Exam 4: Supply and Demand: An Initial Look

Exam 1: What Is Economics?227 Questions

Exam 2: The Economy: Myth and Reality150 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice250 Questions

Exam 4: Supply and Demand: An Initial Look308 Questions

Exam 5: Consumer Choice: Individual and Market Demand202 Questions

Exam 6: Demand and Elasticity209 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis216 Questions

Exam 8: Output, Price, and Profit: The Importance of Marginal Analysis189 Questions

Exam 9: Securities: Business Finance, and the Economy: The Tail that Wags the Dog?198 Questions

Exam 10: The Firm and the Industry under Perfect Competition208 Questions

Exam 11: Monopoly203 Questions

Exam 12: Between Competition and Monopoly225 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust152 Questions

Exam 14: The Case for Free Markets I: The Price System220 Questions

Exam 15: The Shortcomings of Free Markets212 Questions

Exam 16: The Market's Prime Achievement: Innovation and Growth110 Questions

Exam 17: Externalities, the Environment, and Natural Resources217 Questions

Exam 18: Taxation and Resource Allocation219 Questions

Exam 19: Pricing the Factors of Production228 Questions

Exam 20: Labor and Entrepreneurship: The Human Inputs223 Questions

Exam 21: Poverty, Inequality, and Discrimination167 Questions

Exam 22: An Introduction to Macroeconomics211 Questions

Exam 23: The Goals of Macroeconomic Policy207 Questions

Exam 24: Economic Growth: Theory and Policy223 Questions

Exam 25: Aggregate Demand and the Powerful Consumer214 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation?210 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation?223 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy205 Questions

Exam 29: Money and the Banking System219 Questions

Exam 30: Monetary Policy: Conventional and Unconventional205 Questions

Exam 31: The Financial Crisis and the Great Recession61 Questions

Exam 32: The Debate over Monetary and Fiscal Policy214 Questions

Exam 33: Budget Deficits in the Short and Long Run210 Questions

Exam 34: The Trade-Off between Inflation and Unemployment214 Questions

Exam 35: International Trade and Comparative Advantage226 Questions

Exam 36: The International Monetary System: Order or Disorder?213 Questions

Exam 37: Exchange Rates and the Macroeconomy214 Questions

Select questions type

Price controls usually enhance efficiency in the allocation of resources.

(True/False)

4.9/5  (41)

(41)

In early 1996, Congress proposed an agriculture bill that would gradually reduce price supports for many agricultural products.If the bill were to be approved, what would most likely happen to the number of families employed in agriculture?

(Multiple Choice)

4.9/5 (43)

The ____ the demand curve for a good, the ____ the change in equilibrium quantity after a shift of the supply curve.

(Multiple Choice)

4.8/5 (36)

Define equilibrium as it relates to markets.Describe the process by which a market reaches a new equilibrium.Include an appropriate diagram.

(Essay)

4.8/5 (39)

A price ceiling is only effective if it is above the market equilibrium.

(True/False)

4.9/5 (35)

Studies at Cornell University revealed that chickens grow 2 percent larger when a red mitten is placed in their cage and Vivaldi is played in the coop.Resultant feed savings are estimated at $60 million a year.In the chicken market, the

(Multiple Choice)

4.8/5 (37)

Suppose demand can be described with the equation Q = 900 - 5P and supply with the equation Q = 100 + 5P.

a.Determine the equilibrium price and quantity.

b.Determine the surplus or shortage if the price were $100.

(Essay)

4.7/5 (36)

A change in the price of hamburgers will change the supply of hot dogs.

(True/False)

4.9/5 (27)

Equilibrium price and quantity are determined by the intersection of the demand and supply curves.

(True/False)

4.8/5 (37)

Price supports increase the supply of affordable milk for U.S.families.

(True/False)

4.9/5 (39)

If both the supply and demand curves shift to the left, then we can conclude that there will be

(Multiple Choice)

4.8/5 (42)

Why do price ceilings tend to cause persistent imbalances in the market?

(Multiple Choice)

4.9/5 (30)

Changes in consumer preference toward small, imported automobiles have shifted their demand curves downward and to the left.

(True/False)

4.8/5 (28)

In an attempt to reduce poaching of elephant tusks for ivory, officials in Kenya burned illegally gathered ivory.Economists tend to point out that

(Multiple Choice)

4.8/5 (38)

Legal limits on prices will tend to cause misallocation of resources because

(Multiple Choice)

4.8/5 (38)

The cost of processors and memory has decreased dramatically in the past twenty-five years.As a result, we have seen

(Multiple Choice)

4.8/5 (37)

The Red Jacket Mountain View Inn in New Hampshire charges $159 per room in the winter ski season and $114 during the summer months.The number of rooms and operating costs are constant year round.These prices indicate

(Multiple Choice)

4.7/5 (46)

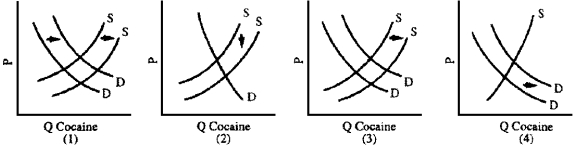

Figure 4-14

-Frustrated by the cost and ineffectiveness of the war on drugs, the U.S.government could consider "decriminalization" of the use and sale of cocaine.Critics contend that lower prices will expand drug use and that decriminalization will remove the stigma and danger from arrest associated with drug use, thus further increasing the demand and number of addicts.Which graph in Figure 4-14 best illustrates the critics' case?

-Frustrated by the cost and ineffectiveness of the war on drugs, the U.S.government could consider "decriminalization" of the use and sale of cocaine.Critics contend that lower prices will expand drug use and that decriminalization will remove the stigma and danger from arrest associated with drug use, thus further increasing the demand and number of addicts.Which graph in Figure 4-14 best illustrates the critics' case?

(Multiple Choice)

4.8/5 (37)

The law of increasing relative costs, depicted by the concavity of the production opportunities frontier, is most closely related to the

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)