Exam 9: Operating Activities

Recording municipal bond interest received in the general ledger will generate a _________________ difference

Permanent

Which of the following is not a distinguishing characteristic of a derivative instrument?

C

Firm D holds 20,000 gallons of chemicals in inventory on October 31,Year 1,that cost $225

per gallon.Firm D contemplates selling the chemicals on March 31,Year 2,when it completes

the processing.Uncertainty about the selling price of the chemical on March 31,Year 2,leads

Firm D to acquire a forward contract on the chemical.The forward contract does not require an initial investment of funds.Firm D designates the forward commodity contract as a cash flow hedge of an anticipated transaction.The forward price on October 31,Year 1,for delivery on March 31,Year 2,is $320 per gallon.

Required: a.Using the financial statement effects template,show the financial statement effects,

if any,that Firm D would have on October 31,Year 1,when it acquires the forward

commodity price contract.

b.On December 31,Year 1,the end of the accounting period for Firm D,the forward

price of the chemical for March 31,Year 2,delivery is $310 per gallon.Show the financial

statement effects of recording the change in the value of the forward commodity

price contract.Ignore the discounting of cash flows in this part and in the remainder

of the problem.

c.Show the financial statement effects of the December 31,Year 1,decline in value of

the chemical inventory.

d.On March 31,Year 2,the price of the chemical declines to $270 per gallon.Show the

financial statement effects of revaluing the forward contract.

e.Show the financial statement effects on March 31,Year 2,to reflect the decline in

value of the inventory.

f.Show the financial statement effects on March 31,Year 2,to settle the forward contract.

g.Assume that Firm D sells the chemical on March 31,Year 2,for $270 a gallon.Show

the financial statement effects of recording the sale and recognizing the cost of

goods sold.

a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d.

above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical.

accounting for Forward Commodity Price Contract as a Cash Flow Hedge

December 31,2010 Revaluation

![a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d. above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical. accounting for Forward Commodity Price Contract as a Cash Flow Hedge December 31,2010 Revaluation Forward Contract 200,000 OCI-Forward Commodity Contract 200,000 OCI-Forward Commodity Contract 200,000 Inventory 200,000 March 31,2011 Revaluation Forward Contract 800,000 OCI-Forward Commodity Contract 800,000 OCI-Forward Commodity Contract 800,000 Inventory 800,000 Closing of Forward Contract and Sale of Inventory Cash 1,000,000 Forward Contract 1,000,000 Cash 5,400,000 Sales Revenue 5,400,000 Cost of Goods Sold 3,500,000 Inventory 3,500,000](https://storage.examlex.com/TB2093/11ea427f_2408_af69_8d65_afb3ef3390be_TB2093_00.jpg)

Forward Contract 200,000

OCI-Forward Commodity Contract 200,000

![a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d. above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical. accounting for Forward Commodity Price Contract as a Cash Flow Hedge December 31,2010 Revaluation Forward Contract 200,000 OCI-Forward Commodity Contract 200,000 OCI-Forward Commodity Contract 200,000 Inventory 200,000 March 31,2011 Revaluation Forward Contract 800,000 OCI-Forward Commodity Contract 800,000 OCI-Forward Commodity Contract 800,000 Inventory 800,000 Closing of Forward Contract and Sale of Inventory Cash 1,000,000 Forward Contract 1,000,000 Cash 5,400,000 Sales Revenue 5,400,000 Cost of Goods Sold 3,500,000 Inventory 3,500,000](https://storage.examlex.com/TB2093/11ea427f_2408_af6a_8d65_b75fda236203_TB2093_00.jpg)

OCI-Forward Commodity Contract 200,000

Inventory 200,000

March 31,2011 Revaluation

![a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d. above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical. accounting for Forward Commodity Price Contract as a Cash Flow Hedge December 31,2010 Revaluation Forward Contract 200,000 OCI-Forward Commodity Contract 200,000 OCI-Forward Commodity Contract 200,000 Inventory 200,000 March 31,2011 Revaluation Forward Contract 800,000 OCI-Forward Commodity Contract 800,000 OCI-Forward Commodity Contract 800,000 Inventory 800,000 Closing of Forward Contract and Sale of Inventory Cash 1,000,000 Forward Contract 1,000,000 Cash 5,400,000 Sales Revenue 5,400,000 Cost of Goods Sold 3,500,000 Inventory 3,500,000](https://storage.examlex.com/TB2093/11ea427f_2408_af6b_8d65_dffd91c867eb_TB2093_00.jpg)

Forward Contract 800,000

OCI-Forward Commodity Contract 800,000

![a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d. above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical. accounting for Forward Commodity Price Contract as a Cash Flow Hedge December 31,2010 Revaluation Forward Contract 200,000 OCI-Forward Commodity Contract 200,000 OCI-Forward Commodity Contract 200,000 Inventory 200,000 March 31,2011 Revaluation Forward Contract 800,000 OCI-Forward Commodity Contract 800,000 OCI-Forward Commodity Contract 800,000 Inventory 800,000 Closing of Forward Contract and Sale of Inventory Cash 1,000,000 Forward Contract 1,000,000 Cash 5,400,000 Sales Revenue 5,400,000 Cost of Goods Sold 3,500,000 Inventory 3,500,000](https://storage.examlex.com/TB2093/11ea427f_2408_af6c_8d65_7fef27e0a3d1_TB2093_00.jpg)

OCI-Forward Commodity Contract 800,000

Inventory 800,000

Closing of Forward Contract and Sale of Inventory

![a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d. above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical. accounting for Forward Commodity Price Contract as a Cash Flow Hedge December 31,2010 Revaluation Forward Contract 200,000 OCI-Forward Commodity Contract 200,000 OCI-Forward Commodity Contract 200,000 Inventory 200,000 March 31,2011 Revaluation Forward Contract 800,000 OCI-Forward Commodity Contract 800,000 OCI-Forward Commodity Contract 800,000 Inventory 800,000 Closing of Forward Contract and Sale of Inventory Cash 1,000,000 Forward Contract 1,000,000 Cash 5,400,000 Sales Revenue 5,400,000 Cost of Goods Sold 3,500,000 Inventory 3,500,000](https://storage.examlex.com/TB2093/11ea427f_2408_af6d_8d65_5380d4906516_TB2093_00.jpg)

Cash 1,000,000

Forward Contract 1,000,000

![a. Firm D does not make an entry on October 1,2010,because the forward commodity price contract is a mutually unexecuted contract and requires no initial investment.b. The value of the forward contract increases $200,000 [= 20,000 x ($320 - $310)].The forward contract is an asset because the firm has the right to sell the chemical at $320 a gallon,whereas the forward rate for settlement on March 31,2011,suggests that other firms will sell the chemical for only $310 per gallon on that date.The increase in the asset is recognized as an increase in other comprehensive income.c. Inventory is written down by the same amount,resulting in a decrease in other comprehensive income.If Firm D had not chosen to designate the forward commodity contract as a hedge of the cash flows from the inventory,it would not have written down the inventory.The market value of the inventory ($6,200,000)still exceeds Firm D's acquisition cost ($4,500,000).By designating the forward contract as a hedge,it must recognize the decrease in value in its accounts.d. By March 31,2011,inventory has decreased further in value [$800,000 = 20,000 x ($310 - $270)],but the forward contract increases by the same amount.The OCI effects cancel each other out.e. See Part d. above.f. On March 31,2011,the firm settles the forward contract net for $1,000,000 [= 20,000 x ($320 - $270)].g. At sale,the firm recognizes 20,000 x $270 = $5,400,000 in sales revenue and 20,000 x ($225 - $10 - $40)= $3,500,000 in cost of goods sold.The net balance in Other Comprehensive Income related to the inventory and the forward contract is zero.Thus,there is no balance to transfer to earnings at this point.Note that the gross margin on the sale is $1,900,000 (= $5,400,000 - $3,500,000).This is the same gross margin that Firm D would have reported if it had not obtained the forward contract and the market price for the chemical on March 31,2011,had been Firm D's anticipated amount of $320 per gallon ($1,900,000 = $6,400,000 - $4,500,000).The forward contract shifted the risk of changes in the selling price to the counterparty.h. Each of the entries in Parts b.-e.involving other comprehensive income would have been made to income statement accounts instead.i. A justification for treating the forward commodity price contract as a fair value hedge is that the firm wanted to protect the gross margin on the sale of $1,900,000 against commodity price changes.A justification for treating the contract as a cash flow hedge is that the firm wanted to ensure that it received a net cash inflow of $6,400,000 on the sale of the chemical. accounting for Forward Commodity Price Contract as a Cash Flow Hedge December 31,2010 Revaluation Forward Contract 200,000 OCI-Forward Commodity Contract 200,000 OCI-Forward Commodity Contract 200,000 Inventory 200,000 March 31,2011 Revaluation Forward Contract 800,000 OCI-Forward Commodity Contract 800,000 OCI-Forward Commodity Contract 800,000 Inventory 800,000 Closing of Forward Contract and Sale of Inventory Cash 1,000,000 Forward Contract 1,000,000 Cash 5,400,000 Sales Revenue 5,400,000 Cost of Goods Sold 3,500,000 Inventory 3,500,000](https://storage.examlex.com/TB2093/11ea427f_2408_af6e_8d65_7593a2e0c4a5_TB2093_00.jpg)

Cash 5,400,000

Sales Revenue 5,400,000

Cost of Goods Sold 3,500,000

Inventory 3,500,000

Although LIFO generally provides higher quality earnings measures,FIFO generally provides higher _____________________________________________ measures.

Under U.S.GAAP,application of the LIFO and FIFO inventory methods result in differences in the balance sheet,income statement and cash flow statement.Compare and contrast the effect of the two methods on each financial statement and determine the advantages and disadvantages of each method.

When input prices are increasing,companies that use the LIFO method of accounting for inventory will report

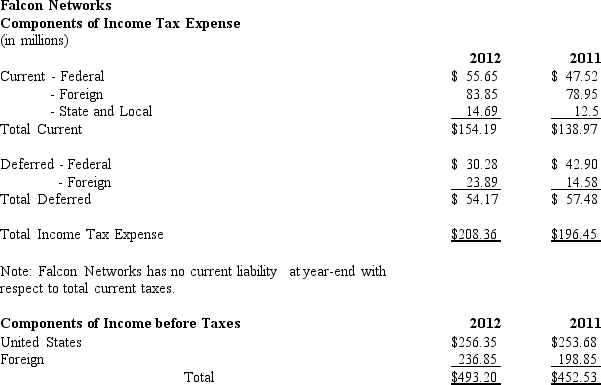

Falcon Networks

Falcon Networks is a leading semiconductor company with operations in 17 different countries. Information about the company's taxes appears below:

-Using the information provided by Falcon Networks determine the foreign effective tax rate for 2012.

-Using the information provided by Falcon Networks determine the foreign effective tax rate for 2012.

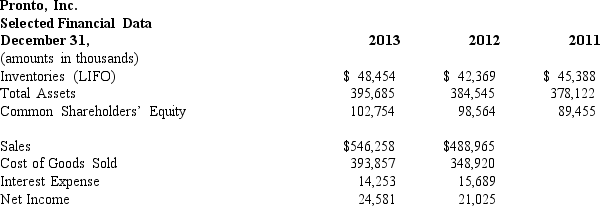

Pronto,Inc.is a major producer of printing equipment.Pronto uses a LIFO cost-flow assumption for inventories.The company's tax rate is 35%.Below is selected financial data for the company.

Required:a.The excess of FIFO over LIFO inventories was $25 million on December 31,2013,$28.5 million on December 31,2012 and $22 million on December 31,2011.Compute the cost of goods sold for Pronto,Inc.for years 2013 and 2012 assuming that it had used a FIFO assumption.

b.Compute the inventory turnover ratio for Pronto,Inc.for years 2013 and 2012 using a LIFO cost-flow assumption.

c.Compute the inventory turnover ratio for Pronto,Inc.for years 2013 and 2012 using a FIFO cost-flow assumption.

d.Compute the rate of return on assets for years 2013 and 2012 based on the reported amounts.Disaggregate ROA into profit margin and asset turnover components.

e.Compute the rate of return on assets for years 2013 and 2012 assuming that Pronto,Inc.had used the FIFO method of accounting for inventories.Disaggregate ROA into profit margin and asset turnover components.

Required:a.The excess of FIFO over LIFO inventories was $25 million on December 31,2013,$28.5 million on December 31,2012 and $22 million on December 31,2011.Compute the cost of goods sold for Pronto,Inc.for years 2013 and 2012 assuming that it had used a FIFO assumption.

b.Compute the inventory turnover ratio for Pronto,Inc.for years 2013 and 2012 using a LIFO cost-flow assumption.

c.Compute the inventory turnover ratio for Pronto,Inc.for years 2013 and 2012 using a FIFO cost-flow assumption.

d.Compute the rate of return on assets for years 2013 and 2012 based on the reported amounts.Disaggregate ROA into profit margin and asset turnover components.

e.Compute the rate of return on assets for years 2013 and 2012 assuming that Pronto,Inc.had used the FIFO method of accounting for inventories.Disaggregate ROA into profit margin and asset turnover components.

All of the following are most likely to change the FMV of pension plan assets during a given period except:

When cash collectibility is uncertain the ___________________________________ method matches the costs of generating revenues dollar for dollar with cash receipts until the firm recovers all such costs.

Firm A places its order for the equipment on June 30,Year1.It simultaneously signs a forward foreign exchange contract for 20,000 GBP.The forward rate on June 30,Year 1,for settlement on June 30,Year 2,is $1.64 per GBP.Firm A designates the forward foreign exchange contract as a fair value hedge of the firm commitment.

Required: a.U.S.GAAP and IFRS do not require Firm A to record the purchase commitment or the

forward foreign exchange contract on the balance sheet as a liability and an asset on

June 30,Year1.What is the logic for this accounting?

b.On December 31,Year 1,the forward foreign exchange rate for settlement on June

30,Year 2,is $1.73 per GBP.Using the financial statement effects template,show the

financial statement effects of recording the change in the value of the purchase commitment

and the change in the value of the forward contract for Year1.Assume an 8 percent per year interest rate for discounting cash flows to their present values on December 31,Year 1.

c.Show the financial statement effects on June 30,Year 2,of recording the change in the present value of the purchase commitment and the forward foreign exchange contract for the passage of time.

d.On June 30,Year 2,the spot foreign exchange rate is $1.75 per GBP.Show the financial

statement effects of recording the change in the value of the purchase commitment and the change in the value of the forward contract due to changes in the exchange rate during the first six months of Year 2.

e.Show the financial statement effects of the June 30,Year 2,purchase of 20,000 GBP with U.S.dollars and acquisition of the equipment.

f.Show the financial statement effects on June 30,Year 2,to settle the forward foreign

exchange contract.

g.How would the effects in Parts b-f differ if Firm A had chosen to designate the forward

foreign exchange contract as a cash flow hedge instead of a fair value hedge?

h.Suggest a scenario that would justify Firm A treating the forward foreign exchange contract as a fair value hedge and a scenario that would justify the firm treating the

contract as a cash flow hedge.

Deferred tax liabilities result in future tax ____________________ when temporary differences reverse.

Dividing a company's income tax expense by its book income before income taxes provides the company's ___________________________________.

Derivative instruments acquired to hedge exposure to variability in expected future cash are _________________________ hedges.

All of the following are considered by analysts when assessing the quality of accounting except:

Companies that engage in long-term contracts can recognize income using either the _____________________________________________ method or the ________________________________________ method.

U.S.GAAP requires firms to report the assets and liabilities of defined benefit plans _______________________________________________________.

The process of allocating the historical cost of certain assets to the periods of their use in a reasonably systematic manner is referred to as ____________________.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)