Exam 13: Between Competition and Monopoly

Exam 1: What Is Economics254 Questions

Exam 2: The Economony: Myth and Reality184 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice278 Questions

Exam 4: Supply and Demand: an Initial Look297 Questions

Exam 5: Consumer Choice: Individual and Market Demand213 Questions

Exam 6: Demand and Elasticity247 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis246 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis232 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog225 Questions

Exam 10: The Firm and the Industry Under Perfect Competition219 Questions

Exam 11: The Case for Free Markets: the Price System251 Questions

Exam 12: Monopoly236 Questions

Exam 13: Between Competition and Monopoly248 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation152 Questions

Exam 15: The Shortcomings of Free Markets210 Questions

Exam 16: The Economics of the Environment, and Natural Resources218 Questions

Exam 17: Taxation and Resource Allocation218 Questions

Exam 18: Pricing the Factors of Production230 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs267 Questions

Exam 20: Poverty, Inequality, and Discrimination167 Questions

Exam 21: An Introduction to Macroeconomics212 Questions

Exam 22: The Goals of Macroeconomic Policy212 Questions

Exam 23: Economic Growth: Theory and Policy226 Questions

Exam 24: Aggregate Demand and the Powerful Consumer216 Questions

Exam 25: Demand-Side Equilibrium: Unemployment or Inflation215 Questions

Exam 26: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 27: Managing Aggregate Demand: Fiscal Policy207 Questions

Exam 28: Money and the Banking System222 Questions

Exam 29: Monetary Policy: Conventional and Unconventional208 Questions

Exam 30: The Financial Crisis and the Great Recession64 Questions

Exam 31: The Debate Over Monetary and Fiscal Policy216 Questions

Exam 32: Budget Deficits in the Short and Long Run214 Questions

Exam 33: The Trade-Off Between Inflation and Unemployment218 Questions

Exam 34: International Trade and Comparative Advantage215 Questions

Exam 35: The International Monetary System: Order or Disorder216 Questions

Exam 36: Exchange Rates and the Macroeconomy215 Questions

Exam 37: Contemporary Issues in the Useconomy23 Questions

Select questions type

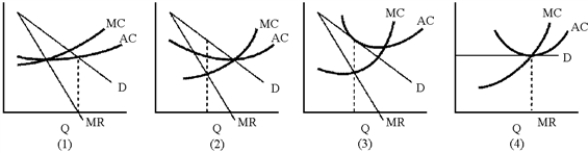

Figure 13-2

-In monopolistic competition, the long-run equilibrium results in zero economic profit of the firms in these industries.The key factor in this is

-In monopolistic competition, the long-run equilibrium results in zero economic profit of the firms in these industries.The key factor in this is

(Multiple Choice)

4.9/5  (44)

(44)

Perfect competition and pure monopoly are concepts useful primarily for realistic applications.

(True/False)

4.9/5 (38)

If firms meet together to decide on prices and outputs, there is

(Multiple Choice)

4.9/5 (40)

Oligopolistic firms never collude because they have almost no incentive to do so.

(True/False)

4.9/5 (47)

In the long run, a monopolistically competitive firm produces at minimum average cost.

(True/False)

5.0/5 (33)

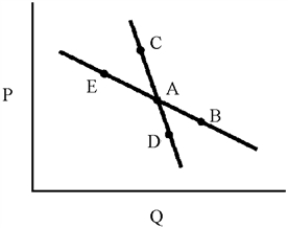

Figure 13-3

-Oligopolist A cuts price in an attempt to enlarge his share of the market.His competitors retaliate with identical price cuts.In this case, in Figure 13-3, oligopolist A will move from point A to which point?

-Oligopolist A cuts price in an attempt to enlarge his share of the market.His competitors retaliate with identical price cuts.In this case, in Figure 13-3, oligopolist A will move from point A to which point?

(Multiple Choice)

4.8/5 (36)

There are generally, in most areas, a large number of qualified physicians whose services are highly personalized.In addition to price, factors such as age, sex, location, and personality influence the choice of physician.Thus, the market is best described as

(Multiple Choice)

4.7/5 (46)

Where interdependence is especially pronounced, competition among oligopolists will

(Multiple Choice)

4.8/5 (39)

In John Rawls' A Theory of Justice, people choose the rules for distributing income from behind a veil of ignorance.People understand that ability determines income, but they do not know their abilities or the abilities of others.Rawls argues that people are risk averse and will choose the distribution rule that maximizes their income in the worst-case scenario (they have relatively little ability).An economist would call this strategy

(Multiple Choice)

4.8/5 (41)

The models of perfect competition and monopoly are the most realistic.

(True/False)

4.9/5 (44)

Price leadership is an example of explicit collusion by oligopolies.

(True/False)

4.9/5 (43)

Why is oligopoly more difficult to model than competition or monopoly?

(Essay)

4.8/5 (33)

In the long run, a monopolistically competitive firm and a perfectly competitive firm both produce at minimum average cost.

(True/False)

4.8/5 (42)

The monopolistically competitive firm in short-run equilibrium

(Multiple Choice)

4.9/5 (38)

Firms that practice tacit collusion may receive some of the benefits of a cartel without explicitly organizing a group of firms.

(True/False)

4.8/5 (39)

Suppose that firms in a monopolistically competitive industry are earning positive economic profits.In this situation, you would expect

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)