Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics455 Questions

Exam 2: Thinking Like an Economist643 Questions

Exam 3: Interdependence and the Gains From Trade547 Questions

Exam 4: The Market Forces of Supply and Demand693 Questions

Exam 5: Elasticity and Its Application626 Questions

Exam 6: Supply, Demand, and Government Policies668 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets547 Questions

Exam 8: Applications: the Costs of Taxation509 Questions

Exam 9: Application: International Trade521 Questions

Exam 10: Externalities543 Questions

Exam 11: Public Goods and Common Resources452 Questions

Exam 12: The Design of the Tax System664 Questions

Exam 13: The Costs of Production649 Questions

Exam 14: Firms in Competitive Markets604 Questions

Exam 15: Monopoly662 Questions

Exam 16: Monopolistic Competition649 Questions

Exam 17: Oligopoly522 Questions

Exam 18: The Markets for the Factors of Production592 Questions

Exam 19: Earnings and Discrimination511 Questions

Exam 20: Income Inequality and Poverty478 Questions

Exam 21: The Theory of Consumer Choice570 Questions

Exam 22: Frontiers in Microeconomics461 Questions

Exam 23: Measuring a Nation S Income547 Questions

Exam 24: Measuring the Cost of Living565 Questions

Exam 25: Production and Growth527 Questions

Exam 26: Saving, Investment, and the Financial System637 Questions

Exam 27: Tools of Finance534 Questions

Exam 28: Unemployment and Its Natural Rate701 Questions

Exam 29: The Monetary System540 Questions

Exam 30: Money Growth and Inflation504 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts540 Questions

Exam 32: A Macroeconomic Theory of the Open Economy511 Questions

Exam 33: Aggregate Demand and Aggregate Supply572 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand523 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment536 Questions

Exam 36: Six Debates Over Macroeconomic Policy354 Questions

Select questions type

The 2005 Boston Globe article discussing ticket scalping points out that the price people will pay for tickets will rise when

(Multiple Choice)

4.9/5  (39)

(39)

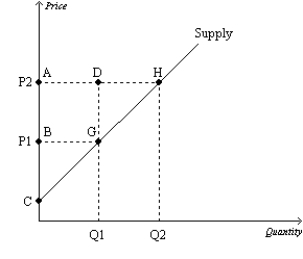

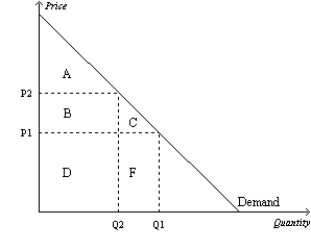

Figure 7-10  -Refer to Figure 7-10. Which area represents the increase in producer surplus when the price rises from P1 to P2?

-Refer to Figure 7-10. Which area represents the increase in producer surplus when the price rises from P1 to P2?

(Multiple Choice)

4.8/5 (34)

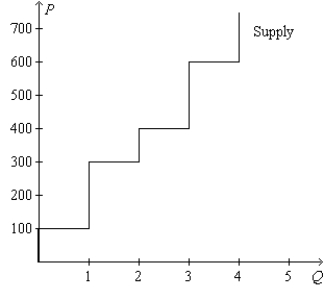

Figure 7-16  -Refer to Figure 7-16. If the price of the good is $300, then producer surplus amounts to

-Refer to Figure 7-16. If the price of the good is $300, then producer surplus amounts to

(Multiple Choice)

4.8/5 (33)

Table 7-11

The only four producers in a market have the following costs:

Seller

Cost

Evan

$50

Selena

$100

Angie

$150

Kris

$200

-Refer to Table 7-11. If the sellers bid against each other for the right to sell the good to a consumer, then the producer surplus will be

(Multiple Choice)

4.8/5 (42)

Justin builds fences for a living. Justin's out-of-pocket expenses (for wood, paint, etc.) plus the value that he places on his own time amount to his

(Multiple Choice)

4.9/5 (41)

The area below the price and above the supply curve measures the producer surplus in a market.

(True/False)

4.8/5 (36)

What happens to consumer surplus in the iPod market if iPods are normal goods and buyers of iPods experience an increase in income?

(Multiple Choice)

4.9/5 (28)

Cameron visits a sporting goods store to buy a new set of golf clubs. He is willing to pay $750 for the clubs but buys them on sale for $575. Cameron's consumer surplus from the purchase is

(Multiple Choice)

4.8/5 (40)

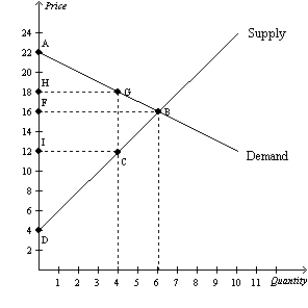

Figure 7-24  -Refer to Figure 7-24. If the government imposes a price floor at $18, then consumer surplus is

-Refer to Figure 7-24. If the government imposes a price floor at $18, then consumer surplus is

(Multiple Choice)

4.8/5 (34)

Table 7-5

For each of three potential buyers of oranges, the table displays the willingness to pay for the first three oranges of the day. Assume Allison, Bob, and Charisse are the only three buyers of oranges, and only three oranges can be supplied per day.  -Refer to Table 7-5. If the market price of an orange is $0.40, then

-Refer to Table 7-5. If the market price of an orange is $0.40, then

(Multiple Choice)

4.8/5 (28)

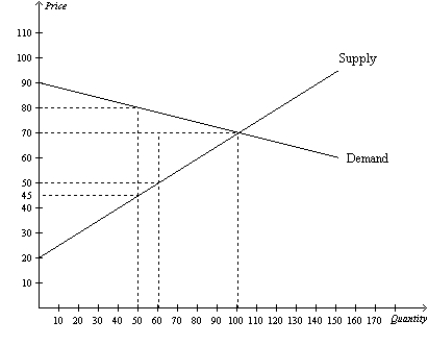

Figure 7-22  -Refer to Figure 7-22. Assume demand increases, which causes the equilibrium price to increase from $50 to $70. The increase in producer surplus would be

-Refer to Figure 7-22. Assume demand increases, which causes the equilibrium price to increase from $50 to $70. The increase in producer surplus would be

(Multiple Choice)

4.9/5 (35)

If a market is allowed to adjust freely to its equilibrium price and quantity, then an increase in demand will

(Multiple Choice)

4.7/5 (35)

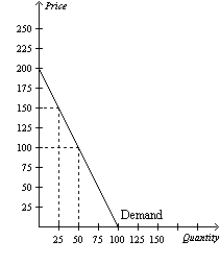

Figure 7-2  -Refer to Figure 7-2. If the price of the good is $100, then consumer surplus amounts to

-Refer to Figure 7-2. If the price of the good is $100, then consumer surplus amounts to

(Multiple Choice)

4.7/5 (46)

Figure 7-3  -Refer to Figure 7-3. When the price rises from P1 to P2, consumer surplus

-Refer to Figure 7-3. When the price rises from P1 to P2, consumer surplus

(Multiple Choice)

4.8/5 (48)

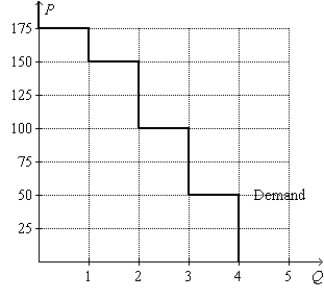

Figure 7-7  -Refer to Figure 7-7. What happens to the consumer surplus if the price rises from $100 to $150?

-Refer to Figure 7-7. What happens to the consumer surplus if the price rises from $100 to $150?

(Multiple Choice)

4.9/5 (36)

Answer each of the following questions about supply and producer surplus.

a.What is producer surplus, and how is it measured?

b.What is the relationship between the cost to sellers and the supply curve?

c.Other things equal, what happens to producer surplus when the price of a good rises? Illustrate your answer on a supply curve.

(Essay)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)