Exam 6: Inventory, Accounts Payable, and Long-Term Assets

Aiello Inc. had the following inventory in fiscal 2016. The company uses the LIFO method of accounting for inventory.

Beginning Inventory, January 1, 2016: 130 units @ $15.00

Purchase 200 units @ $18.00

Purchase 50 units @ $13.50

Purchase 110 units @ $15.75

Ending Inventory, December 31, 2016: 120 units

The company's cost of goods sold for fiscal 2016 is:

D

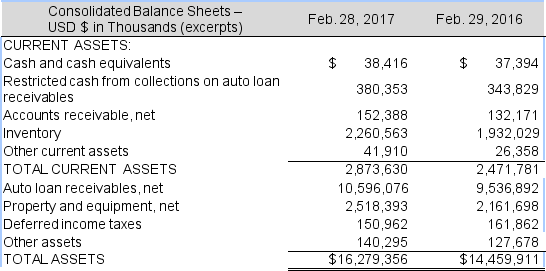

The asset side of the 2017 balance sheet for CarMax Inc. is below.

Continued next page

The footnotes to the annual report include the following:

Inventory is primarily comprised of vehicles held for sale or currently undergoing reconditioning and is stated at the lower of cost or market. Vehicle inventory cost is determined by specific identification. Parts, labor and overhead costs associated with reconditioning vehicles, as well as transportation and other incremental expenses associated with acquiring and reconditioning vehicles, are included in inventory.

Required:

a. Does CarMax use the LIFO or the FIFO method of inventory costing? Explain.

b. Calculate the common-size amount for inventories for both years and comment on any differences that you note. Given that the company is an automotive retailer, does this ratio seem appropriate?

c. At February 28, 2015, Inventory was $2,086,874 thousand. CarMax reports cost of sales of $13,691,824 thousand for the year ended February 28, 2017 and $13,130,915 thousand for the year ended February 29, 2016. Compute inventory turnover and average days inventory outstanding for both years. Do the two ratios tell the same story? Why or why not?

d. CarMax reports revenue of $15,875,118 thousand for the year ended February 28, 2017 and $15,149,675 thousand for the year ended February 29, 2016. Calculate gross profit margins for both years.

e. What is your opinion about the financial health of CarMax? Use the ratios you calculated above to support your opinion.

Continued next page

The footnotes to the annual report include the following:

Inventory is primarily comprised of vehicles held for sale or currently undergoing reconditioning and is stated at the lower of cost or market. Vehicle inventory cost is determined by specific identification. Parts, labor and overhead costs associated with reconditioning vehicles, as well as transportation and other incremental expenses associated with acquiring and reconditioning vehicles, are included in inventory.

Required:

a. Does CarMax use the LIFO or the FIFO method of inventory costing? Explain.

b. Calculate the common-size amount for inventories for both years and comment on any differences that you note. Given that the company is an automotive retailer, does this ratio seem appropriate?

c. At February 28, 2015, Inventory was $2,086,874 thousand. CarMax reports cost of sales of $13,691,824 thousand for the year ended February 28, 2017 and $13,130,915 thousand for the year ended February 29, 2016. Compute inventory turnover and average days inventory outstanding for both years. Do the two ratios tell the same story? Why or why not?

d. CarMax reports revenue of $15,875,118 thousand for the year ended February 28, 2017 and $15,149,675 thousand for the year ended February 29, 2016. Calculate gross profit margins for both years.

e. What is your opinion about the financial health of CarMax? Use the ratios you calculated above to support your opinion.

a. CarMax uses neither the LIFO nor FIFO method of accounting for inventory cost. The company uses the specific identification method. Under this method, the serial number of each vehicle is used to track the vehicles original cost. Any repairs or shipping costs are allocated to the specific vehicle - no averaging is done. When the vehicle is sold, its specific cost is transferred to the income statement as cost of sales.

b. February 2017: $2,260,563 thousand / $16,279,356 thousand = 13.9%

February 2016: $1,932,029 thousand / $14,459,911 thousand = 13.4%

This ratio seems appropriate given that CarMax sells automobiles, which are a high-priced inventory. We may even expect the ratio to be higher, but it is kept at this level due to the large amount of auto loans receivable included in total assets.

c.

Both ratios tell the same story. There was no change in either ratio from 2016 to 2017.

Both ratios tell the same story. There was no change in either ratio from 2016 to 2017.

d.

e. CarMax ratios appear to be stable and includes a slight improvement in its gross profit margin ratio from 2017 to 2016.

e. CarMax ratios appear to be stable and includes a slight improvement in its gross profit margin ratio from 2017 to 2016.

Assume that Barber Co. uses the LIFO inventory costing method for both tax and financial reporting purposes. The balance sheet reports inventories at $297 million. Then, in its footnotes, the company reports that inventories would have been $327 million had the company used the FIFO method.

The difference between these two numbers ($30 million) is referred to as:

A

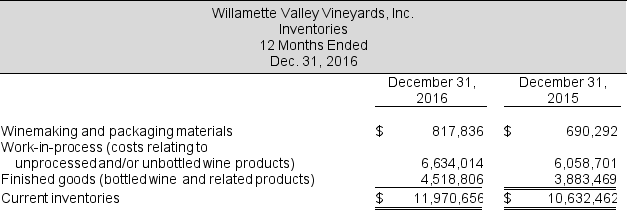

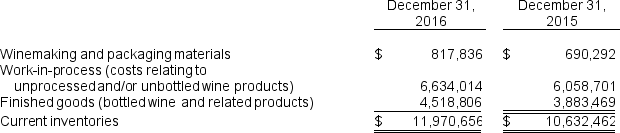

Note 3 to the 2016 financial statements of Willamette Valley Vineyards reports that Inventories consist of the following:

The company reported cost of goods sold of $7,204,884 in 2016 and $7,092,111 in 2015. At December 31, 2014, Total inventories were $ 9,910,570.

Compute average days inventory outstanding for both years. What does this ratio mean? Interpret the ratios.

The company reported cost of goods sold of $7,204,884 in 2016 and $7,092,111 in 2015. At December 31, 2014, Total inventories were $ 9,910,570.

Compute average days inventory outstanding for both years. What does this ratio mean? Interpret the ratios.

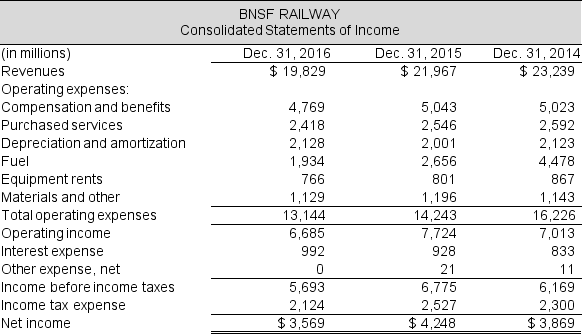

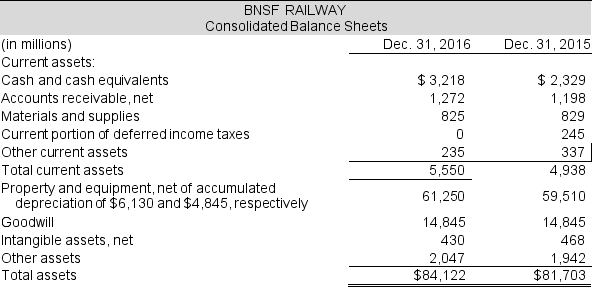

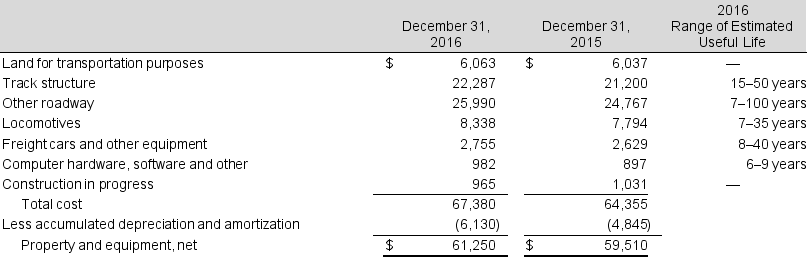

The 2016 income statement and balance sheet (excerpts) for BNSF Railway are below.

Continued next page

The footnotes to the financial statements included the following:

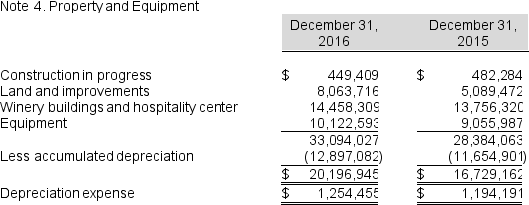

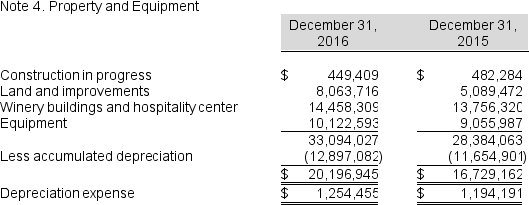

Property and equipment, net (in millions), and the corresponding ranges of estimated useful lives were as follows:

Continued next page

The footnotes to the financial statements included the following:

Property and equipment, net (in millions), and the corresponding ranges of estimated useful lives were as follows:

Required:

a. What proportion of total assets, does BNSF hold as property and equipment in 2016 and 2015? Does this surprise you?

b. Compute property and equipment turnover for 2016 and 2015. Property and equipment, net for 2014 was $55,806 million. Explain this ratio.

c. By what percentage are the assets 'used up' at year-end 2016? What implication does this ratio have for future cash flows at BNSF?

d. Estimate the useful life on average for the BNSF depreciable assets at year-end 2016. Which of the assets listed in the footnote explain this estimated useful life?

Required:

a. What proportion of total assets, does BNSF hold as property and equipment in 2016 and 2015? Does this surprise you?

b. Compute property and equipment turnover for 2016 and 2015. Property and equipment, net for 2014 was $55,806 million. Explain this ratio.

c. By what percentage are the assets 'used up' at year-end 2016? What implication does this ratio have for future cash flows at BNSF?

d. Estimate the useful life on average for the BNSF depreciable assets at year-end 2016. Which of the assets listed in the footnote explain this estimated useful life?

How do companies test assets for impairment? If an asset is impaired, how do companies write them down?

The 2016 financial statements of CVS Health Corporation reported the following information (in millions):

The inventory turnover ratio for 2016 is:

The inventory turnover ratio for 2016 is:

Fey Enterprises recorded a restructuring charge of $16.2 million during fiscal 2016 related entirely to the closing of its division located in Denver, Colorado. The company's financial statement footnotes indicated that expected employee separation payments amounted to $12.6 million and that fixed asset write-downs accounted for the remainder. Nickolas had never before incurred restructuring charges. At the end of the year, the company's balance sheet included a restructuring accrual of $2,700,000.

The cash flow effect of Fey Enterprises' restructuring during fiscal 2016 is:

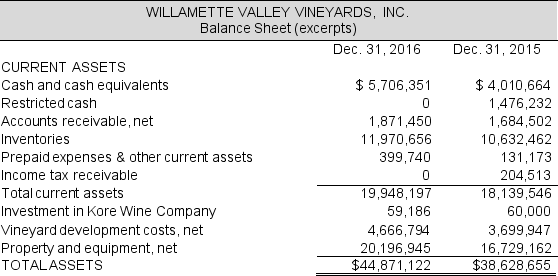

The asset side of the 2016 balance sheet for Willamette Valley Vineyards is as follows:

Continued next page

The following footnotes are from the annual report for Willamette Valley Vineyards for 2016.

Vineyard Development Costs

Vineyard development costs consist primarily of the costs of the vines and expenditures related to labor and materials to prepare the land and construct vine trellises. The costs are capitalized until the vineyard becomes commercially productive, at which time annual amortization is recognized using the straight-line method over the estimated economic useful life of the vineyard, which is estimated to be 30 years. Accumulated amortization of vineyard development costs aggregated $1,185,823 and $1,109,406 at December 31, 2016 and 2015, respectively.

Amortization of vineyard development costs are included in capitalized crop costs that in turn are included in inventory costs and ultimately become a component of cost of goods sold. For the years ending December 31, 2016 and 2015, approximately $76,417 and $75,669, respectively, was amortized into inventory costs.

Continued next page

The following footnotes are from the annual report for Willamette Valley Vineyards for 2016.

Vineyard Development Costs

Vineyard development costs consist primarily of the costs of the vines and expenditures related to labor and materials to prepare the land and construct vine trellises. The costs are capitalized until the vineyard becomes commercially productive, at which time annual amortization is recognized using the straight-line method over the estimated economic useful life of the vineyard, which is estimated to be 30 years. Accumulated amortization of vineyard development costs aggregated $1,185,823 and $1,109,406 at December 31, 2016 and 2015, respectively.

Amortization of vineyard development costs are included in capitalized crop costs that in turn are included in inventory costs and ultimately become a component of cost of goods sold. For the years ending December 31, 2016 and 2015, approximately $76,417 and $75,669, respectively, was amortized into inventory costs.

Required:

a. Explain the difference between Vineyard development costs and Land and improvements.

b. Calculate the percent used up of the Vineyard development costs.

c. Calculate the percent used up of the Property and equipment. What does this imply for future cash flows for Willamette Valley Vineyards?

d. Assume that on January 1, 2017 the company determined that the Vineyard development costs had a fair value of $4,000,000. How would this affect the company's balance sheet and income statement in 2017?

Required:

a. Explain the difference between Vineyard development costs and Land and improvements.

b. Calculate the percent used up of the Vineyard development costs.

c. Calculate the percent used up of the Property and equipment. What does this imply for future cash flows for Willamette Valley Vineyards?

d. Assume that on January 1, 2017 the company determined that the Vineyard development costs had a fair value of $4,000,000. How would this affect the company's balance sheet and income statement in 2017?

Employee severance costs, as part of board-approved restructuring plans, are reported in the income statement even if the actual payment for these costs occurs in subsequent periods.

In order to estimate depreciation expense using the double-declining-balance method, managers must estimate the asset's useful life and its salvage value.

Firms typically report three categories of restructuring costs. What are they and how do they affect the balance sheet and the income statement?

Hauser Corporation has the following metrics for 2016.

The cash conversion cycle for 2016 is:

The cash conversion cycle for 2016 is:

Abercrombie & Fitch has inventory levels of $399,795 thousand and $436,701 thousand at the end of fiscal-year ending 2016 and 2015 respectively. Cost of goods sold for 2016 is $1,298,172 thousand.

a. Calculate the inventory turnover ratio and the average days inventory outstanding for 2016.

b. Suggest three ways that Abercrombie & Fitch might improve inventory turnover.

Everett Company uses the average cost method to account for inventory and has the following activity during the month of March 2017.

During March, Everett sold 850 units.

Compute the cost of goods sold for March and the ending inventory balance at March 31, 2017.

During March, Everett sold 850 units.

Compute the cost of goods sold for March and the ending inventory balance at March 31, 2017.

The January 28, 2017 (fiscal year 2016) financial statements of Caleres, Inc. reported the following information (in thousands):

The footnotes to the 2016 financial statements of Skechers U.S.A., Inc., a competitor of Caleres, Inc., reported that the company uses the FIFO method of accounting for inventories. Financial statements reported the following (in thousands):

The footnotes to the 2016 financial statements of Skechers U.S.A., Inc., a competitor of Caleres, Inc., reported that the company uses the FIFO method of accounting for inventories. Financial statements reported the following (in thousands):

Compare the two companies' days-inventory-outstanding ratios for 2016. To do this properly, you will need to convert the companies' cost of sales and inventories to a common inventory costing method. Which company is more efficient with its inventory?

Compare the two companies' days-inventory-outstanding ratios for 2016. To do this properly, you will need to convert the companies' cost of sales and inventories to a common inventory costing method. Which company is more efficient with its inventory?

The Dow Chemical Corporation announced a restructuring plan in 2016 which incorporated actions related to the recent ownership restructure of Dow Corning Corporation. The following footnote (excerpted) of the Company comes from the December 31, 2016 financial statements:

2016 Restructuring

On June 27, 2016, the Board of Directors of the Company approved a restructuring plan that incorporates actions related to the recent ownership restructure of Dow Corning Corporation ("Dow Corning"). These actions, aligned with Dow's value growth and synergy targets, will result in a global workforce reduction of approximately 2,500 positions, with most of these positions resulting from synergies related to the Dow Corning transaction. These actions are expected to be substantially completed by June 30, 2018.

As a result of these actions, the Company recorded pretax restructuring charges of $449 million in the second quarter of 2016 consisting of severance charges of $268 million, asset write-downs and write-offs of $153 million and costs associated with exit and disposal activities of $28 million. The impact of these charges is shown as "Restructuring charges (credits)"

in the consolidated statements of income and reflected in the Company's segment results in the table that follows. The table also summarizes the activities related to the Company's 2016 restructuring reserve, which is included in "Accrued and other current liabilities"

and "Other noncurrent obligations"

in the consolidated balance sheets.

The following table summarizes the activities related to the Company's restructuring reserve (liability):

Continued next page

Required:

a. Explain why Dow Chemical planned this restructuring. When did the company record the restructuring expense? When will the restructuring take place? Explain the difference.

b. What are the three types of restructuring costs for Dow Chemical for 2016?

c. Explain why no cash is involved in settling the impairment of long-lived assets portion of the restructuring reserve.

d. Dow Chemical managers estimated all of the charges above. What would be the income-statement consequences next year (in 2017) if only $100 million of additional cash payments were necessary to completely settle the employee severance costs? Assume that Dow Chemical did not intentionally overestimate these severance costs.

Continued next page

Required:

a. Explain why Dow Chemical planned this restructuring. When did the company record the restructuring expense? When will the restructuring take place? Explain the difference.

b. What are the three types of restructuring costs for Dow Chemical for 2016?

c. Explain why no cash is involved in settling the impairment of long-lived assets portion of the restructuring reserve.

d. Dow Chemical managers estimated all of the charges above. What would be the income-statement consequences next year (in 2017) if only $100 million of additional cash payments were necessary to completely settle the employee severance costs? Assume that Dow Chemical did not intentionally overestimate these severance costs.

In general, in a period of falling prices, LIFO produces higher gross profits than FIFO.

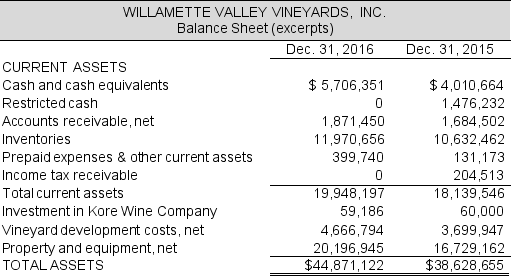

The asset side of the 2016 balance sheet for Willamette Valley Vineyards is below. The company reported cost of goods sold of $7,204,884 in 2016 and $7,092,111 in 2015. Use this information to answer the requirements.

Note 3 to the financial statement reports that Inventories consist of:

Note 3 to the financial statement reports that Inventories consist of:

Continued next page

Required:

a. Explain in layman's terms what each of the three types of inventories comprises.

b. Compute average days inventory outstanding for both years and interpret any change. At December 31, 2014, Total inventories, net, were $ 9,910,570. What does this ratio mean? Is the year-over-year change good news?

c. It is typical in the winemaking industry for wine to stay in "process" for more than a year. How is such inventory classified in Willamette's balance sheet?

Continued next page

Required:

a. Explain in layman's terms what each of the three types of inventories comprises.

b. Compute average days inventory outstanding for both years and interpret any change. At December 31, 2014, Total inventories, net, were $ 9,910,570. What does this ratio mean? Is the year-over-year change good news?

c. It is typical in the winemaking industry for wine to stay in "process" for more than a year. How is such inventory classified in Willamette's balance sheet?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)