Exam 11: Intangible Assets

Exam 1: Financial Accounting and Accounting Standards20 Questions

Exam 2: Conceptual Framework Underlying Financial Accounting35 Questions

Exam 3: The Accounting Information System34 Questions

Exam 4: Balance Sheet32 Questions

Exam 5: Income Statement and Related Information50 Questions

Exam 6: Statement of Cash Flows49 Questions

Exam 7: Revenue Recognition52 Questions

Exam 8: Cash and Receivables58 Questions

Exam 9: Accounting for Inventories51 Questions

Exam 10: Accounting for Property, Plant, and Equipment64 Questions

Exam 11: Intangible Assets48 Questions

Exam 12: Accounting for Liabilities63 Questions

Exam 13: Stockholders Equity74 Questions

Exam 14: Investments48 Questions

Exam 15: Accounting for Income Taxes69 Questions

Exam 16: Accounting for Compensation42 Questions

Exam 17: Accounting for Leases59 Questions

Exam 18: Additional Reporting Issues70 Questions

Exam 19: Appendix A: Accounting and the Time Value of Money31 Questions

Exam 20: Appendix B: Reporting Cash Flows18 Questions

Exam 21: Appendix D: Retail Inventory Method6 Questions

Exam 22: Appendix E: Accounting for Natural Resources6 Questions

Exam 23: Appendix G: Accounting for Troubled Debt3 Questions

Exam 24: Appendix H: Accounting for Derivative Instruments1 Questions

Exam 25: Appendix I: Error Analysis6 Questions

Select questions type

A trademark may properly be considered to have an indefinite life.

(True/False)

4.9/5  (39)

(39)

Acceptable accounting practice requires that disclosure be made in the financial statements of the total R & D costs charged to expense each period for which an income statement is presented.

(True/False)

4.8/5 (36)

Calvin Company incurred the following costs related to the start-up of the business:

The company wishes to amortize these costs over the maximum period allowed under generally accepted accounting principles. Assuming that Calvin Company began operation on January 1, 2008, what amount of the start-up costs should be amortized in 2009?

The company wishes to amortize these costs over the maximum period allowed under generally accepted accounting principles. Assuming that Calvin Company began operation on January 1, 2008, what amount of the start-up costs should be amortized in 2009?

(Multiple Choice)

4.9/5 (41)

Isa Company has equipment that, due to changes in use, is reviewed for possible impairment. The asset's carrying amount is $400,000 ($500,000 cost less $100,000 accumulated depreciation). The expected future net cash flows (undiscounted) from the use of the asset and its eventual disposition are determined to be $380,000 and it has a current market value of $350,000. What is the amount of the impairment, if any, that should be recorded by Isa Company?

(Multiple Choice)

4.7/5 (32)

Use of the master valuation approach to measure goodwill requires an estimate of a firm's excess earning power.

(True/False)

4.8/5 (38)

On June 30, 2008, Cey, Inc. exchanged 2,000 shares of Seely Corp. $30 par value common stock for a patent owned by Gore Co. The Seely stock was acquired in 2008 at a cost of $55,000. At the exchange date, Seely common stock had a fair value of $45 per share, and the patent had a net carrying value of $110,000 on Gore's books. Cey should record the patent at

(Multiple Choice)

5.0/5 (36)

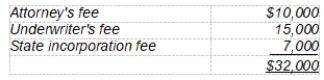

Which of the following legal fees should be capitalized?

Legal fees to Legal fees to successfully obtain a copyright defend a trademark

(Multiple Choice)

4.8/5 (34)

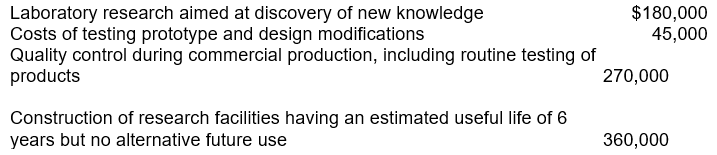

MaBelle Corporation incurred the following costs in 2008:  What amount should MaBelle record as research & development expense in 2008?

What amount should MaBelle record as research & development expense in 2008?

(Multiple Choice)

5.0/5 (38)

Mining Company acquired a patent on an oil extraction technique on January 1, 2007 for $5,000,000. It was expected to have a 10 year life and no residual value. Mining uses straight-line amortization for patents. On December 31, 2008, the expected future cash flows expected from the patent were expected to be $600,000 per year for the next eight years. The present value of these cash flows, discounted at Mining's market interest rate, is $2,800,000. At what amount should the patent be carried on the December 31, 2008 balance sheet?

(Multiple Choice)

4.8/5 (36)

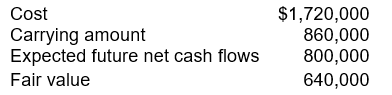

The following information is available for Barkley Company's patents:  Barkley would record a loss on impairment of

Barkley would record a loss on impairment of

(Multiple Choice)

4.9/5 (37)

Distributor Company purchases Supplier Company for $800,000 cash on January 1, 2009. The book value of Supplier Company's net assets, as reflected on its December 31, 2008 balance sheet is $620,000. An analysis by Distributor on December 31, 2008 indicates that the fair value of Supplier's tangible assets exceeded the book value by $60,000, and the fair value of identifiable intangible assets exceeded book value by $45,000. How much goodwill should be recognized by Distributor Company when recording the purchase of Supplier Company?

(Multiple Choice)

4.9/5 (36)

Wildcat Baseball Company had a player contract with Carter that was recorded in its accounting records at $5,800,000. Aggie Baseball Company had a player contract with Jeter that was recorded in its accounting records at $5,600,000. Wildcat traded Carter to Aggie for Jeter by exchanging each player's contract. The fair value of each contract was $6,000,000. What amount should be shown in the accounting records after the exchange of player contracts?

Wildcat Aggie

(Multiple Choice)

4.7/5 (41)

The cost of purchasing patent rights for a product that might otherwise have seriously competed with one of the purchaser's patented products should be

(Multiple Choice)

5.0/5 (35)

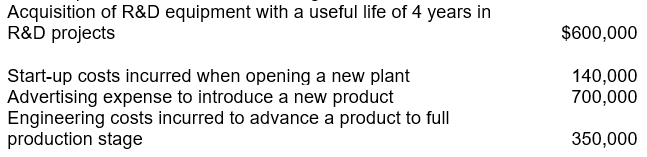

Martin Inc. incurred the following costs during the year ended December 31, 2008:  The total amount to be classified and expensed as research and development in 2008 is

The total amount to be classified and expensed as research and development in 2008 is

(Multiple Choice)

4.8/5 (35)

Hooker Corporation acquired a franchise to operate a Good Pet Dog Kennel in January, 2003. The cost of the franchise was $125,000 and was estimated to have a limited life of 40 years. Early in the year 2009, the franchise was deemed worthless due to significant law suits that caused the franchisor to go out of business. What amount of cost or expense should be charged to the income statement of Hooker Corporation for the years noted below?

2003 2009

(Multiple Choice)

4.8/5 (30)

Goodwill is often identified on the balance sheet as the excess of the fair value over the cost of the net assets acquired.

(True/False)

4.8/5 (46)

The costs of services performed by others in connection with the reporting company's R & D should be expensed as incurred.

(True/False)

4.9/5 (29)

When the fair market value of the assets acquired in a business purchase exceed the purchase price, negative goodwill (also called badwill) arises. When negative goodwill arises, GAAP requires that it be allocated to

(Multiple Choice)

4.9/5 (33)

Lack of physical substance is the only characteristic of intangible assets that distinguishes them from all other assets reported on the balance sheet.

(True/False)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)