Exam 13: Short-Run Decision Making: Relevant Costing

Exam 1: Introduction to Managerial Accounting64 Questions

Exam 2: Basic Managerial Accounting Concepts238 Questions

Exam 3: Cost Behavior231 Questions

Exam 4: Cost-Volume-Profit Analysis: a Managerial Planning Tool185 Questions

Exam 5: Job-Order Costing196 Questions

Exam 6: Process Costing177 Questions

Exam 7: Activity-Based Costing and Management178 Questions

Exam 8: Absorption and Variable Costing, and Inventory Management125 Questions

Exam 9: Profit Planning186 Questions

Exam 10: Standard Costing: a Managerial Control Tool180 Questions

Exam 11: Flexible Budgets and Overhead Analysis173 Questions

Exam 12: Performance Evaluation and Decentralization167 Questions

Exam 13: Short-Run Decision Making: Relevant Costing170 Questions

Exam 14: Capital Investment Decisions172 Questions

Exam 15: Statement of Cash Flows185 Questions

Exam 16: Financial Statement Analysis190 Questions

Select questions type

Figure 13-3.

Elegance Bath Products, Inc. (EBP) makes a variety of ceramic sinks and tubs. EBP has just developed a line of sinks and tubs made from a mixture of glass and ceramic. The sinks sell for $150 each and have variable costs of $80. The tubs sell for $600 and have variable costs of $450. The glass and ceramic sinks and tubs require the use of specialized molding equipment. The specialized molding equipment has 4,050 hours of capacity per year. A sink uses an average of 2 hours of specialized molding equipment time; a tub uses an average of 5 hours of specialized molding equipment time.

-Refer to Figure 13-3. Assume that EBP can sell as many as 1,000 sinks and 500 tubs per year. How many tubs should EBP produce?

(Multiple Choice)

4.8/5  (26)

(26)

At split-off, the joint costs of production for joint products are not relevant to the sell-or-process-further decision.

(True/False)

4.8/5 (42)

The markup includes desired profit and any costs not included in the base cost.

(True/False)

4.9/5 (40)

Figure 13-9.

Sabor Inc. is a medical testing laboratory that performs several tests and analyses for hospitals in the area. Four of the tests that they perform require the use of a specialized machine that can supply 14,000 hours per year. Information on the four lab tests follows:

-Refer to Figure 13-9. What is the contribution margin per hour of machine time for Test C?

-Refer to Figure 13-9. What is the contribution margin per hour of machine time for Test C?

(Multiple Choice)

4.9/5 (41)

The managers of Computer World are trying to determine the best method of deciding the price of their new ultra minicomputer. This computer will present the customers with several unique features that their other computers do not offer. They have asked you to explain the advantages and disadvantages of the two costing methods they are considering; markup costing and target costing.

(Essay)

4.7/5 (44)

Information about three joint products follows:  The cost of the joint process is $140,000. Which of the joint products should be processed further?

The cost of the joint process is $140,000. Which of the joint products should be processed further?

(Multiple Choice)

4.7/5 (32)

_____________________ are simply those factors that are hard to put a number on, including things like political pressure and product safety.

(Short Answer)

4.8/5 (31)

The following information relates to a product produced by Creamer Company:  Fixed selling costs are $500,000 per year, and variable selling costs are $12 per unit sold. Although production capacity is 600,000 units per year, the company expects to produce only 400,000 units next year. The product normally sells for $120 each. A customer has offered to buy 60,000 units for $90 each.

The incremental cost per unit associated with the special order is

Fixed selling costs are $500,000 per year, and variable selling costs are $12 per unit sold. Although production capacity is 600,000 units per year, the company expects to produce only 400,000 units next year. The product normally sells for $120 each. A customer has offered to buy 60,000 units for $90 each.

The incremental cost per unit associated with the special order is

(Multiple Choice)

4.9/5 (36)

A decision involving a choice between internal and external production is what kind of decision?

(Multiple Choice)

4.8/5 (38)

______________ is the point at which products become distinguishable after passing through a common process.

(Short Answer)

4.8/5 (48)

Figure 13-3.

Elegance Bath Products, Inc. (EBP) makes a variety of ceramic sinks and tubs. EBP has just developed a line of sinks and tubs made from a mixture of glass and ceramic. The sinks sell for $150 each and have variable costs of $80. The tubs sell for $600 and have variable costs of $450. The glass and ceramic sinks and tubs require the use of specialized molding equipment. The specialized molding equipment has 4,050 hours of capacity per year. A sink uses an average of 2 hours of specialized molding equipment time; a tub uses an average of 5 hours of specialized molding equipment time.

-Refer to Figure 13-3. Assuming that specialized molding equipment time is the only constrained resource, and that EBP can sell as many tubs and sinks as it can produce, how many sinks should be sold?

(Multiple Choice)

4.7/5 (37)

Typically in a special-order decision, a customer wants to pay more than the usual price.

(True/False)

4.8/5 (36)

MATCHING

Match each statement with the correct item below.

a.

the difference in total cost between the alternatives in a decision

b.

determine whether or not a segment should be kept or dropped

c.

limited resources and limited demand for each product

d.

a specific set of procedures that produces a decision

e.

the point that products that have common processes and costs of production become distinguishable

f.

method of determining the cost of a product based on the price that customers are willing to pay

g.

decisions involving a choice between internal and external production

h.

products that have common processes and costs of production up to a point

i.

past costs that cannot be affected by future decisions

j.

a percentage applied to the base cost to cover other costs plus profit

k.

determine whether a specially priced order should be accepted or rejected

l.

determine whether it is more profitable to process a joint product further

-Keep-or-drop decisions

(Short Answer)

4.9/5 (31)

____________________ consists of choosing among alternatives with an immediate or limited end in view.

(Short Answer)

4.8/5 (38)

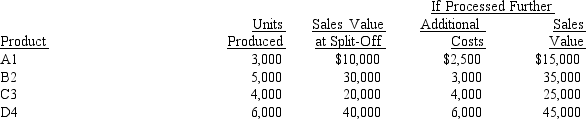

Stars Manufacturing Company produces Products A1, B2, C3, and D4 through a joint process. The joint costs amount to $200,000.  If Product B2 is processed further, profits will

If Product B2 is processed further, profits will

(Multiple Choice)

4.9/5 (47)

Figure 13-4.

Connolly Company produces two types of lamps, classic and fancy, with unit contribution margins of $13 and $21, respectively. Each lamp must spend time on a special machine. The firm owns four machines that together provide 18,000 hours of machine time per year. The classic lamp requires 0.20 hours of machine time, the fancy lamp requires 0.50 hours of machine time.

-Refer to Figure 13-4. What is the total contribution margin of the optimal mix of classic and fancy lamps?

(Multiple Choice)

4.8/5 (36)

The Exchange Company is in the process of developing a new product called LS500. The company requires a 35% profit. The LS500 current design carries with it a total cost of $125.

Required:

A. What is the sales price of the LS500 using markup costing?

B. Assume that the Exchange Company's marketing department has determined that consumers are willing to pay $140 for the LS500. What is the target cost for this product?

(Essay)

4.8/5 (36)

A company is considering a special order for 1,000 units to be priced at $8.90 (the normal price would be $11.50). The order would require specialized materials costing $4.00 per unit. Direct labor and variable factory overhead would cost $2.15 per unit. Fixed factory overhead is $1.20 per unit. However, the company has excess capacity and acceptance of the order would not raise total fixed factory overhead. The warehouse, however, would have to add capacity costing $1,300. Which of the following is relevant to the special order?

(Multiple Choice)

4.8/5 (43)

The benefit sacrificed or foregone when one alternative is chosen over another is known as the ____________________.

(Short Answer)

4.9/5 (45)

________________ refers to the relative amount of each product manufactured by a company.

(Short Answer)

5.0/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)