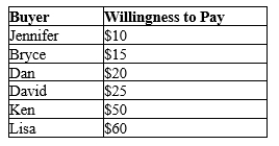

Table 7-2

This table refers to five possible buyers' willingness to pay for a case of Vanilla Coke.  -Refer to Table 7-2. If the market price is $5.50, the consumer surplus in the market will be

-Refer to Table 7-2. If the market price is $5.50, the consumer surplus in the market will be

(Multiple Choice)

5.0/5 (38)

Table 7-15

The following table represents the costs of five possible sellers.

Seller

Cost ($)

Quentin

10

Ruby

30

Sandra

60

Thomas

100

Ursula

150

-Refer to Table 7-15. Suppose each of the five sellers can supply at most one unit of the good. At which of the following prices would the market quantity supplied be exactly three units?

(Multiple Choice)

4.8/5 (40)

Figure 7-34  -Refer to Figure 7-34. Suppose there is initially a price ceiling set at $4 in this market. How much is total producer surplus with the price ceiling in place?

-Refer to Figure 7-34. Suppose there is initially a price ceiling set at $4 in this market. How much is total producer surplus with the price ceiling in place?

(Essay)

4.9/5 (39)

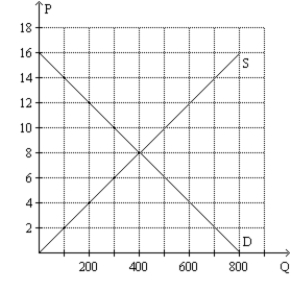

Scenario 7-2

Suppose market demand and market supply are given by the equations:  -Refer to Scenario 7-2. How much is total surplus at the equilibrium price in this market?

-Refer to Scenario 7-2. How much is total surplus at the equilibrium price in this market?

(Essay)

4.8/5 (38)

If the current allocation of resources in the market for hammers is inefficient, then it must be the case that

(Multiple Choice)

4.8/5 (37)

Suppose you buy an iPod for $100. If your consumer surplus is $30, your willingness to pay is $70.

(True/False)

4.9/5 (36)

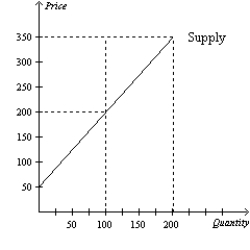

Figure 7-12  -Refer to Figure 7-12. If the equilibrium price is $350, what is the producer surplus?

-Refer to Figure 7-12. If the equilibrium price is $350, what is the producer surplus?

(Multiple Choice)

4.8/5 (34)

Table 7-16  -Refer to Table 7-16. Both the demand curve and the supply curve are straight lines. At equilibrium, consumer surplus is

-Refer to Table 7-16. Both the demand curve and the supply curve are straight lines. At equilibrium, consumer surplus is

(Multiple Choice)

4.9/5 (34)

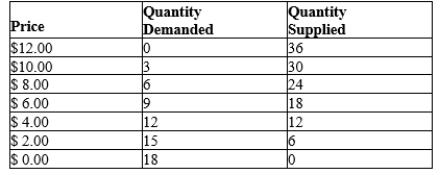

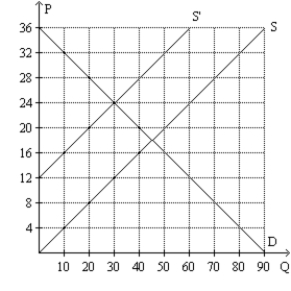

Figure 7-17  -Refer to Figure 7-17. If the supply curve is S and the demand curve is D, what is total producer surplus at the equilibrium price?

-Refer to Figure 7-17. If the supply curve is S and the demand curve is D, what is total producer surplus at the equilibrium price?

(Multiple Choice)

4.7/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)