Exam 24: Portfolio Theory, Asset Pricing Models, and Behavioral Finance

Exam 1: An Overview of Financial Management and the Financial Environment38 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes3 Questions

Exam 3: Analysis of Financial Statements104 Questions

Exam 4: Time Value of Money139 Questions

Exam 5: Bonds, Bond Valuation, and Interest Rates100 Questions

Exam 6: Risks and Rates of Return132 Questions

Exam 7: Stocks and Their Valuation48 Questions

Exam 8: Financial Options and Applications in Corporate Finance22 Questions

Exam 9: The Cost of Capital87 Questions

Exam 10: The Basics of Capital Budgeting98 Questions

Exam 11: Cash Flow Estimation and Risk Analysis66 Questions

Exam 12: Financial Planning and Forecasting Financial Statements46 Questions

Exam 13: Corporate Valuation, Value-Based Management, and Corporate Governance24 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases26 Questions

Exam 15: Capital Structure Decisions70 Questions

Exam 16: Working Capital Management129 Questions

Exam 17: Multinational Financial Management39 Questions

Exam 18: Lease Financing20 Questions

Exam 19: Hybrid Financing: Preferred Stock, Warrants, and Convertibles27 Questions

Exam 20: Initial Public Offerings, Investment Banking, and Financial Restructuring22 Questions

Exam 21: Mergers, Lbos, Divestitures, and Holding Companies41 Questions

Exam 22: Bankruptcy, Reorganization, and Liquidation8 Questions

Exam 23: Derivatives and Risk Management14 Questions

Exam 24: Portfolio Theory, Asset Pricing Models, and Behavioral Finance25 Questions

Exam 25: Real Options15 Questions

Exam 26: Analysis of Capital Structure Theory27 Questions

Exam 27: Providing and Obtaining Credit31 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control20 Questions

Exam 29: Pension Plan Management9 Questions

Exam 30: Financial Management in Not-For-Profit Businesses10 Questions

Select questions type

We will almost always find that the beta of a diversified portfolio is less stable over time than the beta of a single security.

Free

(True/False)

4.8/5  (27)

(27)

Correct Answer: Verified

Verified

False

Which of the following is NOT a potential problem with beta and its estimation?

Free

(Multiple Choice)

4.8/5 (33)

Correct Answer:Verified

C

Stock A's beta is 1.5 and Stock B's beta is 0.5. Which of the following statements must be true about these securities? (Assume market equilibrium.)

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

D

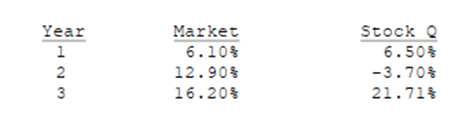

You are given the following returns on "the market" and Stock Q during the last three years. We could calculate beta using data for Years 1 and 2 and then, after Year 3, calculate a new beta for Years 2 and 3. How different are those two betas, i.e., what's the value of beta 2 - beta 1? (Hint: You can find betas using the Rise-Over-Run method, or using your calculator's regression function.)

(Multiple Choice)

4.8/5 (37)

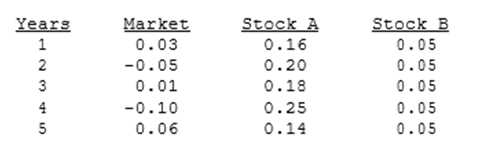

You have the following data on (1) the average annual returns of the market for the past 5 years and (2) similar information on Stocks A and B. Which of the possible answers best describes the historical betas for A and B?

(Multiple Choice)

4.8/5 (30)

If you plotted the returns of Selleck & Company against those of the market and found that the slope of your line was negative, the CAPM would indicate that the required rate of return on Selleck's stock should be less than the risk-free rate for a well-diversified investor, assuming that the observed relationship is expected to continue in the future.

(True/False)

4.9/5 (40)

If the returns of two firms are negatively correlated, then one of them must have a negative beta.

(True/False)

4.9/5 (38)

Arbitrage pricing theory is based on the premise that more than one factor affects stock returns, and the factors are specified to be (1) market returns, (2) dividend yields, and (3) changes in inflation.

(True/False)

4.8/5 (31)

In portfolio analysis, we often use ex post (historical) returns and standard deviations, despite the fact that we are interested in ex ante (future) data.

(True/False)

4.9/5 (36)

The Y-axis intercept of the SML indicates the return on an individual asset when the realized return on an average (b = 1) stock is zero.

(True/False)

4.8/5 (30)

The SML relates required returns to firms' systematic (or market) risk. The slope and intercept of this line can be influenced by managerial actions.

(True/False)

4.8/5 (31)

If investors are risk averse and hold only one stock, we can conclude that the required rate of return on a stock whose standard deviation is

0.21 will be greater than the required return on a stock whose standard deviation is 0.10. However, if stocks are held in portfolios, it is possible that the required return could be higher on the low standard deviation stock.

(True/False)

4.7/5 (32)

It is possible for a firm to have a positive beta, even if the correlation between its returns and those of another firm are negative.

(True/False)

4.8/5 (31)

You hold a diversified portfolio consisting of a $5,000 investment in each of 20 different common stocks. The portfolio beta is equal to

1.12. You have decided to sell a lead mining stock (b = 1.00) at

$5,000 net and use the proceeds to buy a like amount of a steel company stock (b = 2.00). What is the new beta of the portfolio?

(Multiple Choice)

4.8/5 (31)

The CAPM is a multi-period model which takes account of differences in securities' maturities, and it can be used to determine the required rate of return for any given level of systematic risk.

(True/False)

4.8/5 (34)

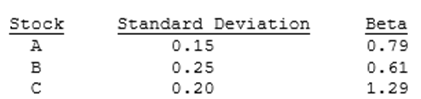

You have the following data on three stocks:  As a risk minimizer, you would choose Stock______ if it is to be held in isolation and Stock_________ if it is to be held as part of a well- diversified portfolio.

As a risk minimizer, you would choose Stock______ if it is to be held in isolation and Stock_________ if it is to be held as part of a well- diversified portfolio.

(Multiple Choice)

4.8/5 (39)

A stock with a beta equal to -1.0 has zero systematic (or market) risk.

(True/False)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)