Exam 7: Activity-Based Costing and Management

Exam 1: Introduction to Managerial Accounting64 Questions

Exam 2: Basic Managerial Accounting Concepts238 Questions

Exam 3: Cost Behavior231 Questions

Exam 4: Cost-Volume-Profit Analysis: a Managerial Planning Tool185 Questions

Exam 5: Job-Order Costing196 Questions

Exam 6: Process Costing177 Questions

Exam 7: Activity-Based Costing and Management178 Questions

Exam 8: Absorption and Variable Costing, and Inventory Management125 Questions

Exam 9: Profit Planning186 Questions

Exam 10: Standard Costing: a Managerial Control Tool180 Questions

Exam 11: Flexible Budgets and Overhead Analysis173 Questions

Exam 12: Performance Evaluation and Decentralization167 Questions

Exam 13: Short-Run Decision Making: Relevant Costing170 Questions

Exam 14: Capital Investment Decisions172 Questions

Exam 15: Statement of Cash Flows185 Questions

Exam 16: Financial Statement Analysis190 Questions

Select questions type

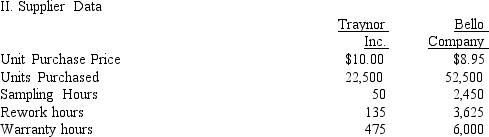

Figure 7-3.

Hamilton Company manufactures engines. Hamilton produces all the parts necessary for its engines except for one electronic component, which is purchased from two local suppliers: Traynor Inc. and Bello Company. Both suppliers are reliable and rarely deliver late; however, Traynor sells the component for $10.00 per unit and Bello sells the same component for $8.95. Hamilton purchases 70% of its components from Bello, because of the lower price. The total annual demand is 75,000 units.

-Refer to Figure 7-3. Suppose that Hamilton loses $2,500,000 in sales per year because of its reputation for defective units attributable to failed components. Using warranty hours, assign the proportional cost of lost sales to Traynor Inc. Then determine what effect this would have on the cost per component.

-Refer to Figure 7-3. Suppose that Hamilton loses $2,500,000 in sales per year because of its reputation for defective units attributable to failed components. Using warranty hours, assign the proportional cost of lost sales to Traynor Inc. Then determine what effect this would have on the cost per component.

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

D

Producing 10,000 units of a cell phone requires $300,000 of prime costs, uses 2,000 machine hours, and takes 1,200 setup hours. The activity rates are $40 per machine hour and $100 per setup hour. What is the unit cost of a cell phone?

Free

(Multiple Choice)

4.9/5 (35)

Correct Answer:Verified

C

Discretionary activities are necessary to comply with legal mandates.

Free

(True/False)

4.7/5 (42)

Correct Answer:Verified

False

Figure 7-3.

Hamilton Company manufactures engines. Hamilton produces all the parts necessary for its engines except for one electronic component, which is purchased from two local suppliers: Traynor Inc. and Bello Company. Both suppliers are reliable and rarely deliver late; however, Traynor sells the component for $10.00 per unit and Bello sells the same component for $8.95. Hamilton purchases 70% of its components from Bello, because of the lower price. The total annual demand is 75,000 units.

-Refer to Figure 7-3. Calculate the total activity cost per component associated with using Traynor Inc., as the supplier.

(Multiple Choice)

4.8/5 (41)

Each unit of a product requires four components. The average number of components is 4.25 due to component failure. Purchasing higher quality components can reduce the average number of components to four per unit. The cost per component is $350. Calculate the reduction in failure costs per unit due to purchasing higher quality components.

(Multiple Choice)

4.9/5 (35)

One way to improve efficiency is to produce higher activity output with higher cost.

(True/False)

4.8/5 (31)

Increasing the efficiency of necessary activities by using economies of scale is known as

(Multiple Choice)

4.8/5 (38)

Factors that measure the consumption of activities by products and other cost objects are value-added costs.

(True/False)

4.9/5 (45)

Figure 7-3.

Hamilton Company manufactures engines. Hamilton produces all the parts necessary for its engines except for one electronic component, which is purchased from two local suppliers: Traynor Inc. and Bello Company. Both suppliers are reliable and rarely deliver late; however, Traynor sells the component for $10.00 per unit and Bello sells the same component for $8.95. Hamilton purchases 70% of its components from Bello, because of the lower price. The total annual demand is 75,000 units.

-Refer to Figure 7-3. Calculate the total cost per component associated with using Bello Company as the supplier.

(Multiple Choice)

4.8/5 (32)

A(n) ____ is derived from the interview process (or written survey).

(Multiple Choice)

4.9/5 (29)

The activity driver for the shipping activity is the number of orders shipped. Product A uses 20 orders and Product B uses 60 orders. Calculate the consumption ratios for each product.

(Multiple Choice)

4.9/5 (36)

To calculate an activity rate, the ____ of each activity must be determined.

(Multiple Choice)

4.8/5 (35)

A plant produces 75 different electronic products. Each product requires an average of six components that are purchased externally. By redesigning the products, it is possible to produce the 75 products so that they all have three components in common. This will reduce the demand for purchasing, receiving, and paying bills. Estimated savings from the reduced demand are $1,200,000 per year. Calculate the nonvalue-added cost of purchasing, receiving and paying bills.

(Multiple Choice)

4.8/5 (35)

Figure 7-5.

Rizzo Manufacturing produces two types of cameras: 35mm and digital. The cameras are produced using one continuous process. Four activities have been identified: machining, setups, receiving, and packing. Resource drivers have been used to assign costs to each activity. The overhead activities, their costs, and the other related data are as follows:

-Refer to Figure 7-5. Calculate an activity rate for packing based on packing orders.

-Refer to Figure 7-5. Calculate an activity rate for packing based on packing orders.

(Multiple Choice)

4.9/5 (45)

The cost of recalls would be an example of a(n) ____________________.

(Short Answer)

4.9/5 (40)

To calculate an activity rate, the practical capacity of each activity must be determined.

(True/False)

4.8/5 (32)

____ focuses on the relationship of activity inputs to activity outputs.

(Multiple Choice)

4.8/5 (46)

Using only unit-based activity drivers to assign nonunit-related overhead costs can cause

(Multiple Choice)

4.7/5 (38)

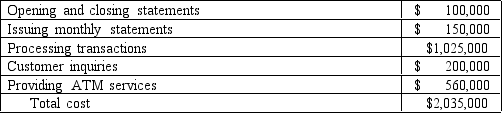

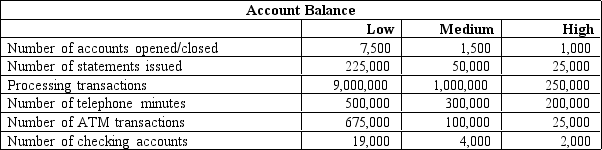

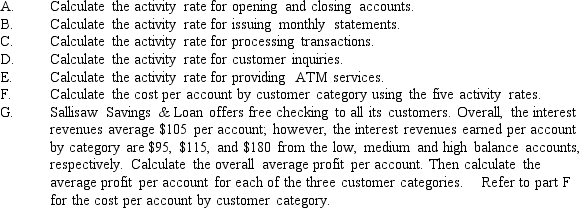

Figure 7-8.

Sallisaw Savings & Loan has requested an analysis of checking account profitability by customer type. Customers are categorized according to size of their account: low balances, medium balances, and high balances. The activities associated with the three different customer categories and their associated annual costs are as follows:

Additional data concerning the usage of the activities by the various customers are also provided:

Additional data concerning the usage of the activities by the various customers are also provided:

-Refer to Figure 7-8. Sallisaw uses an activity-based costing system. The activity rate for opening and closing statements is based on the number of accounts opened and closed. The activity rate for issuing monthly statements is based on the number of statements issued. The activity rate for processing transactions is based on the number of transactions processed. The activity rate for customer inquiries is based on the number of telephone minutes. The rate for ATM services is based on the number of ATM transactions.

-Refer to Figure 7-8. Sallisaw uses an activity-based costing system. The activity rate for opening and closing statements is based on the number of accounts opened and closed. The activity rate for issuing monthly statements is based on the number of statements issued. The activity rate for processing transactions is based on the number of transactions processed. The activity rate for customer inquiries is based on the number of telephone minutes. The rate for ATM services is based on the number of ATM transactions.

(Essay)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)