Exam 10: Standard Costs and Variances

Exam 1: Managerial Accounting and Cost Concepts346 Questions

Exam 2: Job-Order Costing: Calculating Unit Product Costs408 Questions

Exam 3: Job-Order Costing: Cost Flows and External Reporting314 Questions

Exam 4: Process Costing365 Questions

Exam 5: Cost-Volume-Profit Relationships396 Questions

Exam 6: Variable Costing and Segment Reporting: Tools for Management392 Questions

Exam 7: Activity-Based Costing: a Tool to Aid Decision Making382 Questions

Exam 8: Master Budgeting284 Questions

Exam 9: Flexible Budgets and Performance Analysis491 Questions

Exam 10: Standard Costs and Variances469 Questions

Exam 11: Responsibility Accounting Systems335 Questions

Exam 12: Strategic Performance Measurement153 Questions

Exam 13: Differential Analysis: the Key to Decision Making432 Questions

Exam 14: Capital Budgeting Decisions405 Questions

Exam 15: Statement of Cash Flows221 Questions

Exam 16: Financial Statement Analysis327 Questions

Select questions type

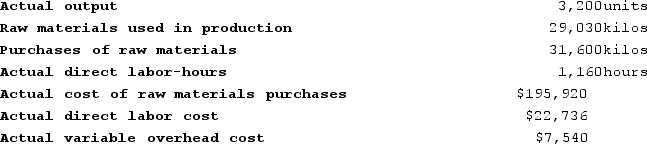

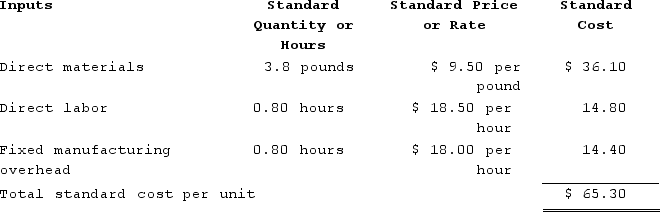

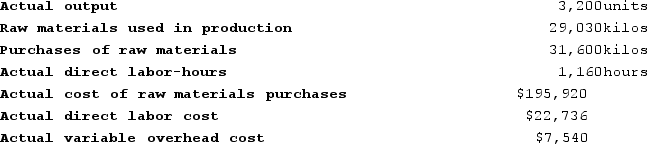

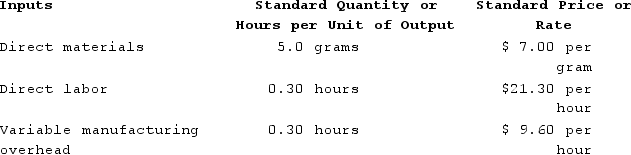

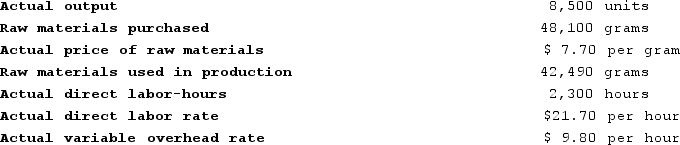

Handerson Corporation makes a product with the following standard costs:  The company reported the following results concerning this product in August.

The company reported the following results concerning this product in August.

The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead rate variance for August is:

The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead rate variance for August is:

(Multiple Choice)

4.8/5  (40)

(40)

The variable overhead efficiency variance does not actually measure how efficiently variable manufacturing overhead resources were used.

(True/False)

5.0/5 (34)

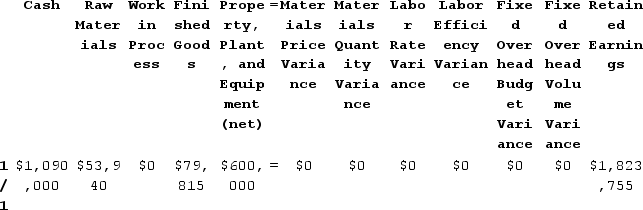

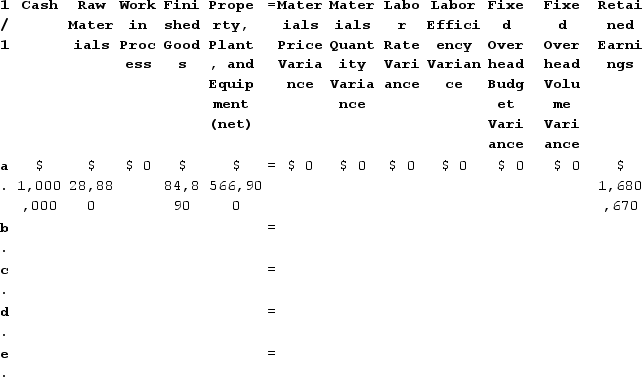

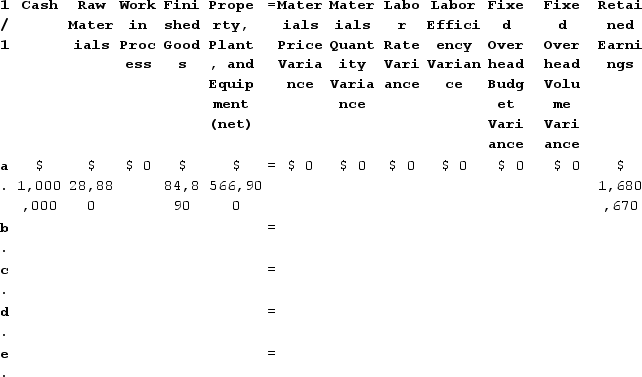

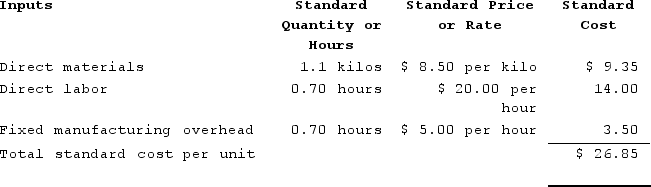

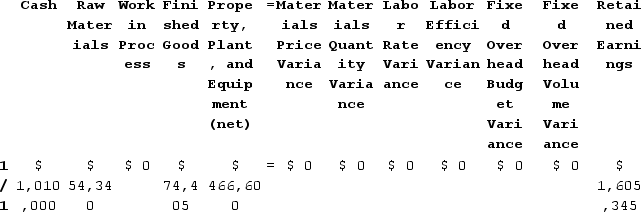

Colbeck Corporation uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. The standard cost card for the company's only product is as follows:  During the year, the company purchased 68,000 gallons of raw material at a price of $5.40 per gallon and used 62,660 gallons of the raw material to produce 18,400 units of work in process.Assume that all transactions are recorded on a worksheet as shown in the text. On the left-hand side of the equals sign in the worksheet are columns for Cash, Raw Materials, Work in Process, Finished Goods, and Property, Plant, and Equipment (net). All of the variance columns are on the right-hand-side of the equals sign along with the column for Retained Earnings.When recording the raw materials used in production, the Raw Materials inventory account will increase (decrease) by:

During the year, the company purchased 68,000 gallons of raw material at a price of $5.40 per gallon and used 62,660 gallons of the raw material to produce 18,400 units of work in process.Assume that all transactions are recorded on a worksheet as shown in the text. On the left-hand side of the equals sign in the worksheet are columns for Cash, Raw Materials, Work in Process, Finished Goods, and Property, Plant, and Equipment (net). All of the variance columns are on the right-hand-side of the equals sign along with the column for Retained Earnings.When recording the raw materials used in production, the Raw Materials inventory account will increase (decrease) by:

(Multiple Choice)

5.0/5 (27)

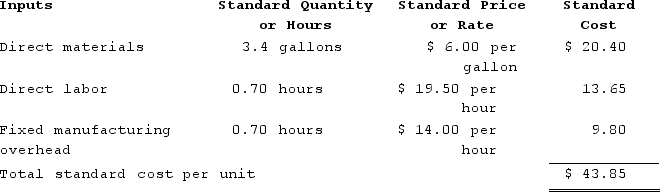

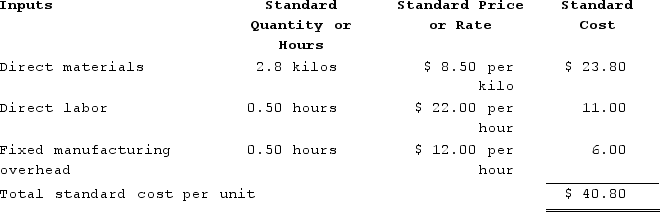

Freiling Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  During the year, the company assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 14,890 hours at an average cost of $22.80 per hour.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

During the year, the company assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 14,890 hours at an average cost of $22.80 per hour.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When recording the direct labor costs, the Cash account will increase (decrease) by:

When recording the direct labor costs, the Cash account will increase (decrease) by:

(Multiple Choice)

4.8/5 (51)

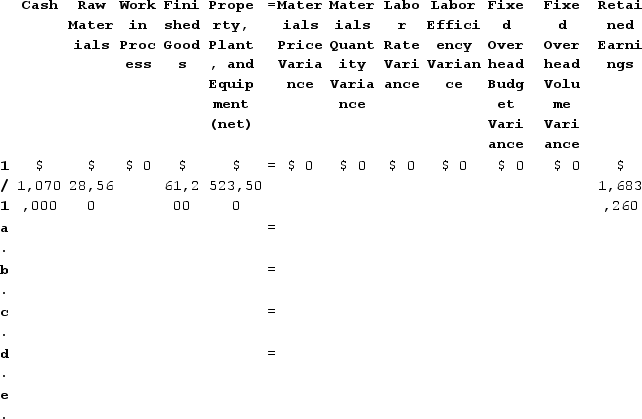

Robins Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $360,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 134,700 pounds of raw material at a price of $9.10 per pound.Used 122,080 pounds of the raw material to produce 32,100 units of work in process.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,680 hours at an average cost of $17.20 per hour.Applied fixed overhead to the 32,100 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $378,400. Of this total, $297,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $81,000 related to depreciation of manufacturing equipment.Completed and transferred 32,100 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $360,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 134,700 pounds of raw material at a price of $9.10 per pound.Used 122,080 pounds of the raw material to produce 32,100 units of work in process.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,680 hours at an average cost of $17.20 per hour.Applied fixed overhead to the 32,100 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $378,400. Of this total, $297,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $81,000 related to depreciation of manufacturing equipment.Completed and transferred 32,100 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When the work in process is completed and transferred to finished goods in transaction (e) above, the Finished Goods inventory account will increase (decrease) by:

When the work in process is completed and transferred to finished goods in transaction (e) above, the Finished Goods inventory account will increase (decrease) by:

(Multiple Choice)

4.7/5 (39)

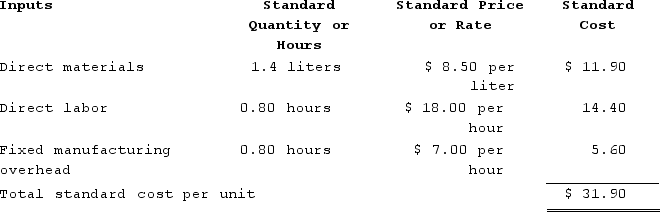

Samples Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $140,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 49,500 liters of raw material at a price of $8.00 per liter. The materials price variance was $24,750 Favorable.Used 45,820 liters of the raw material to produce 32,800 units of work in process. The materials quantity variance was $850 Favorable.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 28,440 hours at an average cost of $17.00 per hour. The direct labor rate variance was $28,440 Favorable. The labor efficiency variance was $39,600 Unfavorable.Applied fixed overhead to the 32,800 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $154,700. Of this total, $83,700 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $71,000 related to depreciation of manufacturing equipment. The fixed manufacturing overhead budget variance was $14,700 Unfavorable. The fixed manufacturing overhead volume variance was $43,680 Favorable.Completed and transferred 32,800 units from work in process to finished goods.Sold (for cash) 32,000 units to customers at a price of $38.20 per unit.Transferred the standard cost associated with the 32,000 units sold from finished goods to cost of goods sold.Paid $133,000 of selling and administrative expenses.Closed all standard cost variances to cost of goods sold.To answer the following questions, it would be advisable to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $140,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 49,500 liters of raw material at a price of $8.00 per liter. The materials price variance was $24,750 Favorable.Used 45,820 liters of the raw material to produce 32,800 units of work in process. The materials quantity variance was $850 Favorable.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 28,440 hours at an average cost of $17.00 per hour. The direct labor rate variance was $28,440 Favorable. The labor efficiency variance was $39,600 Unfavorable.Applied fixed overhead to the 32,800 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $154,700. Of this total, $83,700 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $71,000 related to depreciation of manufacturing equipment. The fixed manufacturing overhead budget variance was $14,700 Unfavorable. The fixed manufacturing overhead volume variance was $43,680 Favorable.Completed and transferred 32,800 units from work in process to finished goods.Sold (for cash) 32,000 units to customers at a price of $38.20 per unit.Transferred the standard cost associated with the 32,000 units sold from finished goods to cost of goods sold.Paid $133,000 of selling and administrative expenses.Closed all standard cost variances to cost of goods sold.To answer the following questions, it would be advisable to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When the company closes its standard cost variances, the Cost of Goods Sold will increase (decrease) by:

When the company closes its standard cost variances, the Cost of Goods Sold will increase (decrease) by:

(Multiple Choice)

4.8/5 (40)

Robins Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $360,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 134,700 pounds of raw material at a price of $9.10 per pound.Used 122,080 pounds of the raw material to produce 32,100 units of work in process.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,680 hours at an average cost of $17.20 per hour.Applied fixed overhead to the 32,100 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $378,400. Of this total, $297,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $81,000 related to depreciation of manufacturing equipment.Completed and transferred 32,100 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $360,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 134,700 pounds of raw material at a price of $9.10 per pound.Used 122,080 pounds of the raw material to produce 32,100 units of work in process.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,680 hours at an average cost of $17.20 per hour.Applied fixed overhead to the 32,100 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $378,400. Of this total, $297,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $81,000 related to depreciation of manufacturing equipment.Completed and transferred 32,100 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When recording the raw materials used in production in transaction (b) above, the Work in Process inventory account will increase (decrease) by:

When recording the raw materials used in production in transaction (b) above, the Work in Process inventory account will increase (decrease) by:

(Multiple Choice)

4.8/5 (32)

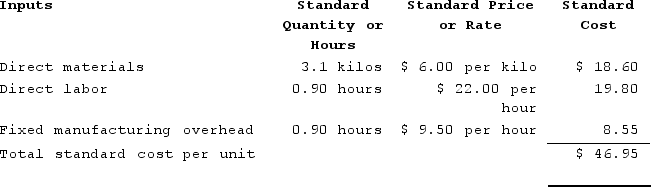

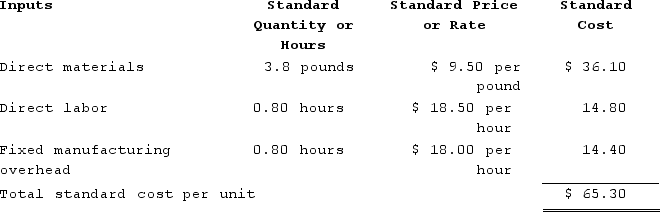

Phann Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $90,000 and budgeted activity of 7,500 hours.During the year, the company completed the following transactions:a. Purchased 59,000 kilos of raw material at a price of $9.20 per kilo.b. Used 51,340 kilos of the raw material to produce 18,300 units of work in process.c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 8,850 hours at an average cost of $23.70 per hour.d. Applied fixed overhead to the 18,300 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $79,400. Of this total, $22,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $57,000 related to depreciation of manufacturing equipment.e. Completed and transferred 18,300 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $90,000 and budgeted activity of 7,500 hours.During the year, the company completed the following transactions:a. Purchased 59,000 kilos of raw material at a price of $9.20 per kilo.b. Used 51,340 kilos of the raw material to produce 18,300 units of work in process.c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 8,850 hours at an average cost of $23.70 per hour.d. Applied fixed overhead to the 18,300 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $79,400. Of this total, $22,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $57,000 related to depreciation of manufacturing equipment.e. Completed and transferred 18,300 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When recording the direct labor costs in transaction (c) above, the Cash account will increase (decrease) by:

When recording the direct labor costs in transaction (c) above, the Cash account will increase (decrease) by:

(Multiple Choice)

4.9/5 (33)

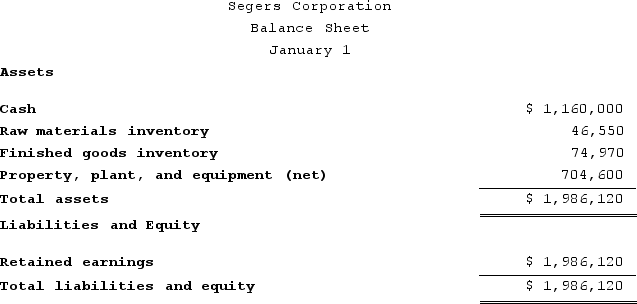

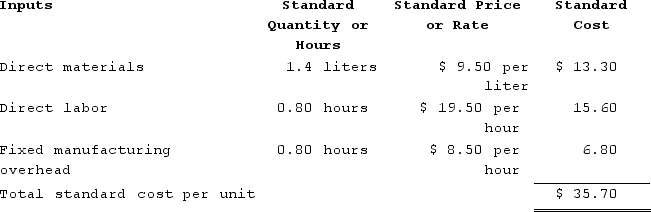

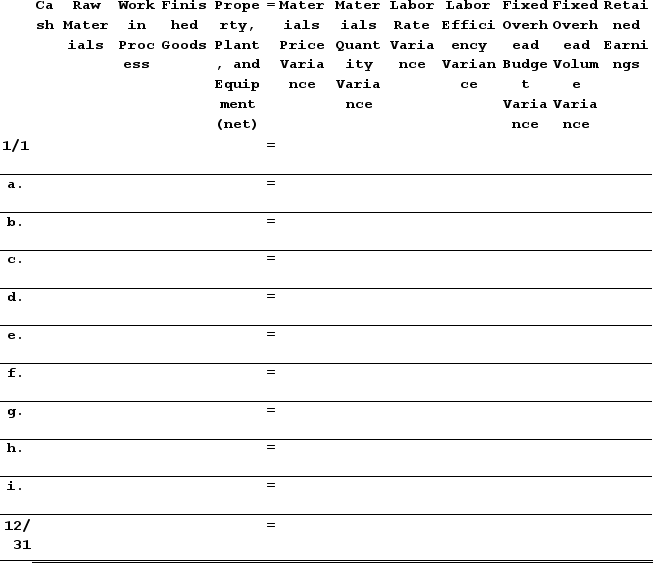

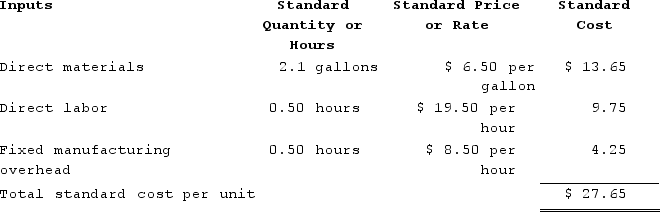

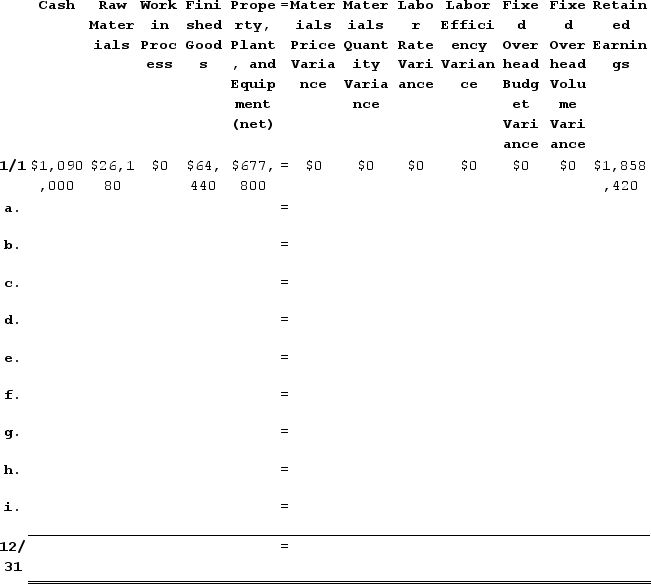

Segers Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The company's balance sheet at the beginning of the year was as follows:

The standard cost card for the company's only product is as follows:

The standard cost card for the company's only product is as follows:

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $238,000 and budgeted activity of 28,000 hours.

During the year, the company completed the following transactions:a. Purchased 51,000 liters of raw material at a price of $9.20 per liter.b. Used 46,100 liters of the raw material to produce 33,000 units of work in process.c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,200 hours at an average cost of $19.90 per hour.d. Applied fixed overhead to the 33,000 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $251,800. Of this total, $165,800 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $86,000 related to depreciation of manufacturing equipment.e. Transferred 33,000 units from work in process to finished goods.f. Sold for cash 34,800 units to customers at a price of $44.00 per unit.g. Completed and transferred the standard cost associated with the 34,800 units sold from finished goods to cost of goods sold.h. Paid $156,000 of selling and administrative expenses.i. Closed all standard cost variances to cost of goods sold.

Required:1. Compute all direct materials, direct labor, and fixed overhead variances for the year.2. Enter the beginning balances and record the above transactions in the worksheet that appears below.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $238,000 and budgeted activity of 28,000 hours.

During the year, the company completed the following transactions:a. Purchased 51,000 liters of raw material at a price of $9.20 per liter.b. Used 46,100 liters of the raw material to produce 33,000 units of work in process.c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,200 hours at an average cost of $19.90 per hour.d. Applied fixed overhead to the 33,000 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $251,800. Of this total, $165,800 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $86,000 related to depreciation of manufacturing equipment.e. Transferred 33,000 units from work in process to finished goods.f. Sold for cash 34,800 units to customers at a price of $44.00 per unit.g. Completed and transferred the standard cost associated with the 34,800 units sold from finished goods to cost of goods sold.h. Paid $156,000 of selling and administrative expenses.i. Closed all standard cost variances to cost of goods sold.

Required:1. Compute all direct materials, direct labor, and fixed overhead variances for the year.2. Enter the beginning balances and record the above transactions in the worksheet that appears below.

3. Determine the ending balance (e.g., 12/31 balance) in each account.

3. Determine the ending balance (e.g., 12/31 balance) in each account.

(Essay)

4.8/5 (40)

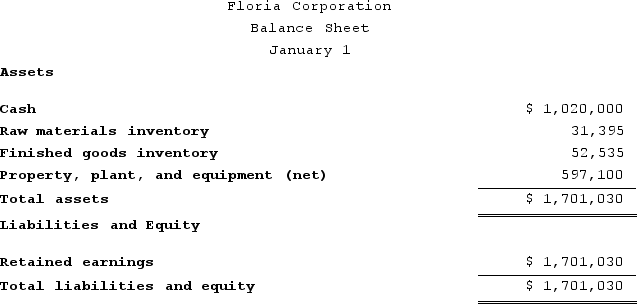

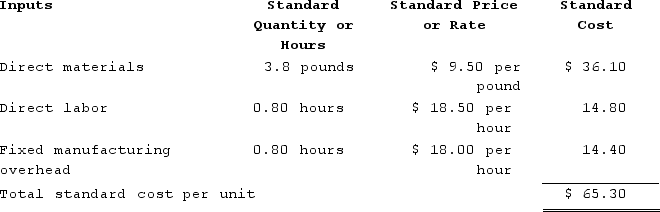

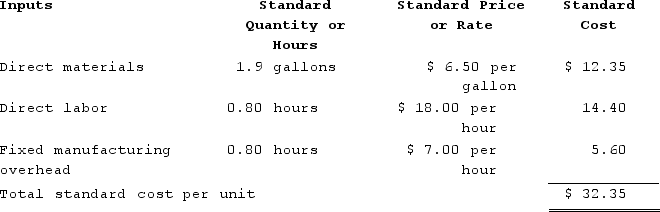

Floria Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The company's balance sheet at the beginning of the year was as follows:

The standard cost card for the company's only product is as follows:

The standard cost card for the company's only product is as follows:

The company calculated the following variances for the year:

The company calculated the following variances for the year:

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $148,750 and budgeted activity of 17,500 hours.

During the year, the company completed the following transactions:

a. Purchased 68,500 gallons of raw material at a price of $5.60 per gallon.b. Used 64,990 gallons of the raw material to produce 30,900 units of work in process.c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 14,550 hours at an average cost of $19.00 per hour.d. Applied fixed overhead to the 30,900 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $160,350. Of this total, $78,350 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $82,000 related to depreciation of manufacturing equipment.e. Transferred 30,900 units from work in process to finished goods.f. Sold for cash 27,200 units to customers at a price of $33.50 per unit.g. Completed and transferred the standard cost associated with the 27,200 units sold from finished goods to cost of goods sold.h. Paid $79,000 of selling and administrative expenses.i. Closed all standard cost variances to cost of goods sold.

Required:1. Enter the beginning balances and record the above transactions in the worksheet that appears below.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $148,750 and budgeted activity of 17,500 hours.

During the year, the company completed the following transactions:

a. Purchased 68,500 gallons of raw material at a price of $5.60 per gallon.b. Used 64,990 gallons of the raw material to produce 30,900 units of work in process.c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 14,550 hours at an average cost of $19.00 per hour.d. Applied fixed overhead to the 30,900 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $160,350. Of this total, $78,350 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $82,000 related to depreciation of manufacturing equipment.e. Transferred 30,900 units from work in process to finished goods.f. Sold for cash 27,200 units to customers at a price of $33.50 per unit.g. Completed and transferred the standard cost associated with the 27,200 units sold from finished goods to cost of goods sold.h. Paid $79,000 of selling and administrative expenses.i. Closed all standard cost variances to cost of goods sold.

Required:1. Enter the beginning balances and record the above transactions in the worksheet that appears below.

2.Determine the ending balance (e.g., 12/31 balance) in each account.

2.Determine the ending balance (e.g., 12/31 balance) in each account.

(Essay)

4.8/5 (42)

The following labor standards have been established for a particular product:

The following data pertain to operations concerning the product for the last month:

The following data pertain to operations concerning the product for the last month:

Required:a. What is the labor rate variance for the month?b. What is the labor efficiency variance for the month?

Required:a. What is the labor rate variance for the month?b. What is the labor efficiency variance for the month?

(Essay)

4.7/5 (24)

Robins Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $360,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 134,700 pounds of raw material at a price of $9.10 per pound.Used 122,080 pounds of the raw material to produce 32,100 units of work in process.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,680 hours at an average cost of $17.20 per hour.Applied fixed overhead to the 32,100 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $378,400. Of this total, $297,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $81,000 related to depreciation of manufacturing equipment.Completed and transferred 32,100 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $360,000 and budgeted activity of 20,000 hours.During the year, the company completed the following transactions:Purchased 134,700 pounds of raw material at a price of $9.10 per pound.Used 122,080 pounds of the raw material to produce 32,100 units of work in process.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 26,680 hours at an average cost of $17.20 per hour.Applied fixed overhead to the 32,100 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $378,400. Of this total, $297,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $81,000 related to depreciation of manufacturing equipment.Completed and transferred 32,100 units from work in process to finished goods.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When recording the direct labor costs in transaction (c) above, the Work in Process inventory account will increase (decrease) by:

When recording the direct labor costs in transaction (c) above, the Work in Process inventory account will increase (decrease) by:

(Multiple Choice)

4.9/5 (35)

Handerson Corporation makes a product with the following standard costs:  The company reported the following results concerning this product in August.

The company reported the following results concerning this product in August.

The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead efficiency variance for August is:

The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead efficiency variance for August is:

(Multiple Choice)

4.8/5 (40)

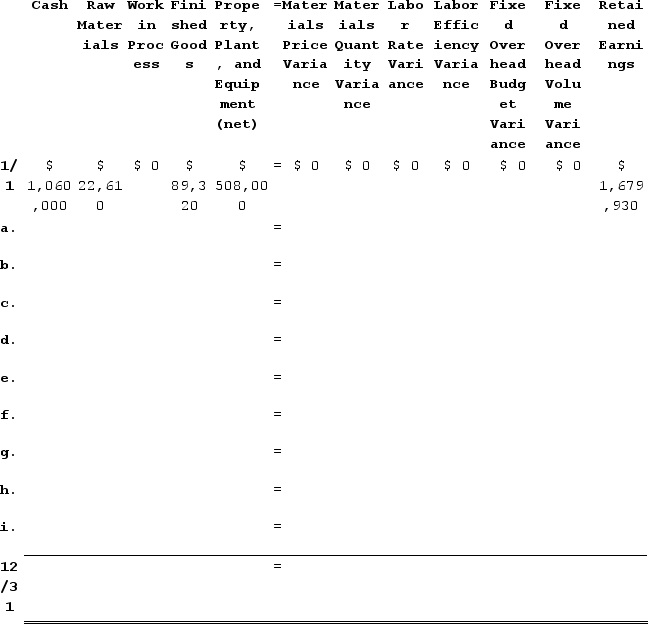

Alvino Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead.The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $70,000 and budgeted activity of 14,000 hours.During the year, the company completed the following transactions:Purchased 32,200 kilos of raw material at a price of $7.80 per kilo. The materials price variance was $22,540 Favorable.Used 30,480 kilos of the raw material to produce 27,800 units of work in process. The materials quantity variance was $850 Favorable.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 18,260 hours at an average cost of $20.50 per hour. The direct labor rate variance was $9,130 Unfavorable. The labor efficiency variance was $24,000 Favorable.Applied fixed overhead to the 27,800 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor−hours allowed. Actual fixed overhead costs for the year were $59,500. Of this total, $22,500 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $82,000 related to depreciation of manufacturing equipment. The fixed manufacturing overhead budget variance was $10,500 Favorable. The fixed manufacturing overhead volume variance was $27,300 Favorable.Completed and transferred 27,800 units from work in process to finished goods.Sold (for cash) 29,000 units to customers at a price of $31.90 per unit.Transferred the standard cost associated with the 29,000 units sold from finished goods to cost of goods sold.Paid $101,000 of selling and administrative expenses.Closed all standard cost variances to cost of goods sold.To answer the following questions, you will need to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $70,000 and budgeted activity of 14,000 hours.During the year, the company completed the following transactions:Purchased 32,200 kilos of raw material at a price of $7.80 per kilo. The materials price variance was $22,540 Favorable.Used 30,480 kilos of the raw material to produce 27,800 units of work in process. The materials quantity variance was $850 Favorable.Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 18,260 hours at an average cost of $20.50 per hour. The direct labor rate variance was $9,130 Unfavorable. The labor efficiency variance was $24,000 Favorable.Applied fixed overhead to the 27,800 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor−hours allowed. Actual fixed overhead costs for the year were $59,500. Of this total, $22,500 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $82,000 related to depreciation of manufacturing equipment. The fixed manufacturing overhead budget variance was $10,500 Favorable. The fixed manufacturing overhead volume variance was $27,300 Favorable.Completed and transferred 27,800 units from work in process to finished goods.Sold (for cash) 29,000 units to customers at a price of $31.90 per unit.Transferred the standard cost associated with the 29,000 units sold from finished goods to cost of goods sold.Paid $101,000 of selling and administrative expenses.Closed all standard cost variances to cost of goods sold.To answer the following questions, you will need to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The ending balance in the Property, Plant, and Equipment (net) account will be closest to:

The ending balance in the Property, Plant, and Equipment (net) account will be closest to:

(Multiple Choice)

4.8/5 (29)

Valera Corporation makes a product with the following standards for labor and variable overhead:  The company budgeted for production of 5,300 units in July, but actual production was 5,400 units. The company used 2,130 direct labor-hours to produce this output. The actual variable overhead rate was $6.10 per hour. The company applies variable overhead on the basis of direct labor-hours.The variable overhead efficiency variance for July is:

The company budgeted for production of 5,300 units in July, but actual production was 5,400 units. The company used 2,130 direct labor-hours to produce this output. The actual variable overhead rate was $6.10 per hour. The company applies variable overhead on the basis of direct labor-hours.The variable overhead efficiency variance for July is:

(Multiple Choice)

4.8/5 (34)

Juhasz Corporation makes a product with the following standards for direct labor and variable overhead:  In August the company produced 8,000 units using 4,190 direct labor-hours. The actual variable overhead cost was $15,922. The company applies variable overhead on the basis of direct labor-hours.The variable overhead efficiency variance for August is:

In August the company produced 8,000 units using 4,190 direct labor-hours. The actual variable overhead cost was $15,922. The company applies variable overhead on the basis of direct labor-hours.The variable overhead efficiency variance for August is:

(Multiple Choice)

4.9/5 (42)

Krizun Industries makes heavy construction equipment. The standard for a particular crane calls for 20 direct labor-hours at $24 per direct labor-hour. During a recent period 875 cranes were made. The labor efficiency variance was $1,200 Unfavorable. How many actual direct labor-hours were worked?

(Multiple Choice)

4.8/5 (40)

Ester Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:  The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $168,000 and budgeted activity of 24,000 hours.During the year, the company applied fixed overhead to the 22,600 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $149,800. Of this total, $83,800 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $66,000 related to depreciation of manufacturing equipment.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $168,000 and budgeted activity of 24,000 hours.During the year, the company applied fixed overhead to the 22,600 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $149,800. Of this total, $83,800 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $66,000 related to depreciation of manufacturing equipment.Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

When applying fixed manufacturing overhead to production, the Work in Process inventory account will increase (decrease) by:

When applying fixed manufacturing overhead to production, the Work in Process inventory account will increase (decrease) by:

(Multiple Choice)

4.9/5 (38)

The standards for product G78V specify 4.1 direct labor-hours per unit at $12.10 per direct labor-hour. Last month 1,600 units of product G78V were produced using 6,600 direct labor-hours at a total direct labor wage cost of $77,220.Required:a. What was the labor rate variance for the month?b. What was the labor efficiency variance for the month?

(Essay)

4.8/5 (35)

Pippin Incorporated has provided the following data concerning one of the products in its standard cost system. Variable manufacturing overhead is applied to products on the basis of direct labor-hours.  The company has reported the following actual results for the product for June:

The company has reported the following actual results for the product for June:

The variable overhead rate variance for the month is closest to:

The variable overhead rate variance for the month is closest to:

(Multiple Choice)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)