Exam 16: Expectations Theory and the Economy

Exam 1: What Economics Is About174 Questions

Exam 2: Production Possibilities Frontier Framework156 Questions

Exam 3: Supply and Demand Theory224 Questions

Exam 4: Prices Free Controlled and Relative122 Questions

Exam 5: Supply Demand and Price Applications76 Questions

Exam 6: Macroeconomic Measurements Part I Prices and Unemployment151 Questions

Exam 7: Macroeconomic Measurements Part II Gdp and Real Gdp150 Questions

Exam 8: Aggregate Demand and Aggregate Supply204 Questions

Exam 9: Classical Macroeconomics and the Self Regulating Economy172 Questions

Exam 10: Keynesian Macroeconomics and Economic Instability a Critique of the Self Regulating Economy200 Questions

Exam 11: Fiscal Policy and the Federal Budget167 Questions

Exam 12: Money Banking and the Financial System150 Questions

Exam 13: The Federal Reserve System180 Questions

Exam 14: Money and the Economy150 Questions

Exam 15: Monetary Policy185 Questions

Exam 16: Expectations Theory and the Economy150 Questions

Exam 17: Economic Growth Resources Technology Ideas and Institutions103 Questions

Exam 18: Debates in Macroeconomics Over the Role and Effects of Government100 Questions

Exam 19: Elasticity204 Questions

Exam 20: Consumer Choice and Behavioral Economics179 Questions

Exam 21: Production and Costs245 Questions

Exam 22: Perfect Competition187 Questions

Exam 23: Monopoly195 Questions

Exam 24: Monopolistic Competition Oligopoly and Game Theory172 Questions

Exam 25: Government and Product Markets Antitrust and Regulation158 Questions

Exam 26: Factor Markets With Emphasis on the Labor Market184 Questions

Exam 27: Wages Unions and Labor138 Questions

Exam 28: The Distribution of Income and Poverty99 Questions

Exam 29: Interest Rent and Profit198 Questions

Exam 30: Market Failure Externalities Public Goods and Asymmetric Information187 Questions

Exam 31: Public Choice and Special Interest Group Politics135 Questions

Exam 32: Building Theories to Explain Everyday Life From Observations to Questions to Theories to Predictions62 Questions

Exam 33: International Trade152 Questions

Exam 34: International Finance122 Questions

Exam 35: The Economic Case for and Against Government Five Topics Considered87 Questions

Exam 36: Stocks Bonds Futures and Options110 Questions

Select questions type

Milton Friedman argued that the economy is not in long-run equilibrium if the expected inflation rate __________ the actual inflation rate.

(Multiple Choice)

4.8/5  (49)

(49)

Starting from long-run equilibrium, if the public anticipates that policymakers will increase aggregate demand by less than policymakers do increase aggregate demand, and if the short-run aggregate supply curve fully adjusts to the (incorrectly) anticipated increase in aggregate demand, then Real GDP will __________ and the price level will __________.

(Multiple Choice)

4.9/5 (35)

In the real business cycle theory, business cycle contractions begin as a result of changes in

(Multiple Choice)

4.7/5 (27)

According to Milton Friedman, there are two Phillips curves, a short-run one and a long-run one.

(True/False)

4.9/5 (39)

Stagflation exists when an economy is experiencing high rates of both unemployment and inflation.

(True/False)

4.9/5 (32)

According to real business cycle theorists, changes in Real GDP are the result of initial changes in

(Multiple Choice)

4.8/5 (35)

According to the real business cycle theory, business cycle contractions are generally caused by

(Multiple Choice)

4.9/5 (35)

The original Phillips curve depicted the relationship between

(Multiple Choice)

4.8/5 (33)

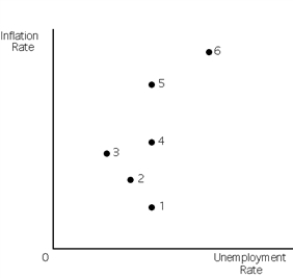

Exhibit 16-5

-Refer to Exhibit 16-5. If the economy continually moves between points 1, 2, and 3, it follows that

-Refer to Exhibit 16-5. If the economy continually moves between points 1, 2, and 3, it follows that

(Multiple Choice)

4.8/5 (27)

Real business cycle theory would emphasize the ability of a beneficial supply shock to shift the __________ curve rightward and __________ Real GDP.

(Multiple Choice)

4.9/5 (32)

If expectations are formed rationally, wages and prices are not completely flexible in the short run, and policy is correctly anticipated, increases in aggregate demand will stimulate the economy to higher levels of Real GDP and lower levels of unemployment in

(Multiple Choice)

4.8/5 (33)

Describe the sequence of events that real business cycle theorists would use to explain how an adverse supply shock would impact the economy. Use your answer to explain why it is easy to confuse cause and effect between changes originating on the supply side and those that begin on the demand side.

(Essay)

5.0/5 (39)

The original (1958) Phillips curve differed from the Samuelson-Solow Phillips curve in that

(Multiple Choice)

4.7/5 (36)

The real business cycle theory holds that the business cycle

(Multiple Choice)

4.8/5 (37)

The policy ineffectiveness proposition (PIP) argument states that under certain circumstances, neither expansionary demand-side fiscal policy nor expansionary monetary policy is effective at achieving macroeconomic goals.

(True/False)

4.9/5 (38)

New classical economists believe that monetary and fiscal policies are never effective.

(True/False)

4.8/5 (36)

Exhibit 16-1

-Refer to Exhibit 16-1. According to new classical macroeconomists, if decreases in aggregate demand are unanticipated, then the economy will move from point C to

-Refer to Exhibit 16-1. According to new classical macroeconomists, if decreases in aggregate demand are unanticipated, then the economy will move from point C to

(Multiple Choice)

4.7/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)