Exam 11: Intangible Assets

Exam 1: Financial Accounting and Accounting Standards20 Questions

Exam 2: Conceptual Framework Underlying Financial Accounting35 Questions

Exam 3: The Accounting Information System34 Questions

Exam 4: Balance Sheet32 Questions

Exam 5: Income Statement and Related Information50 Questions

Exam 6: Statement of Cash Flows49 Questions

Exam 7: Revenue Recognition52 Questions

Exam 8: Cash and Receivables58 Questions

Exam 9: Accounting for Inventories51 Questions

Exam 10: Accounting for Property, Plant, and Equipment64 Questions

Exam 11: Intangible Assets48 Questions

Exam 12: Accounting for Liabilities63 Questions

Exam 13: Stockholders Equity74 Questions

Exam 14: Investments48 Questions

Exam 15: Accounting for Income Taxes69 Questions

Exam 16: Accounting for Compensation42 Questions

Exam 17: Accounting for Leases59 Questions

Exam 18: Additional Reporting Issues70 Questions

Exam 19: Appendix A: Accounting and the Time Value of Money31 Questions

Exam 20: Appendix B: Reporting Cash Flows18 Questions

Exam 21: Appendix D: Retail Inventory Method6 Questions

Exam 22: Appendix E: Accounting for Natural Resources6 Questions

Exam 23: Appendix G: Accounting for Troubled Debt3 Questions

Exam 24: Appendix H: Accounting for Derivative Instruments1 Questions

Exam 25: Appendix I: Error Analysis6 Questions

Select questions type

In January, 2003, Findley Corporation purchased a patent for a new consumer product for $720,000. At the time of purchase, the patent was valid for fifteen years. Due to the competitive nature of the product, however, the patent was estimated to have a useful life of only ten years. During 2008, the product was permanently removed from the market under governmental order because of a potential health hazard present in the product. What amount should Findley charge to expense during 2008, assuming amortization is recorded at the end of each year?

(Multiple Choice)

4.7/5  (36)

(36)

As a result of FASB Statement No. 2, all research and development (R & D) costs should normally be charged to expense when incurred.

(True/False)

4.9/5 (34)

A large publicly held company has developed and registered a trademark during 2008. How should the cost of developing and registering the trademark be accounted for if it is considered to have a limited life?

(Multiple Choice)

4.9/5 (36)

Intangible assets are amortized over their useful lives unless the intangible can remain in existence indefinitely.

(True/False)

4.8/5 (34)

Twilight Corporation acquired End-of-the-World Products on January 1, 2008 for $2,000,000, and recorded goodwill of $375,000 as a result of that purchase. At December 31, 2008, the End-of-the-World Products Division had a fair value of $1,700,000. The net identifiable assets of the Division (excluding goodwill) had a fair value of $1,450,000 at that time. What amount of loss on impairment of goodwill should Twilight record in 2008?

(Multiple Choice)

5.0/5 (34)

During 2008, Bond Company purchased the net assets of May Corporation for $950,000. On the date of the transaction, May had $300,000 of liabilities. The fair value of May's assets when acquired were as follows:

How should the $550,000 difference between the fair value of the net assets acquired ($1,500,000) and the cost ($950,000) be accounted for by Bond?

How should the $550,000 difference between the fair value of the net assets acquired ($1,500,000) and the cost ($950,000) be accounted for by Bond?

(Multiple Choice)

4.9/5 (30)

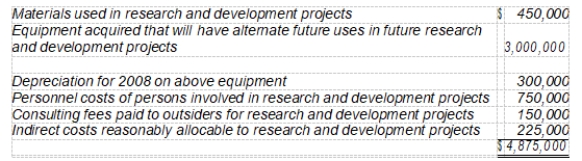

Hall Co. incurred research and development costs in 2008 as follows:

The amount of research and development costs charged to Hall's 2008 income statement should be

The amount of research and development costs charged to Hall's 2008 income statement should be

(Multiple Choice)

4.7/5 (36)

If a company constructs a laboratory building to be used as a research and development facility, the cost of the laboratory building is matched against earnings as

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)