Exam 11: Flexible Budgeting and Analysis of Overhead Costs

Exam 1: The Changing Role of Managerial Accounting in a Dynamic Business Environment85 Questions

Exam 2: Basic Cost Management Concepts115 Questions

Exam 3: Product Costing and Cost Accumulation in a Batch Production Environment95 Questions

Exam 4: Process Costing and Hybrid Product-Costing Systems88 Questions

Exam 5: Activity-Based Costing and Management103 Questions

Exam 6: Activity Analysis, Cost Behavior, and Cost Estimation90 Questions

Exam 7: Cost-Volume-Profit Analysis109 Questions

Exam 8: Variable Costing and the Costs of Quality and Sustainability74 Questions

Exam 9: Financial Planning and Analysis: the Master Budget112 Questions

Exam 10: Standard Costing and Analysis of Direct Costs97 Questions

Exam 11: Flexible Budgeting and Analysis of Overhead Costs89 Questions

Exam 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard89 Questions

Exam 13: Investment Centers and Transfer Pricing101 Questions

Exam 14: Decision Making: Relevant Costs and Benefits96 Questions

Exam 15: Target Costing and Cost Analysis for Pricing Decisions107 Questions

Exam 16: Capital Expenditure Decisions120 Questions

Exam 17: Allocation of Support Activity Costs and Joint Costs81 Questions

Exam 18: The Sarbanes-Oxley Act, Internal Controls, and Management Accounting20 Questions

Exam 19: Compound Interest and the Concept of Present Value27 Questions

Exam 20: Inventory Management20 Questions

Select questions type

The formula flexible budget is more general than the columnar flexible budget, because the formula allows managers to compute budgeted overhead costs at any activity level.

(True/False)

4.9/5  (45)

(45)

Flexible budgets reflect a company's anticipated costs based on variations in activity levels.

(True/False)

4.9/5 (47)

Waldren Corporation applies fixed manufacturing overhead to production on the basis of machine hours worked. The following data relate to the month just ended:

Actual fixed overhead incurred: $1,245,000

Budgeted fixed overhead: $1,200,000

Anticipated machine hours: 240,000

Standard machine hours per finished unit: 8

Actual finished units completed: 31,250

Required:

A. Compute Waldren's standard fixed-overhead rate per machine hour.

B. Determine Waldren's fixed-overhead budget variance and fixed-overhead volume variance.

C. Calculate the amount of fixed overhead applied to production.

D. Consider the two events that follow and determine whether the event will affect the fixed-overhead budget variance, the fixed-overhead volume variance, both variances, or neither variance. Assume that Waldren has not yet revised its standards to reflect these events if a revision is warranted.

1. A raw material shortage halted production for two days.

2. An additional assembly-line supervisor was hired at the beginning of the month.

(Essay)

4.8/5 (36)

The manufacturing overhead applied to Work-in-Process Inventory by a company that uses standard costing would be computed as actual hours times a predetermined (standard) overhead rate.

(True/False)

4.9/5 (30)

Use the following information to answer the following Questions

Sigmo Company, which uses a standard cost system, budgeted $800,000 of fixed overhead when 50,000 machine hours were anticipated. Other data for the period were:

Actual units produced: 10,600

Actual machine hours worked: 51,800

Actual variable overhead incurred: $475,000

Actual fixed overhead incurred: $790,100

Standard variable overhead rate per machine hour: $8.50

Standard production time per unit: 5 hours

-Sigmo's variable-overhead efficiency variance is:

(Multiple Choice)

5.0/5 (39)

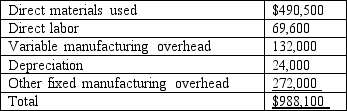

Practical Products plans to manufacture 8,000 units over the next month at the following costs: direct materials, $480,000; direct labor, $60,000; variable manufacturing overhead, $150,000; straight-line depreciation, $24,000, and other fixed manufacturing overhead, $272,000. The result is total budgeted cost of $990,000.

Shortly after the conclusion of the month, Practical Products reported the following costs:

Supervisor, Calvin Moore and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Moore was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Practical's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Moore be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

Supervisor, Calvin Moore and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Moore was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Practical's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Moore be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

(Essay)

5.0/5 (37)

The following information relates to Joplin Company for the period just ended:

All of the company's overhead is variable or fixed in nature.

Required:

A. Calculate the spending and efficiency variances for variable overhead.

B. Calculate the budget and volume variances for fixed overhead.

All of the company's overhead is variable or fixed in nature.

Required:

A. Calculate the spending and efficiency variances for variable overhead.

B. Calculate the budget and volume variances for fixed overhead.

(Essay)

4.7/5 (32)

Use the following information to answer the following Questions

Admac Technologies has a standard variable overhead rate of $4.50 per machine hour, and each unit produced has a standard time allowed of three hours. The company's static budget was based on 46,000 units. Actual results for the year follow.

Actual units produced: 42,000

Actual machine hours worked: 120,000

Actual variable overhead incurred: $520,000

-Admac's variable-overhead spending variance is:

(Multiple Choice)

4.9/5 (38)

Auditory Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 13,000

Actual fixed overhead incurred: $742,000

Standard fixed overhead rate: $15 per hour

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 48,000

If Auditory estimates four hours to manufacture a completed unit, the company's fixed-overhead budget variance would be:

(Multiple Choice)

4.9/5 (34)

Prevlar's budget for variable overhead and fixed overhead revealed the following information for an anticipated 40,000 hours of activity: variable overhead, $348,000; fixed overhead, $600,000.

The company actually worked 43,000 hours and actual overhead incurred was: variable, $365,500; fixed, $608,000.

Required:

A. Compute the company's total cost variance for variable overhead and fixed overhead if the firm uses a static budget to help assess performance.

B. Repeat part "A" assuming the use of a flexible budget.

C. Which of the two budgets (static or flexible) is preferred for performance evaluations? Why?

(Essay)

4.8/5 (31)

In an effort to reduce record-keeping, companies that sell perishable goods will often enter the standard cost of direct material, direct labor, and manufacturing overhead directly into what account?

(Multiple Choice)

4.8/5 (35)

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours would reveal total overhead costs of $210,000.

(True/False)

4.9/5 (34)

Campaign Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 12,000

Actual fixed overhead incurred: $730,000

Actual machine hours worked: 60,000

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 50,000

If Campaign estimates four hours to manufacture a completed unit, the company's standard fixed overhead rate per machine hour would be:

(Multiple Choice)

4.8/5 (37)

The sales-volume variance measures the effect on sales revenue of sales price deviations.

(True/False)

4.9/5 (36)

In a standard-costing system, the standard costs are used for product costing as well as for cost control.

(True/False)

4.9/5 (32)

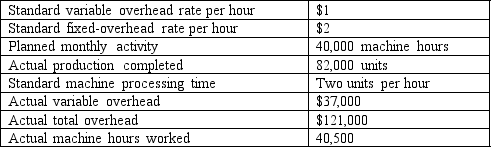

Halt Company uses a standard cost system and applies manufacturing overhead to products on the basis of machine hours. The following information is available for the year just ended:

Standard variable-overhead rate per machine hour: $2.50

Standard fixed-overhead rate per machine hour: $5.00

Planned activity during the period: 30,000 machine hours

Actual production: 10,700 finished units

Production standard: Three machine hours per unit

Actual variable overhead: $86,200

Actual total overhead: $225,500

Actual machine hours worked: 35,100

Required:

A. Calculate the budgeted fixed overhead for the year.

B. Did Halt spend more or less than anticipated for fixed overhead? How much?

C. Was variable overhead under- or overapplied during the year? By how much?

D. Was Halt efficient in its use of machine hours? Briefly explain.

E. Would the company's efficiency or inefficiency in the use of machine hours have any effect on Halt's overhead variances? If "yes," which one(s)?

(Essay)

4.8/5 (39)

Use the following information to answer the following Questions

Commerce Corporation has a high probability of operating at 40,000 activity hours during the upcoming period, and lower probabilities of operating at 30,000 hours and 50,000 hours. The company's flexible budget revealed the following:

-Commerce's flexible-budget formula, where Y is defined as total cost and AH represents activity hours, is:

-Commerce's flexible-budget formula, where Y is defined as total cost and AH represents activity hours, is:

(Multiple Choice)

4.8/5 (35)

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours would reveal total overhead costs of:

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)