Exam 2: Procedures and Administration

Exam 1: Introduction to Federal Taxation in Canada144 Questions

Exam 2: Procedures and Administration92 Questions

Exam 3: Income or Loss From an Office or Employment108 Questions

Exam 4: Taxable Income and Tax Payable for Individuals105 Questions

Exam 5: Capital Cost Allowance95 Questions

Exam 6: Income or Loss From a Business103 Questions

Exam 7: Income From Property89 Questions

Exam 8: Capital Gains and Capital Losses104 Questions

Exam 9: Other Income, Other Deductions, and Other Issues130 Questions

Exam 10: Retirement Savings and Other Special Income Arrangements95 Questions

Exam 11: Taxable Income and Tax Payable for Individuals Revisited106 Questions

Exam 12: Taxable Income and Tax Payable for Corporations89 Questions

Exam 13: Taxation of Corporate Investment Income79 Questions

Exam 14: Other Issues in Corporate Taxation96 Questions

Exam 15: Corporate Taxation and Management Decisions93 Questions

Exam 16: Rollovers Under Section 8585 Questions

Exam 17: Other Rollovers and Sale of an Incorporated Business92 Questions

Exam 18: Partnerships96 Questions

Exam 19: Trusts and Estate Planning92 Questions

Exam 20: International Issues in Taxation66 Questions

Exam 21: Gst-Hst82 Questions

Select questions type

The interest rate applicable on refunds to individuals is 4 percentage points less than the interest rate applicable on amounts owing to the CRA.

Free

(True/False)

4.8/5  (45)

(45)

Correct Answer: Verified

Verified

False

Which of the following statements is correct?

Free

(Multiple Choice)

4.7/5 (31)

Correct Answer:Verified

D

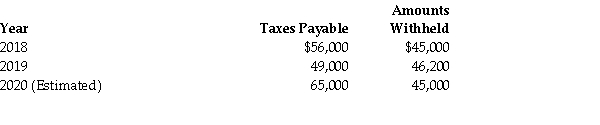

A Canadian public company has Tax Payable of $62,000 in 2018, $95,000 in 2019, and $75,000 in 2020. The company would like to minimize its 2020 instalments. What would its instalments be?

Free

(Multiple Choice)

4.9/5 (31)

Correct Answer:Verified

C

One way to ensure that no interest will be assessed for late instalments is:

(Multiple Choice)

4.8/5 (40)

Mr. James Simon has asked for your services with respect to dealing with a Notice of Reassessment requesting additional tax for the 2016 taxation year which he says he has just received. Your first interview takes place a week later, on April 25, 2020, and Mr. Simon informs you that he has had considerable difficulty with the CRA in past years and, on two occasions in the past five years, he has been required to pay penalties as well as interest.

With respect to the current reassessment, he assures you that he has complied with the law and that there is a misunderstanding on the part of the assessor. After listening to him describe the situation, you decide it is likely that his analysis of the situation is correct.

Required: Indicate what additional information should be obtained during the interview with Mr. Simon and what steps should be taken if you decide to accept him as a client.

(Essay)

5.0/5 (42)

All corporations must file their tax returns no later than six months after the end of their fiscal year, and pay any balance of tax owing no later than three months after the end of their fiscal year.

(True/False)

4.7/5 (42)

The notice of objection for a corporation must be filed within 90 days from the date of mailing of the notice of assessment.

(True/False)

4.9/5 (36)

By making all instalments on the basis of the CRA's instalment reminder, the taxpayer is assured that no interest will be assessed for deficient instalments. However, this may not be the best alternative for making instalment payments. Explain why this is true.

(Essay)

4.7/5 (38)

If an individual dies after October in a particular taxation year, his legal representatives must file his tax return by the later of his normal filing due date and six months after the date of his death.

(True/False)

4.8/5 (45)

If an individual is required to make quarterly instalment payments on their income taxes, how is the required amount of the instalments determined?

(Essay)

4.8/5 (39)

For each of the following independent cases, indicate whether you believe any penalty would be assessed under ITA 163.2 on any of the parties involved. Explain your conclusion.

Case 1

In preparing a tax return for one of his established clients, an accountant relies on the financial statements that another accountant has prepared for the client's business income. Nothing in these statements seemed unreasonable.

On audit, the CRA finds that the business income financial statements prepared by the other accountant contained material misrepresentations.

Case 2

An accountant is asked to prepare tax return for a new client. The accountant had no previous acquaintance with the individual.

The client provides statements, prepared using the appropriate tax figures, showing a net business income of $45,000. He has no other income. He indicates that, during the current year, he made a $32,000 contribution to a registered Canadian charity, but has lost the receipt and has requested a duplicate. As it is now April 29, in order to avoid a late filing penalty, the accountant e-files the tax return, claiming a tax credit for the contribution without seeing the receipt.

Case 3

An accountant has been engaged by a new client to use his records to prepare an income statement and to use the information in this statement to prepare a tax return. As part of this engagement, the accountant reviews both the expense and revenue information that has been provided to him by the new client. He finds revenues of $285,000 and expenses of $201,000. The information used to arrive at these figures seems reasonable and, given this, the accountant files the required tax return.

When the client is audited, the CRA finds a large proportion of the expenses claimed cannot be substantiated by adequate documentation and may not have been incurred. Furthermore, it appears that the client has a substantial amount of unreported revenues.

Case 4

An accountant who lives in an expensive neighbourhood notices that the house next door has just been sold. It was listed for $1 million. The accountant introduces himself to the new neighbour and they become friends.

At tax time the friend hires the accountant to prepare his return. The accountant is given a T4 with $25,000 in income reported. Thinking that the gross income is on the low side, the accountant asks if this is all the income he has and the friend replies that it is so. The accountant is still not satisfied with the answer as the income seems to be out of proportion with the living standard of the friend, so he then asks him if he has received money from any source other than his employment and the friend replies that he received a substantial inheritance from his mother last year.

The accountant does not ask any further questions and prepares and files the return. When the friend is audited it is discovered that he has over $200,000 in unreported income.

Case 5

Units in a new limited partnership tax shelter are being sold by a company. The company has established this limited partnership by acquiring a software application in the open market for $100,000. However, the prospectus prepared by the company states that the fair market value of the application is $5,000,000, a value that was supported by an independent appraiser. The tax shelter is registered with the CRA and is available as an investment opportunity in the current year.

On audit, the CRA determines that the $100,000 that was paid for the software application is, in fact, its fair market value on the date of the transfer. In discussing the matter with the independent appraiser, the CRA finds that the appraisal was not prepared using normal valuation procedures. In addition, the appraiser based his work entirely on assumptions and facts that were provided by the company. The appraiser was paid $50,000 for his work.

Case 6 (Requires Basic GST/HST Knowledge)

An accountant is asked to file a HST return for a client who has not kept records of the HST paid or payable on her business purchases for the year. However, the client does have financial statements for her business which, after a brief review, the accountant finds to be reasonable.

In his review, the accountant found that these statements contain large amounts for wages and interest expense, as well as a significant amount of purchases that are zero-rated. (HST is not paid on any of these types of expenses). In preparing the HST return, the accountant applies a factor of 13/113 to all of the expenses shown in the income statement. This results in an overstatement of input tax credits reported on the HST return.

(Essay)

4.9/5 (35)

John Barron is self-employed and plans to file his 2020 tax return on June 15, 2021. His balance-due day is:

(Multiple Choice)

4.9/5 (39)

In some situations, an employee may request an increase in the amounts that are withheld for future income taxes. What circumstances might lead an employee to make such a request?

(Essay)

4.8/5 (39)

The GAAR provisions are not applicable to gifts to adult children.

(True/False)

4.9/5 (34)

Cases can be heard by the Tax Court of Canada using either the general or the informal procedures. How do these two procedures differ?

(Essay)

4.8/5 (32)

The taxation year end for Grange Inc. is March 31, 2020. It is a Canadian controlled private corporation that claims the small business deduction and had Taxable Income for the year ending March 31, 2019 of $165,000. Indicate the date on which the corporate tax return for the year ending March 31, 2020 must be filed, as well as the date on which any final payment of taxes is due.

(Essay)

4.8/5 (34)

Dora Chen has determined that her minimum tax instalments for 2020 are $8,000 per quarter. She also owes $30,000 on her credit card, which carries an interest rate of 20%. She has destroyed her credit card, so no more can be put on it. Dora is unable to pay both the entire instalment amounts and her credit card balance, but she does have $8,000 in cash each quarter for her debts. Which of the following would be the best choice for Dora from a financial planning perspective?

(Multiple Choice)

4.7/5 (41)

On April 30 of the current year, her filing due date, Nicole Houde finds that she has a significant net tax owing. She will not be able to pay this until the beginning of July. She doesn't want to file her return until she has the funds available to pay the balance. What advice would you give Ms. Houde in this regard?

(Essay)

4.8/5 (30)

For the three years ending December 31, 2018 through December 31, 2020, a corporation's combined federal and provincial Tax Payable is as follows:  Case One

The taxpayer is a small CCPC.

Case Two

The taxpayer is a small CCPC. Assume that its combined federal and provincial taxes payable for the year ending December 31, 2019 were $163,420, instead of the $186,540 given in the problem.

Case Three

The taxpayer is a publicly traded corporation.

Case Four

The taxpayer is a publicly traded corporation. Assume that its combined federal and provincial taxes payable for the year ending December 31, 2019 were $163,420, instead of the $186,540 given in the problem.

Required: For each of the preceding independent Cases, provide the following information:

1. Indicate whether instalments are required during 2020. Provide a brief explanation of your conclusion.

2. Calculate the amount of instalments that would be required under each of the acceptable methods available.

3. Indicate which of the available methods would best serve to minimize instalment payments.

Case One

The taxpayer is a small CCPC.

Case Two

The taxpayer is a small CCPC. Assume that its combined federal and provincial taxes payable for the year ending December 31, 2019 were $163,420, instead of the $186,540 given in the problem.

Case Three

The taxpayer is a publicly traded corporation.

Case Four

The taxpayer is a publicly traded corporation. Assume that its combined federal and provincial taxes payable for the year ending December 31, 2019 were $163,420, instead of the $186,540 given in the problem.

Required: For each of the preceding independent Cases, provide the following information:

1. Indicate whether instalments are required during 2020. Provide a brief explanation of your conclusion.

2. Calculate the amount of instalments that would be required under each of the acceptable methods available.

3. Indicate which of the available methods would best serve to minimize instalment payments.

(Essay)

4.8/5 (40)

Horace Greesom filed his 2019 return on time. At the beginning of 2020, the following information relates to Mr. Greesom:  What amounts will be shown on the Instalment Reminder notices for 2020 and when will the amounts be due? Should he pay those amounts? Explain your conclusion.

What amounts will be shown on the Instalment Reminder notices for 2020 and when will the amounts be due? Should he pay those amounts? Explain your conclusion.

(Essay)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)