Exam 11: Profit Maximisation Under Perfect Competition and Monopoly

Exam 1: The Business Environment and Business Economics44 Questions

Exam 2: Economics and the World of Business48 Questions

Exam 3: Business Organisations50 Questions

Exam 4: The Working of Competitive Markets77 Questions

Exam 5: Business in a Market Environment69 Questions

Exam 6: Demand and the Consumer61 Questions

Exam 7: Demand and the Firm48 Questions

Exam 8: Products, Marketing and Advertising40 Questions

Exam 9: Costs of Production60 Questions

Exam 10: Revenue and Profit43 Questions

Exam 11: Profit Maximisation Under Perfect Competition and Monopoly47 Questions

Exam 12: Profit Maximisation Under Imperfect Competition62 Questions

Exam 13: An Introduction to Business Strategy69 Questions

Exam 14: Alternative Theories of the Firm48 Questions

Exam 15: Growth Strategy63 Questions

Exam 16: The Small-Firm Sector51 Questions

Exam 17: Pricing Strategy50 Questions

Exam 18: Labour Markets, Wages and Industrial Relations85 Questions

Exam 19: Investment and the Employment of Capital55 Questions

Exam 20: Reasons for Government Intervention in the Market89 Questions

Exam 21: Government and the Firm90 Questions

Exam 22: Government and the Market133 Questions

Exam 23: Globalisation and Multinational Business74 Questions

Exam 24: International Trade54 Questions

Exam 25: Trading Blocs56 Questions

Exam 26: The Macroeconomic Environment of Business160 Questions

Exam 27: The Balance of Payments and Exchange Rates107 Questions

Exam 28: Banking, Money and Interest Rates128 Questions

Exam 29: Business Activity, Employment and Inflation197 Questions

Exam 30: Demand-Side Policy123 Questions

Exam 31: Supply-Side Policy64 Questions

Exam 32: International Economic Policy67 Questions

Select questions type

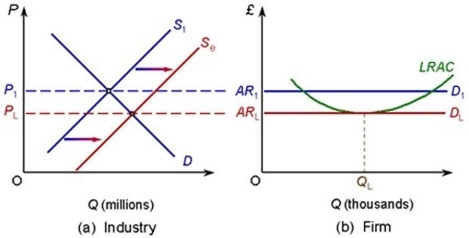

The following diagram shows a perfectly competitive industry and firm. Initial supernormal profits have attracted new firms into the industry.

QL represents long- run equilibrium output of the firm because

QL represents long- run equilibrium output of the firm because

(Multiple Choice)

4.8/5  (31)

(31)

If a firm experiences lower average costs of production as a consequence of producing a range of products, the firm is experiencing

(Multiple Choice)

4.9/5 (30)

The type of product sold is a key difference between a perfectly competitive industry and a monopolistically competitive industry.

(True/False)

4.9/5 (33)

In a contestable market, the threat of competition will be greater the lower the entry costs to the industry.

(True/False)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)