Exam 28: Partnership Dissolution and Conversion to Company Status

Exam 1: Entities and Financial Reporting Standards16 Questions

Exam 2: International Accounting: Institutional Framework and Standards16 Questions

Exam 3: The Nature and Objectives of Financial Accounting16 Questions

Exam 4: Accounting Principles, Concepts and Policies16 Questions

Exam 5: The Conceptual Framework of Accounting16 Questions

Exam 6: Auditing, Corporate Governance and Ethics16 Questions

Exam 7: The Accounting Equation and Its Components16 Questions

Exam 8: Basic Documentation and Books of Accounts16 Questions

Exam 9: The General Ledger16 Questions

Exam 10: The Balancing of Accounts and the Trial Balance16 Questions

Exam 11: Day Books and the Journal16 Questions

Exam 12: The Cash Book16 Questions

Exam 13: The Petty Cash Book6 Questions

Exam 14: The Final Financial Statements of Sole Traders20 Questions

Exam 15: Depreciation and Non-Current Assets20 Questions

Exam 16: Bad Debts and Provisions for Bad Debts16 Questions

Exam 17: Accruals and Prepayments20 Questions

Exam 18: The Preparation of Final Financial Statements From the Trial Balance6 Questions

Exam 19: The Bank Reconciliation Statement17 Questions

Exam 20: Control Accounts16 Questions

Exam 21: Errors and Suspense Accounts16 Questions

Exam 22: Single Entry and Incomplete Records16 Questions

Exam 23: Inventory Valuation16 Questions

Exam 24: Financial Statements for Manufacturing Entities16 Questions

Exam 25: The Final Financial Statements of Clubs16 Questions

Exam 26: The Final Financial Statements of Partnerships16 Questions

Exam 27: Changes in Partnerships16 Questions

Exam 28: Partnership Dissolution and Conversion to Company Status14 Questions

Exam 29: The Nature of Limited Companies and Their Capital16 Questions

Exam 30: The Final Financial Statements of Limited Companies14 Questions

Exam 31: Statement of Cash Flows16 Questions

Exam 32: The Appraisal of Company Financial Statements Using Ratio Analysis20 Questions

Select questions type

In a partnership the double entry to record initial realisation expenses not paid is as follows:

Free

(Multiple Choice)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

C

After receipt of all monies on the dissolution of the partnership the realisation account has a debit

Balance carried down of £8,000. Assuming there are two partners X and Y, sharing the profits and

Losses equally.

What is the double entry to clear the revaluation account?

Free

(Multiple Choice)

4.8/5 (34)

Correct Answer:Verified

B

When there is a credit balance brought down on the realisation account, this means that:

Free

(Multiple Choice)

4.8/5 (42)

Correct Answer:Verified

B

A partnership has reported profit for the year of £258,000 per the income statement. The partners had expected to make £300,000 so are not pleased with performance. The partnership has three partners (Simon, Mary and Anna). It is estimated that these partners would have earned the following amounts (Simon £90,000, Mary £80,000, Anna £65,000) had they been working elsewhere. The balance on Simon's capital account is £400,000, Mary's balance is £200,000 and Anna's is £300,000. The current rate of interest being earned on government gilts is 10%.

Given this information, what is the partnership abnormal profit/ (loss) for the year?

(Multiple Choice)

4.8/5 (34)

What is the main purpose of a purchase of consideration account?

(Multiple Choice)

4.8/5 (35)

When there is a credit balance carried down on the realisation account, this means that:

(Multiple Choice)

4.8/5 (37)

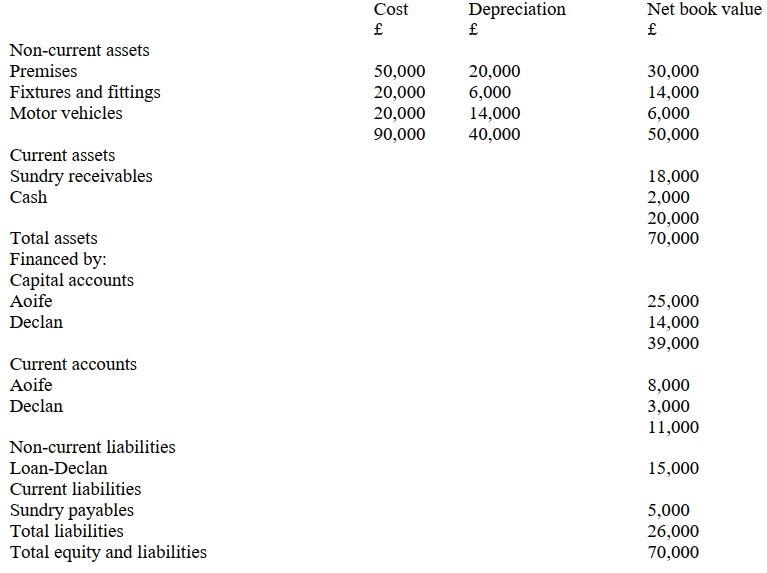

The partners decide to dissolve the partnership. They are offered £40,000 for the building and the fixtures

and fittings. Aoife agrees to take over one car at a value of £2,500 and Declan takes over the other

remaining car at a value of £2,000. It turns out that £2,500 of the trade receivable are bad and the sundry

payables have promised to give the partners, on average 10% discount on settlement of the debt owed to

them if it is paid for on the 1 January 20X2. The loan will be paid off in full on that date. All the monies

in and out will occur on the 1 January 20X2. The dissolution expenses amount to £2,200.

Questions 1 to 4 should be answered from this following information

Aoife and Declan are in partnership, sharing profits equally. Their draft statement of financial position is

as follows:

-What is the profit/ (loss) on realisation in the books of the partnership?

-What is the profit/ (loss) on realisation in the books of the partnership?

(Multiple Choice)

5.0/5 (40)

The partners decide to dissolve the partnership. They are offered £40,000 for the building and the fixtures

and fittings. Aoife agrees to take over one car at a value of £2,500 and Declan takes over the other

remaining car at a value of £2,000. It turns out that £2,500 of the trade receivable are bad and the sundry

payables have promised to give the partners, on average 10% discount on settlement of the debt owed to

them if it is paid for on the 1 January 20X2. The loan will be paid off in full on that date. All the monies

in and out will occur on the 1 January 20X2. The dissolution expenses amount to £2,200.

Questions 1 to 4 should be answered from this following information

Aoife and Declan are in partnership, sharing profits equally. Their draft statement of financial position is

as follows:

-What payment/receipt from/to Aoife is required to close her capital account on the dissolution of the partnership?

(Multiple Choice)

4.9/5 (43)

The partners decide to dissolve the partnership. They are offered £40,000 for the building and the fixtures

and fittings. Aoife agrees to take over one car at a value of £2,500 and Declan takes over the other

remaining car at a value of £2,000. It turns out that £2,500 of the trade receivable are bad and the sundry

payables have promised to give the partners, on average 10% discount on settlement of the debt owed to

them if it is paid for on the 1 January 20X2. The loan will be paid off in full on that date. All the monies

in and out will occur on the 1 January 20X2. The dissolution expenses amount to £2,200.

Questions 1 to 4 should be answered from this following information

Aoife and Declan are in partnership, sharing profits equally. Their draft statement of financial position is

as follows:

-What is the balance on the bank account, before the partners settle their capital account balances assuming all other transactions involving the bank have taken place?

(Multiple Choice)

4.8/5 (33)

In a company's statement of financial position goodwill is classed as:

(Multiple Choice)

4.9/5 (38)

The partnership is being dissolved and converted into a company. The realisation account after all the

Assets and liabilities were adjusted to their fair value and the consideration posted has a credit balance

Carried down of £10,000. Assuming there are two partners X and Y, sharing the profits and losses

Equally.

What is the double entry to clear the realisation account?

(Multiple Choice)

4.8/5 (41)

In the books of the partnership, how is the consideration received for the partnership treated.

What is the double entry?

(Multiple Choice)

4.7/5 (37)

In a partnership the double entry to record realisation expenses paid is as follows:

(Multiple Choice)

4.7/5 (43)

The partners decide to dissolve the partnership. They are offered £40,000 for the building and the fixtures

and fittings. Aoife agrees to take over one car at a value of £2,500 and Declan takes over the other

remaining car at a value of £2,000. It turns out that £2,500 of the trade receivable are bad and the sundry

payables have promised to give the partners, on average 10% discount on settlement of the debt owed to

them if it is paid for on the 1 January 20X2. The loan will be paid off in full on that date. All the monies

in and out will occur on the 1 January 20X2. The dissolution expenses amount to £2,200.

Questions 1 to 4 should be answered from this following information

Aoife and Declan are in partnership, sharing profits equally. Their draft statement of financial position is

as follows:

-What payment/receipt from/to Declan is required to close his capital account on the dissolution of the partnership?

(Multiple Choice)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)