Exam 6: Chinas Path of Investment

In this chapter we discussed the user cost of capital and PE ratio (the home price to annual rental ratio): where user cost = (1 ? t)(r + p) + m + ? + ? ? ?e where t is the personal tax rate, r is the borrowing cost of financing a home, p is the property tax rate, m is the cost of maintenance, ? is the risk premium on property, ?e is the expected appreciation of property values and ? is the depreciation rate on residential property (all expressed in nominal percent).

a. If in the United States, home prices are expected to increase by 3 percent r = 4 percent, the tax rate is 25 percent, property tax is 1 percent, the maintenance fee is 0.5 percent, depreciation is 3.5 percent and the risk premium is 2 percent, calculate the PE Ratio.

b. If some Chinese cities have a PE of let's say 30, calculate the implicit value of ??. Provide justification for the other numbers that you used in the formula for the China case. Do you think ?? is based on rational or adaptive expectations?

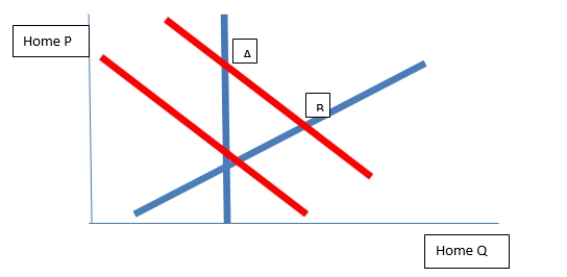

c. In this chapter, Schramm suggests that the housing market price surge in China represents fundamental factors and not a bubble. Buyers may still end up losing money over the long term, however. Explain using basic supply and demand curves. If Schramm is correct, then why haven't rental rates risen as dramatically as home prices? Is Schramm wrong? Explain.

a. Using the above equation: 1/PE = (1 ? .25)(.04 + .01) + .005 + .035+ .02 ? .03

we have PE = 14.8.

b. One Scenario:

1/ 30= (1-0) (.0655+0) + .001 + .045 + .04 -implies = 11.8 % for a very long time. This would be faster than we expect nominal GDP to rise for a prolonged period, so it seems too optimistic. In this sense, it must be based on adaptive expectations.

c. in a nutshell, we have a short run supply which is vertical but a long run supply with some elasticity. If demand grows rapidly we get caught first on the short run curve (A) but eventually prices settle down to the long run curve (B).

Renting is not a perfect substitute for a home. When you buy a home in many cities you may get two very important things: A hukou and a bride. You will likely not get these if you rent in an urban area in China.

Renting is not a perfect substitute for a home. When you buy a home in many cities you may get two very important things: A hukou and a bride. You will likely not get these if you rent in an urban area in China.

When investment is a large fraction of GDP output, as in China, why does this present special challenges in measuring the quality of economic growth as compared to the quantity of economic growth?

If most output is consumption we can value that pretty easily; at the margin its value is worth what a consumer pays for the product or service when purchased. Investment goods are trickier - especially in China. Purchases of investment goods (like a new building) are often between "related parties" or government controlled entities and we are not fully confident that what is paid for these investment goods reflect true value. In the case of investment goods, we only understand its value as it yields benefits over many decades. Ideally, those benefits would be to consumers for sake of measurement. But if the benefits are too more users of investment, we are sort of "kicking the can down the road." Thus, when half of a country's GDP is devoted to investment, we can measure that in a quantity sense, but are measurement may misprice in terms of quality or true value.

Discuss the neoclassical framework as it relates to decision making on Chinese investment:

a. Provide the neoclassical framework for investment and link that to the traditional cash flow Net Present Value approach.

b. Discuss whether the approach in (a) is applicable to China. Is it more relevant for some sectors instead of others? Which sectors of the economy?

c. Why are the questions in (a) and (b) vitally important for China in the coming years?

a. (from Macro Finance Insight 6.1):

which yields

Here, can be defined as the increment to perpetual cash flow from an increase in one unit of capital today. Investment as , and assuming a perpetually level cash flow that can increase as a result of in capital. Thus we have:

To maximize, with respect to , we set

which yields

b. There are really two issues (questions) here. Firstly, is the model relevant to all sectors in China? Secondly, if it is relevant are the costs and returns market based or are they distorted due to some form of financial repression (non-market controls in financial markets)? For the first question, those sectors which are non-government (private companies and entrepreneurs) which make up about 2/3 of all investment probably do use such a model. The second question though relates to the complex structure of China's financial markets, which remain segmented between favored borrowers (often with government ties) and non-favored borrowers. The latter use a cost of capital that is artificially high, the former a cost of capital that is artificially low.

c. Investment yields value in the future. Since such a large part of the economy is devoted to investment, we want to be sure that society's scarce resources (savings) are not being wasted.

Explain the costs and benefits of providing public works projects (infrastructure) via the financing mechanism of the China Development Bank as compared to a taxation mechanism for public works (let's say a property tax or personal income tax) in China.

In this chapter we derived: P × MPK = rental cost of capital or r

a. From the cash-flow valuation approach, assume that cash flows are growing at a rate of g. Derive the above equilibrium condition in this case.

b. Based on your answer in (a), explain in a neoclassical sense why China's investment rates are so high compared to the United States.

Explain why measuring the "cost of capital" (a difficult task anywhere in the world) is particularly difficult to measure in China.

Go to FRED (the Federal Reserve Economic Database) and update Chinese investment as a share of GDP.

Why can the stability (that it fluctuates so little year to year) of China's investment as a share of GDP be viewed as a "blessing," a "curse," and a worrisome omen?

In terms of measuring the size of the government sector in China, explain why it is important to understand how GDP's components of C, I, G, and NX are being measured in a GDP accounting sense?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)