Exam 21: Transfer Pricing and Multinational Management Control Systems

Exam 1: The Accountants Vital Role in Decision Making33 Questions

Exam 2: An Introduction to Cost Terms and Purposes60 Questions

Exam 3: Cost-Volume-Profit Analysis41 Questions

Exam 4: Job Costing49 Questions

Exam 5: Activity-Based Costing and Management40 Questions

Exam 6: Master Budget and Responsibility Accounting50 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I47 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II35 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation52 Questions

Exam 10: Analysis of Cost Behaviour80 Questions

Exam 11: Decision Making and Relevant Information54 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management36 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis43 Questions

Exam 14: Period Cost Allocation38 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts57 Questions

Exam 16: Revenue and Customer Profitability Analysis29 Questions

Exam 17: Process Costing50 Questions

Exam 18: Spoilage, Rework, and Scrap62 Questions

Exam 19: Inventory Cost Management Strategies46 Questions

Exam 20: Capital Budgeting: Methods of Investment Analysis42 Questions

Exam 21: Transfer Pricing and Multinational Management Control Systems45 Questions

Exam 22: Multinational Performance Measurement and Compensation62 Questions

Select questions type

Alsation Ltd. has two divisions:. The Machining Division prepares the raw materials into component parts, and the Assembly Division assembles the components into finished product. No inventories exist in either division at the beginning of the year. During the year the Machining Division prepared 80,000 square metres of sheet metal at a cost of $480,000. All production was transferred to the Assembly Division where the metal was converted into 80,000 units of finished product at an additional costs of $5 per unit. The 80,000 units were sold for $2,000,000.

Required:

a. Determine the operating income for each division if the transfer price from Machining to Assembly is at cost.

b. Determine the operating income for each division if the transfer price is $5/square metre.

c. Since the Machining Division has all of its sales internally to the Assembly Division, does the manager care what price is selected? Why? Should the Machining Division be a cost centre or a profit centre under the circumstances?

(Essay)

4.8/5  (42)

(42)

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Have few interdependencies among divisions.

(Multiple Choice)

4.8/5 (30)

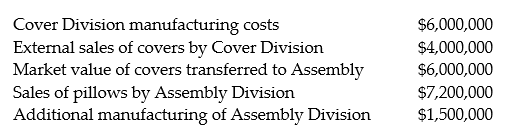

Bedtime Bedding Ltd. manufactures pillows. The Cover Division makes covers, and the Assembly Division makes the finished products. The covers can be sold separately for $5.00. The pillows sell for $6.00. The information related to manufacturing for the most recent year is as follows:

Required:

Compute the operating income for each division and the company as a whole. Use market value as the transfer price. Are all managers happy with this concept? Explain.

Required:

Compute the operating income for each division and the company as a whole. Use market value as the transfer price. Are all managers happy with this concept? Explain.

(Essay)

4.7/5 (40)

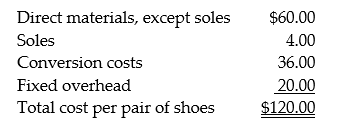

The Brownshoe Company has three specialized divisions. The Casual Shoe Division has asked the Sole Division to supply it with a large quantity of soles. The Sole Division is currently at capacity. The Sole Division sells soles outside for $5.00 each. The Casual Shoe Division, which is operating at 50 percent capacity, has offered to pay $4.00 per sole. The Sole Division has a variable cost of $3.60 per sole. The Casual Shoe Division has the following cost structure:

The manager of Casual Shoe believes that the $4 price from Sole is necessary if the division is to compete in the market for casual shoes.

Required:

a. As manager of Sole Division, would you recommend that your division supply the soles to Casual Shoe? Why?

b. Would it be desirable for the division to supply Casual Shoe with the soles for $4 assuming the Sole Division had excess capacity? Why?

c. What would be the corporate position assuming the Sole Division has excess capacity?

The manager of Casual Shoe believes that the $4 price from Sole is necessary if the division is to compete in the market for casual shoes.

Required:

a. As manager of Sole Division, would you recommend that your division supply the soles to Casual Shoe? Why?

b. Would it be desirable for the division to supply Casual Shoe with the soles for $4 assuming the Sole Division had excess capacity? Why?

c. What would be the corporate position assuming the Sole Division has excess capacity?

(Essay)

5.0/5 (32)

Clark Industries Ltd. manufactures monochromators that are used in a variety of applications. The Monochromator Division (M Division) sells its monochromators both internally and externally. It is operating at 80% of its 250,000 unit capacity and internal sales account for approximately 20% of its current sales volume. Internally the monochromators are transferred into the Aerospace Division (A Division) at a transfer price of $11,250 each. Variable production costs are the same for internal and external sales.

The income statement for the M Division is presented below:

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.

The Aerospace Division is operating at its full capacity of 40,000 units and is evaluating whether it should invest to increase capacity. The investment would cost $900,000,000 and would have a useful life of 3 years. The equipment could be sold for $800,000 at the end of its useful life. For tax purposes it would be sold on January 1 of year 4. The machine would be used to manufacture a variation of its current product with the same transfer price. This new product would sell for $68,000 per unit. The variable cost ratio will be 45% of the selling price. The additional capacity of the new machine would be 14,000 units. It would qualify for a 30% CCA rate and the company would continue to have assets in the pool.

Required:

a. Evaluate the current transfer pricing policy from the standpoint of each division manager as well as the company as a whole.

b. Using net present value (NPV) analysis, would the A Division manager want to invest in the new equipment if the required rate of return is 12% and the tax rate is 25%?

c. If the investment is evaluated from a corporate perspective using NPV analysis and the 12% discount rate, does the decision change? Explain.

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.

The Aerospace Division is operating at its full capacity of 40,000 units and is evaluating whether it should invest to increase capacity. The investment would cost $900,000,000 and would have a useful life of 3 years. The equipment could be sold for $800,000 at the end of its useful life. For tax purposes it would be sold on January 1 of year 4. The machine would be used to manufacture a variation of its current product with the same transfer price. This new product would sell for $68,000 per unit. The variable cost ratio will be 45% of the selling price. The additional capacity of the new machine would be 14,000 units. It would qualify for a 30% CCA rate and the company would continue to have assets in the pool.

Required:

a. Evaluate the current transfer pricing policy from the standpoint of each division manager as well as the company as a whole.

b. Using net present value (NPV) analysis, would the A Division manager want to invest in the new equipment if the required rate of return is 12% and the tax rate is 25%?

c. If the investment is evaluated from a corporate perspective using NPV analysis and the 12% discount rate, does the decision change? Explain.

(Essay)

4.7/5 (41)

In a time of distress prices, which of the following is TRUE?

(Multiple Choice)

4.7/5 (35)

Centralia Components Ltd. manufactures cable assemblies used in transportation, recreational products and medical industries . The capacity of the Manufacturing Division is currently 200,000 units and it sells 160,000 units to the outside market at an average price of $96/unit. Cost to manufacture the cable assemblies are $42 variable and $8 fixed. Fixed costs per unit are based on its normal volume of 160,000 units.

Centralia's Mobility Division uses cable assemblies in the manufacture of wheelchairs. It has offered to buy 25,000 units from the Manufacturing Division at $48 per unit. Calculate the operating income of the Manufacturing Division with and without the offer from the Mobility Division. Should the Manufacturing Division management accept the offer?

(Essay)

4.8/5 (46)

The Mill Flow Company has two divisions. The Cutting Division prepares timber at its sawmills. The Assembly Division prepares the cut lumber into finished wood for the furniture industry. No inventories exist in either division at the beginning of the year. During the year, the Cutting Division prepared 60,000 cords of wood at a cost of $660,000. All the lumber was transferred to the Assembly Division, where additional operating costs of $6 per cord were incurred. The 60,000 cords of finished wood were sold for $2,500,000.

Required:

a. Determine the operating income for each division if the transfer price from Cutting to Assembly is at cost.

b. Determine the operating income for each division if the transfer price is $9 per cord.

c. Since the Cutting Division sells all of its wood internally to the Assembly Division, does the manager care what price is selected? Why? Should the Cutting Division be a cost centre or a profit centre under the circumstances?

(Essay)

4.8/5 (41)

Use the information below to answer the following question(s).

Crush Company makes internal transfers at 180% of full cost. The Soda Refining division purchases 30,000 containers of carbonated water per day, on average, from a local supplier, who delivers the water for $30 per container via an external shipper. In order to reduce costs the company located an independent producer in Manitoba who is willing to sell 30,000 containers at $20 each, delivered to Crush Company's shipping division in Manitoba. The company's Shipping Division in Manitoba can ship the 30,000 containers at a variable cost of $2.50 per container and a full cost, based on practical capacity, of $4.00 per container. When the company's Manitoba shipping division ships for external customers is charges $6.00 per container.

-What is the total cost to Crush Company if the carbonated water is purchased from the local supplier?

(Multiple Choice)

4.9/5 (39)

Bradford Manufacturing Ltd. manufactures custom metal perforating and fabricating. Its Fabricating Division can transfer the perforated metal components to Bradford's Automotive Division or it can sell its products on the external market. Fabricating currently produces and sells 350,000 units per year to the external market at an average price of $38 per unit. Variable costs of production average $22.50 and fixed costs of $6.50/unit. Fabricating incurs $2.50 of variable selling costs on external sales. Fixed costs are based on the practical capacity of the plant which is 400,000 per year. The Automotive Division is interested in acquiring up to 50,000 units per year.

Required:

a. From the standpoint of Bradford Manufacturing Ltd., should the units be transferred? Determine the financial benefit or cost of your recommendation.

b. Using the general guidelines for transfer pricing, what is the minimum transfer price Fabricating should accept?

c. What is the range of acceptable transfer prices?

d. Now assume that demand in the external market for the components is expected to increase by 8%. The Automotive Division has negotiated with an external supplier to supply 50,000 units at a price of $34.50/unit. However, if the Automotive Division reduces its volume below the 50,000 unit volume, it must pay $39 per unit. What is the optimum sourcing arrangement for the company?

(Essay)

4.7/5 (35)

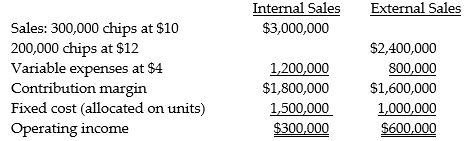

The Micro Division of Silicon Computers produces computer chips that are sold to the Personal Computer Division and to outsiders. Operating data for the Micro Division are as follows:

?

The Personal Computer Division has just received an offer from an outside supplier to furnish chips at $8.60 each. The manager of Micro Division is not willing to meet the $8.60 price. She argues that it costs her $9.00 to produce and sell each chip. Sales to outside customers are at a maximum of 200,000 chips.

Required:

a. Verify the Micro Division's $9.00 unit cost figure.

b. Should the Micro Division meet the outside price of $8.60? Explain on a per unit basis.

c. Prepare a Micro Division income statement for the sale to the Personal Computer Division assuming that the unit selling price of $8.60 is agreed. Comment on the allocation of fixed costs.

The Personal Computer Division has just received an offer from an outside supplier to furnish chips at $8.60 each. The manager of Micro Division is not willing to meet the $8.60 price. She argues that it costs her $9.00 to produce and sell each chip. Sales to outside customers are at a maximum of 200,000 chips.

Required:

a. Verify the Micro Division's $9.00 unit cost figure.

b. Should the Micro Division meet the outside price of $8.60? Explain on a per unit basis.

c. Prepare a Micro Division income statement for the sale to the Personal Computer Division assuming that the unit selling price of $8.60 is agreed. Comment on the allocation of fixed costs.

(Essay)

5.0/5 (40)

Use the information below to answer the following question(s).

Bon Accord uses two divisions in the production of soybean burgers. Division A sells soybean paste internally to Division B, which, in turn, produces soybean burgers that sell for $5 per kilogram. Division A incurs costs of $0.75 per kilogram, while Division B incurs additional costs of $2.50 per kilogram.

-What is Division A's operating income per kilogram assuming the transfer price of the soybean paste is set at $1.25 per kilogram?

(Multiple Choice)

4.9/5 (35)

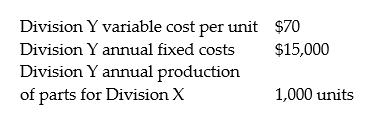

Mar Company has two decentralized divisions, X and Y. Division X has been purchasing certain component parts from Division Y at $75 per unit. Because Division Y plans to raise the price to $100 per unit, Division X desires to purchase these parts from external suppliers for $75 per unit. The following information is available:

If Division X buys from an external supplier, the facilities Division Y uses to manufacture these parts will be idle. Assuming Division Y's fixed costs cannot be avoided, what is the result if Mar requires Division X to buy from Division Y at a transfer price of $100 per unit?

If Division X buys from an external supplier, the facilities Division Y uses to manufacture these parts will be idle. Assuming Division Y's fixed costs cannot be avoided, what is the result if Mar requires Division X to buy from Division Y at a transfer price of $100 per unit?

(Essay)

4.9/5 (36)

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Minimum of sub optimal decision making.

(Multiple Choice)

4.7/5 (33)

The Home Office Company makes all types of office desks. The Computer Desk Division is currently producing 10,000 desks per year with a capacity of 15,000. The variable costs assigned to each desk are $300 and annual fixed costs of the division are $900,000. The computer desks sell for $400.

The Executive Division wants to buy 5,000 desks at $280 for its custom office design business. The Computer Desk manager refuses the order because the price is below variable cost. The Executive manager argues that the order should be accepted because it will lower the fixed cost per desk from $90 to $60 and will take the division to its capacity, thereby causing operations to be at their most efficient level.

Required:

a. Should the order from Executive Division be accepted by Computer Desk? Explain why or why not.

b. From the perspective of the Computer Desk Division and the company, should the order be accepted if the Executive Division plans on selling the chairs in the outside market for $420 after incurring additional costs of $100 per desk?

c. What action should the company president take?

(Essay)

4.9/5 (38)

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Bargaining between selling and buying units

(Multiple Choice)

4.7/5 (38)

Xenon Autocar Company manufactures automobiles. The Fastback Car Division sells its cars for $50,000 each to the general public. The fastback cars have manufacturing costs of $25,000 each for variable and $15,000 each for fixed costs. The division's total fixed manufacturing costs are $75,000,000 at the normal volume of 5,000 units.

The Coupe Car Division has been unable to meet the demand for its cars this year. It has offered to buy 1,000 cars from the Fastback Car Division at the full cost of $40,000. The Fastback Car Division has excess capacity and the 1,000 units can be produced without interfering with the current outside sales of 5,000. The 6,000 volume is within the division's relevant operating range.

Explain whether the Fastback Car Division should accept the offer.

(Essay)

4.8/5 (41)

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Variable manufacturing cost plus a mark-up

(Multiple Choice)

4.8/5 (37)

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Profit centres

(Multiple Choice)

4.7/5 (35)

Global Giant, a multinational corporation, has a producing subsidiary in a low tax rate country and a marketing subsidiary in a high tax country. If Global Giant wants to minimize its worldwide tax liability, we would expect Global Giant to

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)