Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis

Exam 1: What Is Economics261 Questions

Exam 2: The Economy: Myth and Reality185 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice290 Questions

Exam 4: Supply and Demand: an Initial Look337 Questions

Exam 5: Consumer Choice: Individual and Market Demand243 Questions

Exam 6: Demand and Elasticity254 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis260 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis234 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog227 Questions

Exam 10: The Firm and the Industry Under Perfect Competition253 Questions

Exam 11: The Case for Free Markets: the Price System259 Questions

Exam 12: Monopoly244 Questions

Exam 13: Between Competition and Monopoly254 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation155 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, Externaliteis, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination171 Questions

Exam 21: International Trade and Comparative Advantage226 Questions

Exam 22: Contemporary Issues in the Us Economy23 Questions

Select questions type

Average physical product measures the increase in total output that results from a one-unit increase in an input.

(True/False)

4.9/5  (47)

(47)

The marginal revenue product of an hour of labor used in steel production is equal to

(Multiple Choice)

4.9/5 (32)

Most firms have very little flexibility in their choice of input proportions.

(True/False)

4.9/5 (32)

Which of the following equations defines marginal revenue product?

(Multiple Choice)

4.8/5 (33)

The firm's average cost curve is the result of cost minimization in the use of fixed inputs.

(True/False)

4.8/5 (30)

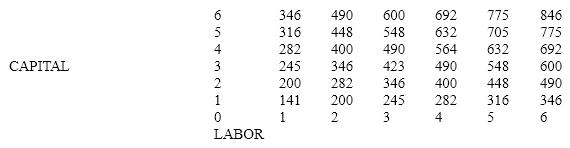

Table 7-4  Table 7-4 shows a production relationship. Assuming the labor input is fixed at 4, what will be the optimum capital input assuming an output price of $1 and a $90-per-day cost for one unit of capital?

Table 7-4 shows a production relationship. Assuming the labor input is fixed at 4, what will be the optimum capital input assuming an output price of $1 and a $90-per-day cost for one unit of capital?

(Multiple Choice)

4.8/5 (33)

If the price of one input changes, generally the firm will change its use of both inputs.

(True/False)

4.9/5 (39)

Production technology determines the relationship of total cost to outputs.

(True/False)

4.9/5 (47)

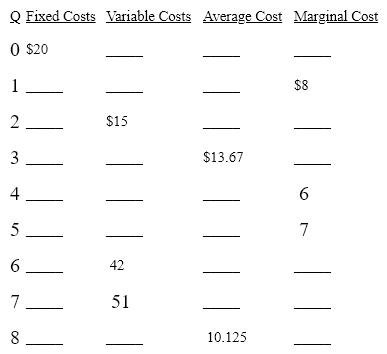

Complete the table below by computing the missing numbers from those that are given.

(Essay)

4.8/5 (26)

When the marginal revenue product of an input is less than its price, the

(Multiple Choice)

4.8/5 (31)

Diminishing marginal returns explains why a firm's long-run average total cost curve is U shaped.

(True/False)

4.8/5 (35)

A factory produces 1,000 radios a year, AVC = $10 and TFC = $5,000. The factory's TC

(Multiple Choice)

4.9/5 (42)

In the typical AC curve, the downward-sloping part is attributable to

(Multiple Choice)

4.8/5 (35)

An example of the law of variable input proportions can be found in

(Multiple Choice)

4.8/5 (36)

Cost minimization is the process of making optimal use of all of the inputs whose quantities are

(Multiple Choice)

4.7/5 (37)

The behavior of historical cost curves says nothing about the cost advantages or disadvantages of a single large firm.

(True/False)

4.7/5 (36)

On Naomi's pig farm, Naomi hires all the labor used, grows all the grain fed to the pigs, and owns the barn. The costs used to calculate the total cost curve include

(Multiple Choice)

4.9/5 (36)

For a typical firm, the portion of the AC curve that is downward-sloping is because production

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)