Exam 11: Long-Term Liabilities: Notes, Bonds, and Leases

GAAP requires the lessee party to a capital lease

A

On January 1, 2009, Standard Incorporated is going to issue long-term debt in order to obtain money required to finance the purchase of equipment. It will have to pay a market rate of interest of 10% on this borrowed money. Standard is considering two different financial instruments in order to obtain $10,494. The first instrument being considered is a 3-year, 12%, $10,000 note with interest payable every December 31 over the life of the note. Alternatively, a 3-year, non-interest-bearing note with maturity value of $13,657 will be issued. Show how Standard's January 1, 2009 balance sheet and 2009 income statement will differ if Standard chooses to issue the non-interest-bearing note instead of the 10% note.

The present value of both financial instruments on January 1, 2009, at an 10% market rate of interest is $10,494. Because each note payable would be carried on the balance sheet at its present value, Standard's January 1, 2009, balance sheet would be unaffected by the choice of financial instruments issued. The presentation under each of the alternative liabilities at January 1, 2009 would be:

Because interest expense is the market rate of interest times the carrying value at the beginning of the year, during 2009 interest expense would also be the same. Under either financial instrument, interest expense would be .10 x $10,494 = $1,049. Net income for 2009 would be unaffected by the choice of notes.

Because interest expense is the market rate of interest times the carrying value at the beginning of the year, during 2009 interest expense would also be the same. Under either financial instrument, interest expense would be .10 x $10,494 = $1,049. Net income for 2009 would be unaffected by the choice of notes.

On January 1, 2009, Enron Corporation issued a 4-year, 7%, $9,000 bond payable. Beginning in 2010, interest is payable annually every January 1. The market rate of interest at issuance is 9%. How much are the interest payments by Enron? Why is the amount of interest expense different than the cash payments?

7% x $9,000 = $630 per year for 4 years

Interest expense is different since it is based on the market rate of interest of 9%. The investor will earn and the issuer must incur the market rate for both parties to be in agreement on the bond transactions, i.e., the investor demands to earn 9% on this bond since he can earn 9% on other investments in the market. Conversely, the issuer will not attract any investors unless it provides a return of 9% to the investors.

On September 10, 2009, Humbert Company issued bonds with a face value of $600,000 for a price of 102. During 2012, Humbert exercised a call provision and redeemed the bonds for 101. At the time of the redemption, the bonds had a balance sheet value of $607,000. The journal entry to record the redemption includes:

a. a credit to Gain on Redemption for $1,000.

b. a debit to Premium on Bonds for $7,000.

c. a credit to Discount on Bonds for $7,000.

d. a credit to Bonds Payable for $600,000.

On January 1, 2010, Foster Corporation issued a 2-year, non-interest-bearing, $4,000 note payable. Interest is payable each December 31 during the life of the note. When the note was issued, the market rate of interest was 6%. Complete the following amortization schedule:

On January 1, a 5-year, $4,000 non-interest-bearing note payable was issued for $2,600 when the market rate of interest was 9%. What is the total interest expense that will be recognized over the life of the note? Round your final answer to the nearest dollar.

On January 1, 2009, Mega Company leased equipment under a 5-year lease with payments of $7,000 on each December 31 of the lease term. The present value of the lease payments at a discount rate of 9% is $27,230. The lease is considered a capital lease.

A. Determine the amount of the leased asset and lease obligation on January 1, 2009.

B. Why are some leases accounted for as purchases by the lessee?

On January 1, 2009, Parker Company leased equipment under a 3-year lease with payments of $5,000 on each December 31 of the lease term. The present value of the lease payments at a discount rate of 12% is $12,010. If the lease is considered a capital lease, depreciation expense (straight-line) and interest expense are recognized. If the lease is considered an operating lease, then rent expense is recognized. What is the difference in the total combined net incomes of 2009, 2010, and 2011, if the lease is considered a capital lease instead of an operating lease?

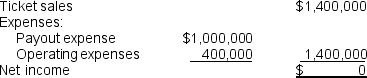

Crawford Company conducts a lottery system for Mississippi. The agreement specifies that the lottery must be conducted on a not-for-profit basis. Crawford's monthly sales of lottery tickets amounts to $1,400,000. Monthly operating expenses are $400,000, including a management charge of $30,000. The payment schedule for the guaranteed $1 million dollar payout for a winning lottery ticket is $100,000 immediately and $100,000 each year for the next 9 years. Crawford produced the following income statement as evidence of its not-for-profit status:

A. If the market rate of interest is 4%, determine the present value of the $900,000 liability arising from the monthly winning lottery ticket.

B. Recalculate the income statement to reflect GAAP measurement of payout expense.

A. If the market rate of interest is 4%, determine the present value of the $900,000 liability arising from the monthly winning lottery ticket.

B. Recalculate the income statement to reflect GAAP measurement of payout expense.

-On January 1, 2009, Foresite Corporation issued a 10-year, 9%, $100,000 installment note payable. The payment on this note is $15,582 and is paid annually at year-end beginning December 31, 2009. How much total interest is paid over the loan period?

-On January 1, 2009, Foresite Corporation issued a 10-year, 9%, $100,000 installment note payable. The payment on this note is $15,582 and is paid annually at year-end beginning December 31, 2009. How much total interest is paid over the loan period?

If interest expense is less than the contractual interest payment, then

Burns Company issued $1,000,000 of 9 percent, ten-year bonds for $937,790 on July 1, 2010, when the market rate of interest was 10 percent. The bonds mature in ten years and pay interest on June 30 and December 31. Burn's fiscal year ends on December 31 and the company uses the effective interest method of amortization. The journal entry on December 31, 2010 will include:

If interest expense is greater than the contractual interest payment, then

On January 1, a 3-year, $1,090 non-interest-bearing note payable was issued for $942 when the market rate of interest was 5%. How much interest expense will Hamlen recognize in each of the first two years using the effective interest method? Round to the nearest dollar.

Which type of note consists of periodic payments covering both interest and principal?

What is the risk premium of a bond issue and what role does it play in the determination of bond prices?

On January 1, 2009, Alcon Corporation issued a 5-year, 10%, $10,000 bond payable. Beginning in 2010, interest is payable every January 1 over the life of the bond. The market rate of interest on the issue date is 10%. Calculate the interest expense for 2009 using the effective interest method.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)