Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis

Exam 1: What Is Economics261 Questions

Exam 2: The Economy: Myth and Reality185 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice290 Questions

Exam 4: Supply and Demand: an Initial Look337 Questions

Exam 5: Consumer Choice: Individual and Market Demand243 Questions

Exam 6: Demand and Elasticity254 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis260 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis234 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog227 Questions

Exam 10: The Firm and the Industry Under Perfect Competition253 Questions

Exam 11: The Case for Free Markets: the Price System259 Questions

Exam 12: Monopoly244 Questions

Exam 13: Between Competition and Monopoly254 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation155 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, Externaliteis, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination171 Questions

Exam 21: International Trade and Comparative Advantage226 Questions

Exam 22: Contemporary Issues in the Us Economy23 Questions

Select questions type

The short run is the time period during which

Free

(Multiple Choice)

4.8/5  (21)

(21)

Correct Answer: Verified

Verified

D

If diminishing marginal returns are present for an input, then the marginal revenue product will be decreasing.

Free

(True/False)

4.7/5 (33)

Correct Answer:Verified

True

A change in input prices has no impact on a firm's budget line.

Free

(True/False)

4.9/5 (35)

Correct Answer:Verified

False

A cost curve drawn with years on the horizontal axis and costs per unit on the vertical axis would be a(n)

(Multiple Choice)

4.9/5 (40)

A firm is operating with an optimal combination of inputs. Suddenly the price of one input rises. The firm should

(Multiple Choice)

4.9/5 (27)

A change in one input price will cause the slope of the firm's budget line to change.

(True/False)

4.8/5 (36)

Higher production indifference curves correspond to larger amounts of one input in relation to a second input.

(True/False)

4.9/5 (36)

For most industries, average costs decrease indefinitely as output expands.

(True/False)

5.0/5 (44)

Decreasing returns to scale is strictly a short run phenomenon for firms.

(True/False)

4.8/5 (35)

If a firm has increasing returns to scale at all levels of output, the

(Multiple Choice)

4.9/5 (31)

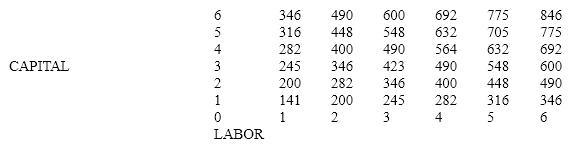

Table 7-4  The production relationship in Table 7-4 indicates a process characterized by

The production relationship in Table 7-4 indicates a process characterized by

(Multiple Choice)

4.9/5 (42)

"Assuming the long-run average cost curve is U shaped, a firm will always seek to operate at the lowest point on the long-run average cost curve.

(True/False)

4.9/5 (31)

A production indifference curve describes the input combinations that will produce a given output.

(True/False)

4.7/5 (26)

In Table 7-1, the average physical product after five workers are hired is

In Table 7-1, the average physical product after five workers are hired is

(Multiple Choice)

5.0/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)