Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics261 Questions

Exam 2: The Economy: Myth and Reality185 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice290 Questions

Exam 4: Supply and Demand: an Initial Look337 Questions

Exam 5: Consumer Choice: Individual and Market Demand243 Questions

Exam 6: Demand and Elasticity254 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis260 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis234 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog227 Questions

Exam 10: The Firm and the Industry Under Perfect Competition253 Questions

Exam 11: The Case for Free Markets: the Price System259 Questions

Exam 12: Monopoly244 Questions

Exam 13: Between Competition and Monopoly254 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation155 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, Externaliteis, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination171 Questions

Exam 21: International Trade and Comparative Advantage226 Questions

Exam 22: Contemporary Issues in the Us Economy23 Questions

Select questions type

Most consumers in stores use marginal analysis to make their buying decisions.

(True/False)

4.9/5  (30)

(30)

The difference between economic profit and accountant's definition of profit is that an economist's total cost counts the ____ of inputs.

(Multiple Choice)

4.9/5 (34)

Many large universities rent out parts of their campuses to conference groups during the summer because such groups cause little damage, require little staff attention, and bring in large amounts of income. A university's decision to rent its campus to a conference group is most clearly based on

(Multiple Choice)

4.8/5 (33)

The addition to total revenue resulting from one more unit of output is called marginal revenue.

(True/False)

4.9/5 (39)

If a firm has determined its optimal output level, where MR = MC, then price

(Multiple Choice)

4.9/5 (40)

In reality, decisions made by firms may not always produce maximum total profit because some executives

(Multiple Choice)

4.8/5 (44)

A grocery store sells soup for $1.50 a can, or $2.50 for two cans. To a customer, the marginal cost of buying the second can of soup is

(Multiple Choice)

4.8/5 (42)

A computer manufacturer sells 1,000 units per month at $500 each. A price cut to $400 is being considered. His marginal cost is constant at $300 per unit. To maintain profits, quantity sold must increase to at least

(Multiple Choice)

4.8/5 (25)

Accounting profit differs from economic profit by the amount of the explicit costs faced by a firm.

(True/False)

4.8/5 (29)

The rule of equating marginal benefit with marginal cost is a tool that can be applied to a wide variety of decisions, not just economics.

(True/False)

4.8/5 (35)

The demand curve for a firm's product is also the curve showing

(Multiple Choice)

4.8/5 (38)

In arriving at the quantity of output and price of its product, a company

(Multiple Choice)

4.8/5 (28)

Marginal revenue is the addition to total revenue resulting from the addition of one unit to total output.

(True/False)

4.8/5 (37)

A graph of total profits is always likely to be positively sloped throughout its length.

(True/False)

4.7/5 (25)

A firm is generally more interested in marginal profits than in total profits.

(True/False)

4.8/5 (36)

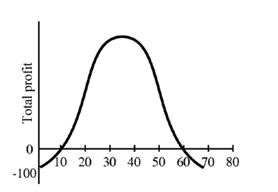

Figure 8-5

In Figure 8-5, profits are maximized at output of

In Figure 8-5, profits are maximized at output of

(Multiple Choice)

4.8/5 (29)

Firms can make decisions using marginal analysis even if they do not know the shape of a demand curve.

(True/False)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)