Exam 11: Profit Maximisation Under Perfect Competition and Monopoly

Exam 1: The Business Environment and Business Economics44 Questions

Exam 2: Economics and the World of Business48 Questions

Exam 3: Business Organisations50 Questions

Exam 4: The Working of Competitive Markets77 Questions

Exam 5: Business in a Market Environment69 Questions

Exam 6: Demand and the Consumer61 Questions

Exam 7: Demand and the Firm48 Questions

Exam 8: Products, Marketing and Advertising40 Questions

Exam 9: Costs of Production60 Questions

Exam 10: Revenue and Profit43 Questions

Exam 11: Profit Maximisation Under Perfect Competition and Monopoly47 Questions

Exam 12: Profit Maximisation Under Imperfect Competition62 Questions

Exam 13: An Introduction to Business Strategy69 Questions

Exam 14: Alternative Theories of the Firm48 Questions

Exam 15: Growth Strategy63 Questions

Exam 16: The Small-Firm Sector51 Questions

Exam 17: Pricing Strategy50 Questions

Exam 18: Labour Markets, Wages and Industrial Relations85 Questions

Exam 19: Investment and the Employment of Capital55 Questions

Exam 20: Reasons for Government Intervention in the Market89 Questions

Exam 21: Government and the Firm90 Questions

Exam 22: Government and the Market133 Questions

Exam 23: Globalisation and Multinational Business74 Questions

Exam 24: International Trade54 Questions

Exam 25: Trading Blocs56 Questions

Exam 26: The Macroeconomic Environment of Business160 Questions

Exam 27: The Balance of Payments and Exchange Rates107 Questions

Exam 28: Banking, Money and Interest Rates128 Questions

Exam 29: Business Activity, Employment and Inflation197 Questions

Exam 30: Demand-Side Policy123 Questions

Exam 31: Supply-Side Policy64 Questions

Exam 32: International Economic Policy67 Questions

Select questions type

Perfect competition exists in an industry that contains many relatively small firms producing identical products with profit- maximising prices equal to the respective marginal costs of products.

(True/False)

4.9/5  (34)

(34)

For a firm to be a natural monopoly, economies of scale must be realised at a scale that is close to total demand in the market.

(True/False)

4.9/5 (36)

A firm in long- run equilibrium is also in short- run equilibrium.

(True/False)

4.8/5 (32)

Concentration ratios are a good guide to the degree of competition when an industry competes with overseas suppliers.

(True/False)

4.7/5 (47)

What is the connection between perfect competition and the public interest?

(Essay)

4.9/5 (28)

The efficient regulatory solution for a natural monopoly is to set price equal to average cost and allow the monopolist to earn a normal return.

(True/False)

4.9/5 (30)

Under contestable theory, it is not the number of firms that is the most important factor.

(True/False)

4.8/5 (40)

Why is perfect competition incompatible with achieving substantial economies of scale?

(Essay)

4.8/5 (32)

Which of the following statements does not refer to a characteristic of a perfectly competitive industry?

(Multiple Choice)

4.7/5 (30)

Under perfect competition, super profits are competed away in the long run because

(Multiple Choice)

4.9/5 (36)

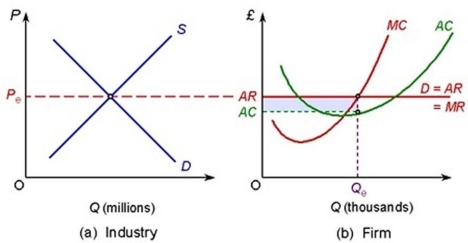

The following diagram shows a perfectly competitive industry and firm.

The position shown is not a long- run equilibrium because

The position shown is not a long- run equilibrium because

(Multiple Choice)

4.8/5 (38)

Assume the wool industry is a perfectly competitive industry. Why is it difficult for a wool producer to make excess profits as implied by the assumptions of perfect competition?

(Essay)

4.9/5 (35)

For a natural monopolist, fixed costs are very , while marginal costs are relatively

(Multiple Choice)

4.7/5 (39)

Which of the following is least likely to be considered a firm in an imperfectly competitive industry?

(Multiple Choice)

4.7/5 (30)

Monopolies may become inefficient without competitive pressure resulting in higher costs. This is sometimes called

(Multiple Choice)

5.0/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)