Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics261 Questions

Exam 2: The Economy: Myth and Reality185 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice290 Questions

Exam 4: Supply and Demand: an Initial Look337 Questions

Exam 5: Consumer Choice: Individual and Market Demand243 Questions

Exam 6: Demand and Elasticity254 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis260 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis234 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog227 Questions

Exam 10: The Firm and the Industry Under Perfect Competition253 Questions

Exam 11: The Case for Free Markets: the Price System259 Questions

Exam 12: Monopoly244 Questions

Exam 13: Between Competition and Monopoly254 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation155 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, Externaliteis, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination171 Questions

Exam 21: International Trade and Comparative Advantage226 Questions

Exam 22: Contemporary Issues in the Us Economy23 Questions

Select questions type

Economists assume that business firms have many goals, and profit maximization is just one of them.

(True/False)

4.8/5  (28)

(28)

The federal government, in order to fund expanded health care, imposes a lump-sum tax on all business property. Profit-maximizing firms that stay in business will respond by

(Multiple Choice)

4.8/5 (23)

Marginal cost curves and average cost curves are both purely upward sloping.

(True/False)

4.7/5 (38)

Profit is maximized at the output at which marginal revenue exceeds marginal cost by the greatest margin.

(True/False)

4.9/5 (35)

In arriving at the quantity of output and price of its product, a company

(Multiple Choice)

4.9/5 (37)

Some companies follow a strategy of sales maximization. They say that this puts them in close touch with their customers and they can better track the market, responding to needs more quickly. However, this increases costs because of the need to stock a wider variety of parts, sizes, colors, etc. What would make this strategy a profit-maximizing one?

(Essay)

4.8/5 (40)

If the price of a product is $10 per unit and the variable cost per unit is $5, the firm is making a profit.

(True/False)

4.8/5 (38)

Distinguish between the economist's definition of profit and the accountant's definition. Which is superior for decision making?

(Essay)

4.8/5 (28)

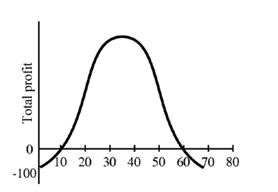

Figure 8-5

-In Figure 8-5, the firm's marginal profit at the profit maximizing output level

-In Figure 8-5, the firm's marginal profit at the profit maximizing output level

(Multiple Choice)

4.8/5 (49)

In the short run, which are most important in determining changes in output?

(Multiple Choice)

5.0/5 (34)

Total profit = Total revenue − Total cost (including opportunity cost). Total profit defined in this way is called

(Multiple Choice)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)